How to Use Credit Cards Without Going Into Debt

How to Use Credit Cards Without Going Into Debt

Table of Contents

- About the Author

- Introduction

- A Quick Trust Note

- What You Will Learn

- Understanding the Real Danger of Credit Cards

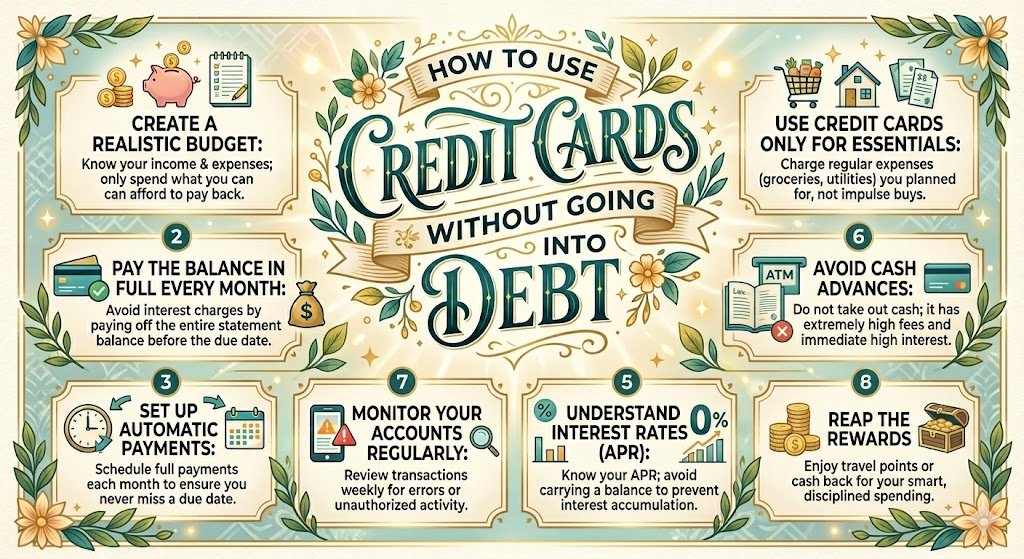

- Rule One: Treat Your Credit Card Like a Debit Card

- Rule Two: Always Pay the Full Balance Every Month

- Rule Three: Never Max Out Your Credit Limit

- Rule Four: Pick the Right Card for Your Life

- Rule Five: Set Up Alerts and Automate Payments

- Real-World Case Study: How Marcus Turned His Credit Card Habit Around

- Practical Examples of Smart Credit Card Use

- Mistakes People Make (And How to Dodge Them)

- Tools and Apps That Actually Help

- Frequently Asked Questions

- Sources Used in This Article

- Helpful Next Steps

About the Author

By Arshiyan Ahmed | Personal Finance Writer

Introduction

I still remember the sick feeling in my stomach the first time I opened my credit card statement and saw a balance I could not pay off. It was not some enormous number — just over $1,400. But I was fresh out of college, earning $28,000 a year in Chicago, and that number felt like a wall closing in on me.

The thing is, nobody really taught me how credit cards worked. I thought paying the minimum was the smart move. I thought having a high limit meant I had more money. I was wrong on both counts — and I paid for it, quite literally, in interest charges that piled up for almost two years.

That experience pushed me to dig deep into personal finance. I eventually became a credit counselor, helped hundreds of people untangle their debt, and learned every trick — good and bad — that credit cards have up their sleeve. This article is what I wish someone had handed me at age 22.

A Quick Trust Note

The guidance in this article is based on my personal experience as a certified credit counselor, publicly available data from the Consumer Financial Protection Bureau (CFPB), and information from well-established financial institutions. Nothing here is sponsored or paid placement. I am not telling you to open a specific card or use a particular bank. The goal is purely to give you a playbook that works.

What You Will Learn

- Why credit cards trap people even when those people are smart and careful

- The core rules that keep you debt-free while using credit cards regularly

- How to pick a card that actually benefits your lifestyle

- Real automation strategies that remove human error from the equation

- A real case study from a client (name changed) who reversed $6,200 in credit card debt

- The apps and tools that make tracking effortless

- The most common mistakes and how to sidestep them completely

Understanding the Real Danger of Credit Cards

Here is the thing about credit cards — they are not inherently evil. They are, in fact, one of the most powerful financial tools available to regular Americans when used properly. You get fraud protection, purchase insurance on big items, travel rewards, and a boost to your credit score. That is a lot of value sitting in a small plastic rectangle.

