How to Start Investing After Paying Off Debt: Your Real Next Step Forward

How to Start Investing After Paying Off Debt: Your Real Next Step Forward

Table of Contents

- Introduction

- What You’ll Learn

- The Psychological Shift Nobody Talks About

- Step 1 — Take a Real Look at Where You Stand

- Step 2 — Build Your Emergency Fund First

- Step 3 — Understand What Kind of Investor You Are

- Step 4 — Start With Tax-Advantaged Accounts

- Step 5 — Choose Your First Investment Vehicle

- Step 6 — Automate and Stay Consistent

- Real-World Case Study: Marcus from Ohio

- Practical Examples of How to Allocate Your Money

- Common Mistakes New Investors Make After Paying Off Debt

- Tools and Apps That Actually Help

- Frequently Asked Questions

- Sources Used in This Article

- Helpful Next Steps

By Arshiyan Ahmed | Personal Finance Writer | Last Updated: April 2025

You did it. The last payment went through, the balance hit zero, and for a moment you just sat there staring at the screen. Maybe you even did a little victory dance in your kitchen — no judgment here, I absolutely did mine.

But then comes the quiet. The autopay that used to drain your account every month is gone. There is extra money sitting there now. And the question that follows is almost louder than the debt ever was: What do I do with this?

This is the exact place where a lot of people either make a great decision or accidentally backfire. Some people go back into debt because they suddenly feel rich. Others just park the money in a savings account and never think twice, losing years of compounding growth. And a smaller group — the ones who get it right — use this moment as a launchpad.

This article is for that third group. Or for anyone who wants to be in it.

Trust Note: The information shared here is for educational purposes and reflects general financial principles. It is not personalized investment advice. Please consider consulting a certified financial planner (CFP) before making major investment decisions, especially if your financial situation is complex.

What You’ll Learn

By the time you finish reading this, you will know how to assess your financial position after debt payoff, understand which accounts to open first, pick investment options that match your actual risk level, avoid the most common beginner mistakes, and build a system that works on autopilot.

No MBA required. Just a clear head and some honest math.

