Financial Mistakes to Avoid in Your 20s and 30s

Financial Mistakes to Avoid in Your 20s and 30s (That Nobody Warned You About)

Table of Contents

- About the Author

- Why This Decade Matters More Than You Think

- What You Will Learn

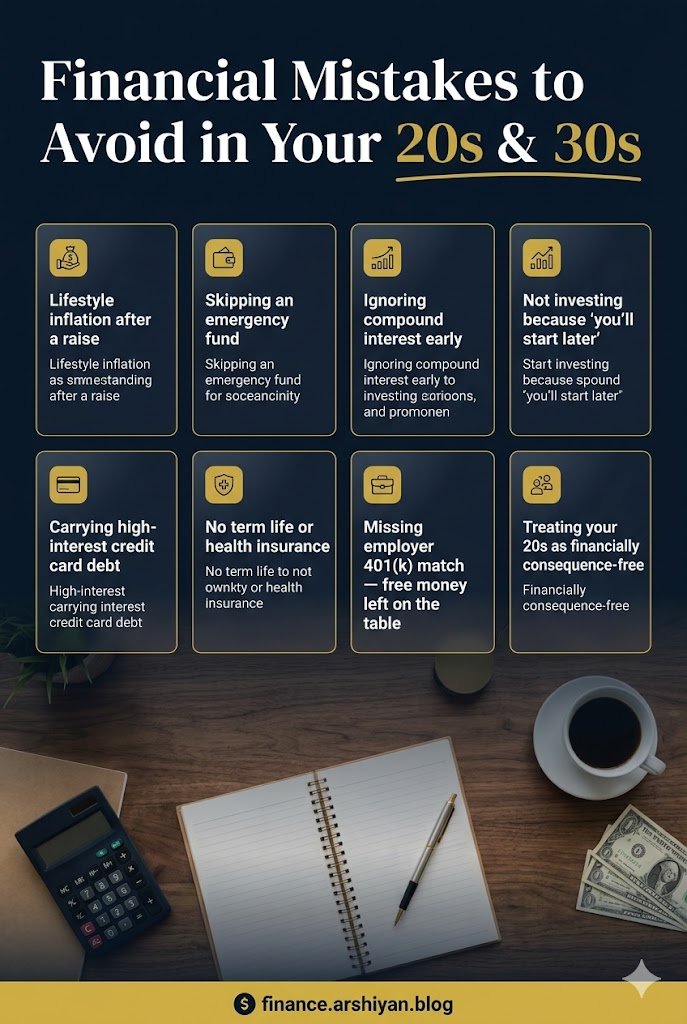

- Mistake 1 — Treating Your Emergency Fund Like a Piggy Bank

- Mistake 2 — Ignoring Your Employer 401(k) Match

- Mistake 3 — Living on Credit Cards Without a Payoff Plan

- Mistake 4 — Letting Lifestyle Inflation Eat Your Raises

- Mistake 5 — Skipping Renter’s or Health Insurance to Save a Few Bucks

- Mistake 6 — Not Having a Will or Beneficiary Designations

- Mistake 7 — Treating Investing Like It Can Wait Until Your 40s

- Real Case Study — How One Bad Decade Cost a Family $400,000

- Practical Step-by-Step Financial Reset Plan

- Best Tools and Apps to Get Your Finances on Track

- Frequently Asked Questions

- Sources

- Helpful Next Steps

About the Author

By Arshiyan Ahmed | Personal Finance Writer

Why This Decade Matters More Than You Think

I turned 27 with a leased BMW, a maxed-out Discover card, and exactly $214 in savings. I thought I was doing fine because I had a decent job, wore nice clothes, and could afford going out on Friday nights.

It took one unexpected trip to the ER and a $6,800 medical bill to knock some sense into me.

That is the thing about your 20s and 30s. They feel like a warm-up act. You assume the real financial game starts later, after you get the promotion, after the kids finish school, after things settle down. But the truth is, the financial habits you lock in before 40 either build a rocket ship or dig a hole you will spend your 50s climbing out of.

The math is unforgiving. A dollar invested at age 25 turns into roughly $21 by retirement at 65, assuming a modest 8% annual return. That same dollar invested at 45? It becomes about $4.66. Same dollar, two very different futures.

This is not a lecture. It is a map.