The danger is not the card itself. The danger is the psychological gap between swiping and paying.

When you hand over cash, your brain registers the loss immediately. Neuroscience researchers at Carnegie Mellon University found that cash payments actually activate the pain centers in the brain. Credit cards? They numb that response. You feel like you are spending future money, which always seems more available than the money you have right now.

Add to that the minimum payment trap — where a $2,000 balance at 24% APR could take over 10 years to pay off if you only make minimum payments — and you start to see how the system is designed to keep a certain type of user in debt.

The average American carries about $6,500 in credit card debt, according to data from Experian’s 2023 Consumer Credit Review. That is not because those people are irresponsible. It is because the product is designed to be used in a way that generates interest, and most users were never taught how to resist that pull.

Rule One: Treat Your Credit Card Like a Debit Card

This is the single most effective mindset shift you can make. Before you swipe your card, ask yourself one simple question: “Do I have this money sitting in my checking account right now?”

If the answer is no, you do not buy it. Period.

This is not about being a tightwad. It is about keeping your credit card use inside the boundaries of what you can actually afford. The card becomes a payment vehicle, not a borrowing tool.

Step-by-step approach:

- Before making a purchase, open your banking app (Chase, Bank of America, Wells Fargo, or whichever you use) and check your available balance.

- Only charge things to your card that your checking account can cover at that moment.

- At the end of each week, log in and mentally match your card charges to your bank balance.

- On payday, before spending a single cent on fun things, set aside the amount needed to pay your card bill in full.

This approach turns your credit card into a tool for earning rewards on purchases you would have made anyway. You stop borrowing. You start earning.

Rule Two: Always Pay the Full Balance Every Month

This one is non-negotiable. I have said it to every single client who sat across from me in my counseling office, and I will say it here too: the minimum payment is a financial trap dressed up as generosity.

When a credit card company shows you a minimum payment of $35 on a $1,200 balance, they are not doing you a favor. They are giving you just enough rope to stay comfortable while interest accumulates in the background.

At a standard 22% APR (which is close to the national average as of 2024), paying only the minimum on a $1,200 balance would cost you more than $900 in interest over time. You would essentially be paying nearly double for whatever you bought.

How to make sure you always pay in full:

- Set your credit card to autopay the statement balance, not the minimum. Most major issuers — Citi, Chase, Capital One, American Express — allow this through their apps or online portals.

- If autopay makes you nervous, set a calendar reminder three days before your due date as a backup.

- Never treat your credit card statement balance as optional. It is a bill, just like rent.

If you genuinely cannot pay the full balance one month because of a real emergency, pay as much as you can above the minimum, and stop using the card until the balance is zeroed out.

Rule Three: Never Max Out Your Credit Limit

Your credit utilization ratio — how much of your available credit you are using — is one of the biggest factors in your credit score. Keeping it below 30% is the standard advice, but honestly, the lower the better.

Here is a concrete example. If your card has a $5,000 limit, you want to keep your balance under $1,500. Ideally under $1,000.

But beyond the credit score angle, there is a practical reason too. When your balance creeps close to the limit, it becomes psychologically harder to stop spending. That buffer of available credit feels like permission. It is not.

What to actually do:

- Pick a personal spending ceiling that is well below your actual limit. If your limit is $3,000, treat $1,000 as your real cap.

- Many card issuers let you set a custom alert when you hit a certain spending threshold. Use it.

- If you find yourself regularly pushing near the limit, request a credit limit increase — not to spend more, but to lower your utilization percentage while keeping your real spending the same.

Rule Four: Pick the Right Card for Your Life

This is where a lot of people either make great decisions or waste enormous potential. Not all credit cards are the same, and the right card for a frequent traveler looks completely different from the right card for a family doing weekly grocery runs.

If you travel often: Cards like the Chase Sapphire Preferred or the American Express Gold Card offer travel points that can genuinely offset flight and hotel costs. The Sapphire Preferred, for instance, has historically offered 2x points on travel and dining, which adds up fast if those are your main expense categories.

If you mostly buy groceries and gas: A flat cashback card like the Citi Double Cash (2% back on everything) or the Blue Cash Preferred from American Express (6% at U.S. supermarkets) can quietly build you real savings over a year.