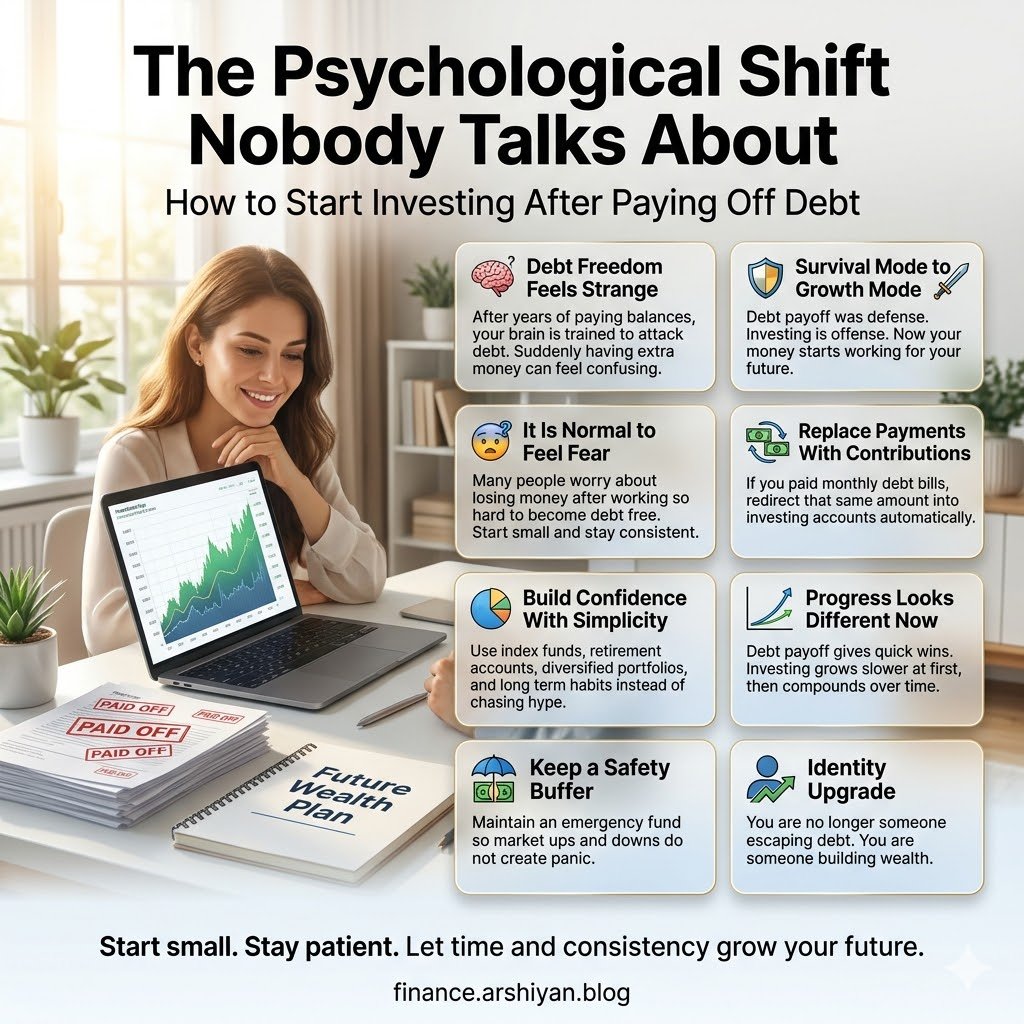

The Psychological Shift Nobody Talks About

Here is something financial influencers rarely bring up: paying off debt changes how your brain relates to money.

When you were in debt, every dollar had a mission. It went somewhere specific — minimum payment here, extra principal there. You were defensive with your money because you had to be.

Now there is no enemy. And weirdly, that freedom can feel paralyzing.

A 2023 study from Northwestern Mutual found that 72% of Americans who paid off significant debt reported feeling “financially lost” in the months that followed. Not broke. Not stressed. Just… directionless. It is like training for a marathon and then not knowing what to do after the finish line.

The solution is to redirect that same energy and intentionality you used during debt payoff into building wealth. The habits are already there. You just need a new target.

Step 1 — Take a Real Look at Where You Stand

Before you invest a single dollar, spend about 30 minutes getting a clean picture of your current finances.

Write down or open a spreadsheet and list the following:

Monthly take-home income — what actually hits your bank account after taxes.

Monthly fixed expenses — rent, utilities, insurance, subscriptions, food. Be honest. That Hulu and Netflix and Spotify triple stack counts.

What you were paying toward debt — this is now your investable amount, at least in part.

Current savings balance — how much liquid cash do you have sitting in a checking or savings account right now?

Once you have these numbers in front of you, you will immediately see what you are working with. For most people coming out of debt, there is anywhere from $200 to $800 a month that suddenly has no assignment. That is your starting capital.

Step 2 — Build Your Emergency Fund First

I know. You want to invest. You are fired up. But hear me out.

An emergency fund is not boring. It is the foundation that keeps you from raiding your investments every time your car needs a transmission or your water heater dies.

The general rule of thumb is three to six months of living expenses in a high-yield savings account. If your monthly expenses run about $3,000, you want between $9,000 and $18,000 parked somewhere safe and accessible.

Right now, the best high-yield savings accounts from institutions like Marcus by Goldman Sachs, Ally Bank, and SoFi are paying somewhere in the range of 4.5% to 5.0% APY. That is not nothing. Your emergency fund can actually earn real money while it waits.

If you already have a fully funded emergency fund, skip ahead. If not, give yourself 3 to 6 months to build it before you go all-in on investing. Yes, even before maxing your 401(k) — though capturing your employer match is worth doing simultaneously (more on that in a moment).

Step 3 — Understand What Kind of Investor You Are

This is not a personality quiz. It is a practical exercise.

Ask yourself one question honestly: If my investment dropped 30% in value tomorrow, what would I do?

If your honest answer is “sell everything immediately,” you are a conservative investor. You need more stable, lower-volatility options like bonds, target-date funds, or dividend-focused ETFs.

If your answer is “hold and maybe buy more,” you have a moderate to aggressive risk tolerance. You can lean heavier into stock index funds and growth ETFs.

Neither answer is wrong. Getting this right just means you are less likely to panic-sell during a market correction and lock in losses you did not have to take.

Your time horizon matters here too. If you are 28 years old, you have 35-plus years until retirement. Short-term volatility barely matters in that window. If you are 55, your runway is shorter and capital preservation becomes more important.

Step 4 — Start With Tax-Advantaged Accounts

Before you open a brokerage account and start picking stocks, look at what the government is essentially offering you for free.