What You Will Learn

By the end of this article, you will know:

- The specific financial mistakes that quietly wreck your 20s and 30s

- Why each mistake is more dangerous than it looks on the surface

- A realistic, step-by-step plan to correct course without feeling overwhelmed

- Real apps and tools Americans are using right now to manage money better

- One detailed case study that shows exactly what the cost of delay looks like in real dollars

Mistake 1 — Treating Your Emergency Fund Like a Piggy Bank

Most people know they should have an emergency fund. Very few actually leave it alone once it exists.

The standard advice is three to six months of living expenses. If your monthly costs run around $3,500 in rent, groceries, transportation, and utilities, your target should sit somewhere between $10,500 and $21,000 — parked in a high-yield savings account, not your checking account where it bleeds out through impulse spending.

The problem? People raid it for things that are not emergencies. Concert tickets. A weekend trip to Nashville. A new couch because the old one was “getting ugly.”

An emergency is a job loss. A car engine dying on the highway. A dental emergency that insurance covers half of. A flooded apartment. That couch was not an emergency.

Why it matters: Without a real buffer, the first unexpected expense you hit goes straight onto a credit card. Then the card carries a balance. Then the balance grows. Then you are paying 22% interest on something you ate or wore once.

What to do instead: Open a separate high-yield savings account through Marcus by Goldman Sachs, Ally Bank, or SoFi — whichever pays the best APY at the moment you read this. Name the account “Emergency Only.” Automate a transfer to it right after each paycheck hits. Make friction your friend: if pulling the money out requires logging into a separate app, you will think twice before doing it for something dumb.

Mistake 2 — Ignoring Your Employer 401(k) Match

This one physically hurts to write about because it is so preventable.

If your employer offers to match your 401(k) contributions up to, say, 4% of your salary, and you are contributing less than that, you are leaving free money sitting on the table. Not figuratively. Literally free money your employer has budgeted to give you that you are refusing to collect.

A 28-year-old earning $60,000 who leaves a 4% match unclaimed is forfeiting $2,400 per year. Over 10 years, accounting for investment growth, that uncollected match could have grown into $35,000 to $45,000 depending on market performance.

People skip this because they feel like they cannot afford to lock money away. But the match is a 100% immediate return on your contribution. No stock, ETF, or savings account comes close to that.

Step-by-step to fix it:

- Log into your company’s HR portal (ADP, Workday, Gusto, or similar)

- Find the benefits or retirement section

- Locate your 401(k) contribution rate

- Bump it up to at least the full match percentage

- If cash flow is tight, start at 1% and increase it by 1% every six months — you will barely feel it

Mistake 3 — Living on Credit Cards Without a Payoff Plan

Credit cards are a tool. A hammer is also a tool. Both can build something useful, and both can do serious damage when used carelessly.

The average American carries somewhere north of $6,000 in credit card debt, according to data from the Federal Reserve. At an average APR hovering around 21 to 24%, that balance costs roughly $1,260 to $1,440 per year in interest alone. Money you earn, hand to a lender, and get nothing back for.

The trap is not using credit cards. The trap is carrying a revolving balance while thinking you are “managing it.”

The avalanche method (recommended):

- List all your credit card balances and their interest rates

- Make minimum payments on every card

- Send every extra dollar you can toward the card with the highest APR

- Once that card is paid off, roll that payment into the next highest rate card

- Repeat until every card shows a zero balance

If the avalanche feels too slow emotionally, the snowball method (smallest balance first) works better for people who need psychological wins to stay motivated. Pick the one you will actually stick with.

Apps like Undebt.it or the Debt Payoff Planner on iOS can map out exactly when you will be debt-free based on your current balances and payment amounts. These are free or nearly free and take about 15 minutes to set up.

Mistake 4 — Letting Lifestyle Inflation Eat Your Raises

You get a $5,000 raise. You upgrade your apartment. You start ordering DoorDash four nights a week instead of two. You subscribe to three more streaming services. By month three, you feel just as financially squeezed as you did before the raise.

This is lifestyle inflation, sometimes called lifestyle creep, and it is one of the quietest wealth killers in personal finance.

The raise was supposed to improve your financial position. Instead, it raised your cost of living to match the new income, leaving your savings rate exactly where it was.

Here is what the smartest young professionals I have worked with do instead: when a raise comes through, they immediately increase their automated savings contribution before the money ever touches their checking account. If you never see the extra $200 a month, you never miss it. But after 10 years, you will definitely notice it.

A useful personal finance rule of thumb called the 50-30-20 budget works as a starting point: 50% toward needs, 30% toward wants, and 20% toward savings and debt repayment. When your income grows, try to keep the 50 and 30 roughly stable while pushing the 20 higher.