If you are rebuilding credit: A secured card like the Discover it Secured or Capital One Platinum Secured is the smart entry point. You put down a deposit, use the card for small purchases, pay it off monthly, and watch your score climb.

What to avoid: Cards with annual fees that you cannot justify through the rewards you actually earn. A $95 annual fee card that earns you $40 in cashback is losing you $55 a year.

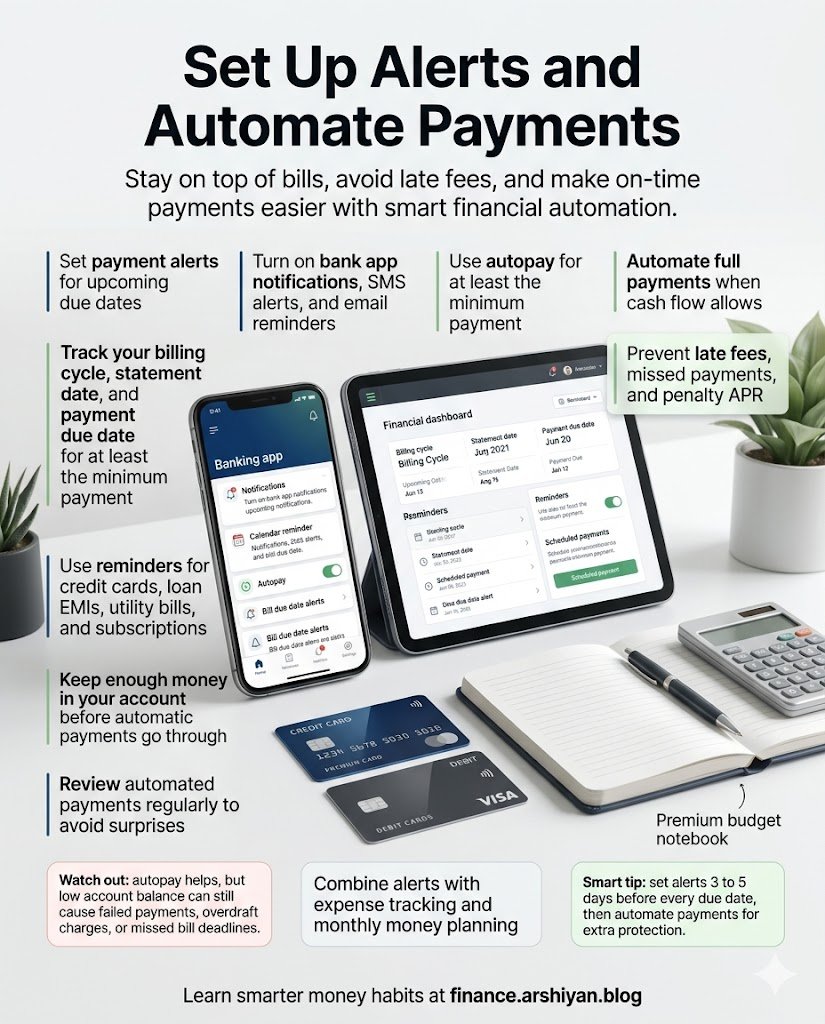

Rule Five: Set Up Alerts and Automate Payments

Human willpower is a depletable resource. By the end of a long workweek, the last thing you want to do is log into your bank and manually review charges. Automation removes the need for willpower entirely.

Here is the setup that works:

- Enable real-time transaction alerts through your card’s app. Every single time your card is used, you get a push notification. This keeps spending visible instead of invisible.

- Set a balance alert for when you hit a certain dollar amount. This acts as an early warning system.

- Automate payment of the full statement balance on the due date. Not the minimum — the full amount.

- Use a budgeting app like YNAB (You Need A Budget), Monarch Money, or even the built-in budgeting tool inside many bank apps to categorize your spending in real time.

With these systems in place, you barely have to think about it. The guardrails are doing the work for you.

Real-World Case Study: How Marcus Turned His Credit Card Habit Around {#real-world-case-study}

Marcus (name changed for privacy) came to me as a client in 2021. He was 31, working in IT in Atlanta, earning a solid $72,000 a year. On paper, he should have been comfortable. Instead, he was carrying $6,200 across three credit cards, making minimum payments each month, and watching the balances barely move.