401(k) with Employer Match

If your employer matches contributions up to a certain percentage, contribute at least that much. If they match 3% of your salary, you contribute 3% — because anything less means you are leaving part of your compensation on the table. That match is an immediate 50% to 100% return on your money, which no stock in history guarantees.

The 2025 contribution limit for a 401(k) is $23,500 per year, with an additional $7,500 catch-up contribution allowed if you are 50 or older.

Roth IRA

After capturing your employer match, many financial advisors recommend opening a Roth IRA next. With a Roth, you contribute after-tax dollars and your money grows completely tax-free. When you withdraw in retirement, you owe nothing to the IRS.

The 2025 annual contribution limit for a Roth IRA is $7,000 (or $8,000 if you are 50 or older). Income limits apply — single filers with a modified adjusted gross income above $161,000 begin to phase out of eligibility.

Platforms like Fidelity, Vanguard, and Charles Schwab make opening a Roth IRA straightforward. Fidelity in particular is highly recommended for beginners because there are no account minimums and their interface is clean and easy to navigate.

HSA (Health Savings Account)

If you have a high-deductible health plan, an HSA is one of the most underrated investment vehicles in the country. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. That is a triple tax benefit. After age 65, you can withdraw for any reason (non-medical withdrawals are just taxed as ordinary income, similar to a traditional IRA).

Step 5 — Choose Your First Investment Vehicle

Once your accounts are open, you need to actually buy something. This is where a lot of new investors freeze up because there are thousands of options.

Keep it simple. Here is what works well for most people starting out:

Total Stock Market Index Funds

These funds own a small piece of the entire U.S. stock market in one purchase. Vanguard’s VTI, Fidelity’s FZROX, and Schwab’s SCHB are popular options. Expense ratios are near zero, diversification is built-in, and you are betting on the U.S. economy as a whole rather than any single company.

S&P 500 Index Funds

Similar concept, but focused on the 500 largest publicly traded U.S. companies. VOO (Vanguard), FXAIX (Fidelity), and SPY (State Street) are the big names here. Historically, the S&P 500 has returned an average of roughly 10% per year over the long run, though past performance does not guarantee future results.

Target-Date Funds

If you want to set it and forget it, a target-date fund automatically adjusts its stock-to-bond ratio as you approach retirement. If you plan to retire around 2050, a “Target Date 2050” fund is the whole portfolio in a single ticker. Available from Vanguard, Fidelity, and Schwab.

Step 6 — Automate and Stay Consistent

The investors who win over time are rarely the ones who time the market perfectly. They are the ones who show up every single month without fail.

Set up automatic contributions on a schedule. Most 401(k) plans do this through payroll deduction already. For your IRA, set up a recurring transfer from your checking account on the same day each month — ideally the day after payday.

This strategy is called dollar-cost averaging. You buy more shares when prices are low and fewer when prices are high, which smooths out your average cost over time. It also removes emotion from the equation, which is honestly the biggest investment advantage most people never talk about.

Real-World Case Study: Marcus from Columbus, Ohio

Marcus, 34, finished paying off $22,000 in credit card and personal loan debt in late 2022 after three years of aggressive payments. He had been contributing just enough to his 401(k) to get his employer’s 3% match the entire time, so that piece was already in place.

When the debt was gone, he had about $550 per month that was suddenly free. Here is what he did over the next 18 months:

He spent the first four months building his emergency fund from $1,200 to $10,000 using a Marcus by Goldman Sachs high-yield savings account earning 4.75% APY.

Once the fund was in place, he opened a Roth IRA at Fidelity and set up an automatic monthly transfer of $500 into the account, investing it all into FZROX, Fidelity’s zero-fee total market index fund.

He also bumped his 401(k) contribution from 3% to 8% of his salary, since he now had the cash flow to handle it.

By early 2025, about two and a half years after his last debt payment, Marcus had over $28,000 in combined investment accounts. More importantly, he described having a completely different relationship with money. “I used to dread looking at my accounts,” he said. “Now I actually look forward to it.”

Practical Examples of How to Allocate Your Money

Here are a few scenarios to give you a concrete sense of what allocation might look like:

Scenario A — $300 per month freed up after debt payoff

First $100 goes toward completing the emergency fund. Remaining $200 goes into a Roth IRA invested in an S&P 500 index fund.