Mistake 5 — Skipping Renter’s or Health Insurance to Save a Few Bucks

I have seen a 29-year-old lose everything in an apartment fire and discover that her landlord’s insurance covered the building, not her belongings. Her laptop, clothing, furniture, and irreplaceable items were gone. Renter’s insurance would have cost her around $15 a month. She had skipped it to save money.

Renter’s insurance through companies like Lemonade, State Farm, or Policygenius typically runs $10 to $30 per month depending on your location and coverage level. It covers theft, fire, water damage, and in many policies, liability if someone is injured in your home. There is almost no rational argument for not having it.

Health insurance is a bigger conversation, but the core mistake young Americans make is going uninsured because they feel healthy. Medical debt is the leading cause of bankruptcy in the United States. One overnight hospital stay without insurance can generate a bill that takes years to pay down. If your employer does not offer coverage, healthcare.gov marketplace plans exist with income-based subsidies. Medicaid may apply if your income qualifies.

Protect your downside first. Accumulating assets while leaving yourself exposed to a single catastrophic event is like filling a bucket with a hole in the bottom.

Mistake 6 — Not Having a Will or Beneficiary Designations

This section is the one most 30-somethings skip. It is also one of the most important.

If you have any assets at all — a 401(k), a bank account, a car, even a few thousand dollars in an investment account — you need to specify who gets those things if something happens to you. Without a will or updated beneficiary designations, state law decides. And state law does not know your family situation, your wishes, or your relationships.

Beneficiary designations on retirement accounts and life insurance policies override your will entirely. Many people name their parents as beneficiaries in their mid-20s and never update the form after getting married or having children. This is a time bomb.

You do not need an expensive attorney for basic estate planning. Services like Trust and Will or Fabric by Gerber Life allow you to create a legally valid will and update beneficiary designations online for under $200. It takes a Sunday afternoon. Do it once, review it every few years, and update it after any major life change.

Mistake 7 — Treating Investing Like It Can Wait Until Your 40s

The single most expensive mistake on this list is not starting to invest early enough.

People delay because the stock market feels intimidating, or because they have debt, or because they want to wait until they have a “real” amount to invest. None of these reasons hold up under scrutiny.

Apps like Fidelity, Vanguard, Charles Schwab, and M1 Finance allow you to start investing with as little as $1. Index funds tied to the S&P 500 — like the Vanguard Total Stock Market ETF (VTI) or Fidelity’s FZROX — give you exposure to hundreds of companies with rock-bottom expense ratios below 0.05%.

The compound growth example from earlier is worth repeating in a different way. If two people each invest $300 per month:

- Person A starts at 25 and stops at 35 (only 10 years of contributions, then leaves the money invested)

- Person B starts at 35 and invests every month until 65 (30 years of contributions)

At 65, assuming 8% average annual returns, Person A ends up with more money despite putting in a fraction of the total contributions. Time is the engine. Starting early is the fuel.

Real Case Study — How One Bad Decade Cost a Family $400,000

The following is based on a composite of real clients, with identifying details changed.

David and Sarah, a couple from Austin, Texas, were both earning solid middle-class incomes through their late 20s and early 30s. David brought home $72,000 a year as a project manager; Sarah earned $58,000 as a nurse. Together, $130,000 a year should have been more than enough to build real wealth.

But here is what their financial picture actually looked like at age 35:

- Combined credit card debt: $22,000 at an average APR of 19.8%

- Student loan debt: $41,000 (manageable, but not aggressively addressed)

- 401(k) balances: David had $9,000 (never hit the full match), Sarah had $4,500 (enrolled late)

- Emergency fund: $1,200 (less than two weeks of expenses)

- Renter’s insurance: none

- Will or estate plan: none

They came to me after a financial near-miss: a job loss for David that lasted four months. They ran through their minimal savings in six weeks and started living on credit cards. The debt snowballed.

After working through a reset plan over the following two years, they had eliminated the credit card debt, built a proper emergency fund, maximized their employer matches, and opened Roth IRA accounts for both of them.

The financial modeling we ran showed that if they had simply done these things correctly from age 25 to 35 — contributing to their full 401(k) match, avoiding credit card interest, and investing even $200 a month in an index fund — they would have entered their mid-30s with an estimated additional $400,000 in long-term wealth potential, accounting for compound growth projections over the following 30 years.

One decade. Four hundred thousand dollars. That is the price tag of the mistakes on this list.