His problem was not income. It was a habit. He used his cards for everything — restaurants, Amazon purchases, weekend trips — without any system to track whether he could actually afford those things. He assumed the minimum payment meant he was staying current. He did not realize he was treading water against a current.

What we did over 14 months:

- First, we stopped using two of the three cards entirely. He cut them up. Not canceled — that can ding your credit score — but physically cut and removed from his wallet.

- He redirected $600 per month from discretionary spending toward the card with the highest interest rate first (the avalanche method).

- He set up the budget alert on his Chase app at $400 per month, which was his new card spending limit.

- He automated full statement balance payment each month once the high-interest card was cleared.

By month 14, Marcus was debt-free on all three cards. He had also improved his credit score by 71 points during that same period, largely because his utilization ratio dropped from 68% to under 10%.

He still uses credit cards today. He just treats them like the tools they are, not like a safety net.

Practical Examples of Smart Credit Card Use

Example 1: Monthly Groceries Sarah spends about $400 a month on groceries. She puts all of it on her Blue Cash Preferred card, which returns 6% at supermarkets. That is $24 back per month, or $288 per year. She pays the balance in full each month. No interest. Pure profit.

Example 2: A Planned Vacation Dave and his partner want to take a trip to Florida. Instead of putting the flights and hotel on credit and worrying about it later, they save for three months first. When they book the trip, they charge everything to a travel rewards card, immediately pay the card with the money they had already saved. They earn about 12,000 points and pay zero interest.

Example 3: A Home Emergency Lisa’s water heater breaks. The repair costs $850, which she does not have in cash right now. She puts it on her low-APR card, but she also moves $300 from savings immediately and commits to paying $150 extra per month until it is cleared. She treats it as a short-term, time-limited exception — not permission to spend freely.

Mistakes People Make (And How to Dodge Them) {#mistakes-people-make}

Mistake 1: Opening too many cards at once. Each new application creates a hard inquiry on your credit report. Multiple inquiries in a short window can lower your score temporarily and signal risk to lenders.

Mistake 2: Closing old cards. Closing a card reduces your available credit, which raises your utilization ratio. If you want to stop using a card, just lock it away rather than closing the account.

Mistake 3: Ignoring the due date vs. the statement closing date. These are two different things. Charges made after the statement closes show up on the next month’s bill. Misunderstanding this leads to surprise balances.

Mistake 4: Using a credit card for cash advances. This is one of the most expensive things you can do. Cash advances typically come with a fee of 3% to 5% plus a higher APR than regular purchases — and interest starts accruing immediately with no grace period.

Mistake 5: Paying on time but not paying in full. On-time payments help your credit score, yes. But carrying a balance means you are still paying interest. These are two separate things.

Mistake 6: Ignoring the statement entirely. Credit card fraud is real. If you do not review your statement monthly, fraudulent charges can sit there quietly, racking up interest that you eventually owe.

Tools and Apps That Actually Help {#tools-and-apps-that-actually-help}

YNAB (You Need A Budget): Available on iOS and Android, YNAB connects to your bank and credit card accounts and helps you assign every dollar a purpose before you spend it. It has a learning curve but is widely considered the gold standard for people who want to get serious about their spending. Subscription costs about $14 a month or $99 annually.

Monarch Money: A newer competitor to YNAB that many people find more intuitive. Excellent for couples managing shared finances. Connects to most major U.S. banks and card issuers.

Credit Karma: Free tool that shows your TransUnion and Equifax credit scores and explains what is affecting them. Useful for tracking your utilization ratio month over month.

Your Bank’s Native App: Chase, Bank of America, Wells Fargo, and most other major banks now have built-in spending dashboards, category breakdowns, and alert systems that are genuinely useful and free.

NerdWallet Credit Card Comparison Tool: Before picking a new card, use NerdWallet’s comparison feature to filter cards by your spending habits. It is unbiased and comprehensive.

Frequently Asked Questions

Q: Can I build credit while still paying in full every month? Yes, absolutely. Payment history and credit utilization both factor into your score. Paying in full each month actually helps more than carrying a balance, because your utilization stays low and your payment record stays clean.

Q: What if I have already built up credit card debt? Where do I start? List all your cards, their balances, and their interest rates. Pay the minimum on all of them to stay current, then put every extra dollar toward the card with the highest APR first. This is the avalanche method and it minimizes the total interest you pay.