Scenario B — $600 per month freed up

Increase 401(k) contribution to capture full employer match if not already doing so. Open a Roth IRA and contribute $400 per month. Keep $100 in a high-yield savings account as a buffer for irregular expenses.

Scenario C — $1,000 or more per month freed up

Maximize Roth IRA contributions ($583 per month to hit $7,000 per year). Increase 401(k) contributions further. If both are maxed, open a taxable brokerage account and invest in low-cost index funds.

Common Mistakes New Investors Make After Paying Off Debt

Lifestyle inflation that eats the freed-up cash. This is the big one. You finally have breathing room, and suddenly a newer car or a bigger apartment starts sounding very reasonable. Give yourself a small reward — you earned it — but protect the majority of that freed-up cash for your future self.

Waiting for the “perfect” time to invest. There is no perfect time. The best time was ten years ago; the second-best time is now. Markets go up and down, but long-term investors who stay in the game historically come out ahead.

Picking individual stocks before understanding basics. There is nothing wrong with buying individual company shares eventually, but starting your investment journey with a handful of speculative stock picks is closer to gambling than investing. Begin with index funds, get comfortable, and expand from there.

Ignoring fees. An expense ratio of 1% might not sound like much, but over 30 years it can cost you tens of thousands of dollars in compounded lost growth compared to a fund charging 0.03%. Always check the expense ratio before you buy.

Not rebalancing once a year. If your stocks grow faster than your bonds, your portfolio drifts out of your target allocation over time. A quick annual check-up — most brokerage apps prompt this — keeps you on track.

Tools and Apps That Actually Help

Fidelity — Best overall platform for beginners. Zero-fee index funds, no account minimums, and clean mobile app.

Vanguard — The gold standard for low-cost investing, especially for long-term buy-and-hold investors.

Betterment — A robo-advisor that handles allocation and rebalancing for you. Good if you want more automation and less decision-making.

Personal Capital (now Empower) — Excellent free tool for seeing all your accounts in one place, tracking your net worth, and analyzing your investment fee load.

YNAB (You Need A Budget) — Still useful even after debt is gone. Helps you see exactly what your freed-up cash is doing each month.

NerdWallet and Investopedia — Reliable sources when you need to compare accounts, understand terms, or research specific funds.

Frequently Asked Questions

How much should I have saved before I start investing? Most experts recommend a fully funded emergency fund of three to six months of expenses before investing heavily. However, capturing any employer 401(k) match can happen at the same time — do not delay that.

Should I invest in crypto after paying off debt? Cryptocurrency is highly speculative. A small allocation (some advisors say no more than 5% of your overall portfolio) may be fine if you understand and accept the risk. But it should not be the first thing you put your money into.

What if I still have a mortgage? Should I pay it off or invest? This depends on your mortgage interest rate. If your rate is below 4% or so, the math often favors investing over extra principal payments, since historically stock market returns have exceeded that rate. Above 5% to 6%, it becomes more of a personal preference question.

I have no idea how to pick funds. What should I just buy? A single target-date fund from Fidelity, Vanguard, or Schwab based on your expected retirement year is a completely legitimate and well-regarded strategy. It is not a compromise. Many professional investors use this approach.

What is the first account I should open? If your employer offers a 401(k) with a match, start there. Then open a Roth IRA. If no employer match is available, the Roth IRA is usually the first move.

Sources Used in This Article

- IRS.gov — 2025 Retirement Contribution Limits

- Northwestern Mutual 2023 Planning and Progress Study

- Vanguard Investor Research on Dollar-Cost Averaging

- Fidelity Investments Learning Center

- Investopedia — Guide to Tax-Advantaged Accounts

- Charles Schwab — Index Fund Education Resources

Helpful Next Steps

Open a high-yield savings account this week if you do not already have one. Ally, Marcus by Goldman Sachs, and SoFi are all strong options with minimal friction to set up.

Log into your employer’s 401(k) portal and confirm you are getting the full match. If you are not, change your contribution percentage today.

Spend 20 minutes on Fidelity’s website looking at their Roth IRA opening process. It takes less than 15 minutes to open one.

Write down the exact dollar amount you used to put toward debt. Then write down where that money is going now. If you cannot answer that second question clearly, this is the moment to make a plan.

Paying off debt was not the finish line. It was the starting block. The race you are running now is the one that builds generational wealth, financial security, and the kind of freedom where you stop dreading your account balance and start looking forward to it.

You already proved you can do hard things. This next part is easier than you think.