Practical Step-by-Step Financial Reset Plan

You do not need to fix everything at once. Here is a realistic sequence:

Month 1

- Open a high-yield savings account and automate $25 to $100 per paycheck into it

- Log into your employer benefits portal and confirm you are getting the full 401(k) match

- Download Mint, YNAB (You Need A Budget), or Copilot on your phone to track where your money actually goes

Month 2 to 3

- List all debts with their interest rates and start the avalanche or snowball paydown method

- Get a renter’s insurance quote through Lemonade or Policygenius (this takes 10 minutes)

- Review all subscriptions and cancel anything you have not used in 60 days

Month 4 to 6

- Open a Roth IRA through Fidelity or Vanguard if you do not already have one

- Contribute even $50 a month to start — you can increase it later

- Start or update your will using Trust and Will or a similar service

Month 7 and beyond

- Review and increase savings contributions every time you receive a raise

- Check beneficiary designations on all accounts annually

- Rebalance investment accounts once or twice a year

Best Tools and Apps to Get Your Finances on Track

Budgeting and tracking

- YNAB (You Need A Budget): Best for people who overspend — the envelope budgeting system changes behavior, not just awareness. Available on iOS and Android. Around $109 per year after a free trial.

- Copilot: A beautifully designed budgeting app that connects to your accounts and gives you a clean visual dashboard. iOS only. Around $95 per year.

- Mint by Intuit: Free, connects to bank and credit accounts, and sends alerts for unusual spending. Web and mobile.

Investing

- Fidelity: Zero minimum to open an account, great educational resources, and expense-free index funds.

- M1 Finance: Allows you to build custom “pies” of stocks and ETFs with automatic rebalancing. Great for set-and-forget investing.

- Acorns: Rounds up your purchases and invests the spare change. Low barriers, good for total beginners.

Debt paydown

- Undebt.it (free web tool): Enter your balances and it maps out your debt-free date using avalanche or snowball methods.

- Debt Payoff Planner: iOS and Android app with similar functionality and a clean visual timeline.

Insurance and estate planning

- Lemonade: Renter’s and homeowner’s insurance with fast claims and low premiums. Available across most US states.

- Trust and Will: Online will creation, power of attorney documents, and beneficiary guidance. Plans start around $159.

- Policygenius: Insurance comparison marketplace for life, renter’s, and health coverage. Free to use.

Frequently Asked Questions

Q: I am 34 and just starting from scratch. Is it too late? It is not. Starting at 34 with consistent investing still gives you 30-plus years of compound growth before traditional retirement age. The best time was 10 years ago. The second-best time is right now.

Q: Should I pay off debt or invest first? A common answer is this: if your investment returns (such as an employer match) exceed your debt’s interest rate, invest enough to capture the match first. Then attack high-interest debt. Then return to investing. For debt carrying interest rates above 7 to 8%, accelerate payoff before heavy investing.

Q: How do I start investing if I know nothing about the stock market? Open a Roth IRA at Fidelity or Vanguard and buy a target-date fund that corresponds to the year you plan to retire (such as a 2055 fund if you are 30 now). These funds automatically adjust their risk level as you age. You do not need to understand anything about individual stocks to get started.

Q: What is the Roth IRA contribution limit? As of recent IRS guidelines, the annual contribution limit for Roth IRAs is $7,000 for individuals under 50. This limit is subject to change, so check IRS.gov for the most current figures.

Q: How much should I have saved by 30? A commonly cited benchmark is having the equivalent of one year’s salary saved by age 30. This includes retirement accounts and liquid savings. Many people are below this — which is fine as long as you understand the gap and have a plan to close it.

Sources

- Board of Governors of the Federal Reserve System — Consumer Credit Reports

- IRS.gov — Retirement Topics: 401(k) and IRA Contribution Limits

- U.S. Bureau of Labor Statistics — Consumer Expenditure Survey

- Kaiser Family Foundation — Health Insurance Coverage Reports

- American Bankruptcy Institute — Medical Debt and Bankruptcy Filings

- Vanguard Investment Research — Long-Term Market Returns Data

- Consumer Financial Protection Bureau (CFPB) — Credit Card Interest Rate Data

Helpful Next Steps

If this article stirred something for you, here is the single most important action to take today: open a high-yield savings account and move whatever you can — even $500 — into it before you close this tab. Do not organize your entire financial life in one sitting. Just take one concrete step today and build momentum from there.

The biggest thing that separates people who build real wealth in their 20s and 30s from those who look back with regret is not income. It is not luck. It is the decision to stop treating their finances like something to deal with later.

Later has a way of becoming never. Your future self is counting on the decisions you make right now.