Q: Is it better to have one card or multiple cards? It depends. Multiple cards can improve your available credit and thus lower your utilization ratio, which benefits your score. But multiple cards also mean multiple statements to track and more opportunities for spending to slip through the cracks. Start with one, master it, then consider a second only if there is a clear reward benefit.

Q: How long does it take to see a credit score improvement? Most people see meaningful movement within three to six months of lowering their utilization ratio and maintaining on-time payments. A 50 to 80 point improvement is achievable within a year for most people starting from a mid-range score.

Q: Should I use credit cards for small everyday purchases like coffee? Yes, if you are disciplined. Small purchases add up into real rewards over time. The key is that you were going to buy the coffee anyway — you are just choosing how to pay for it. As long as you are not buying coffee you cannot afford just because the card makes it painless, it is a smart habit.

Sources Used in This Article

- Experian 2023 State of Credit Report — average U.S. credit card debt figures

- Consumer Financial Protection Bureau (CFPB) — credit card interest and minimum payment guidelines

- Carnegie Mellon University research on cash vs. card spending behavior (cited in Neuroeconomics: Decision Making and the Brain, 2nd edition)

- NerdWallet Credit Card Database — card feature comparisons

- FICO Score education resources at myfico.com — credit utilization impact on scores

Helpful Next Steps

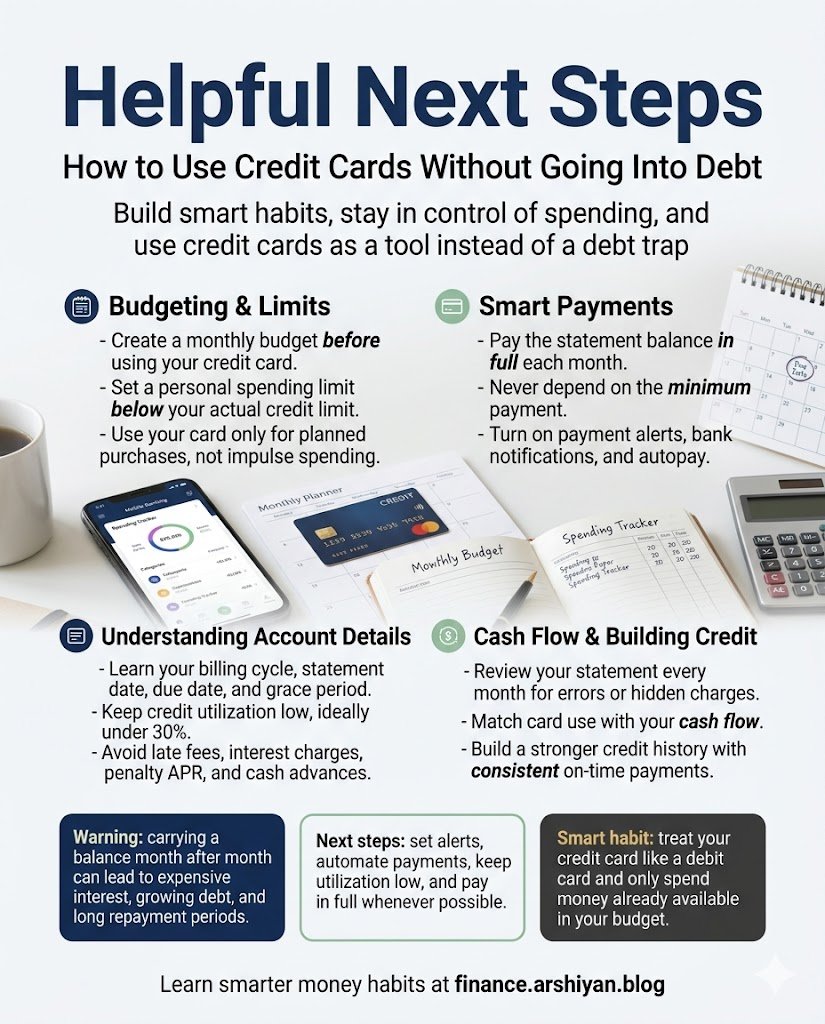

If you made it this far, you already have more practical credit card knowledge than most people walking into a bank branch. Here is what I would suggest doing in the next 48 hours:

Step 1: Pull up your most recent credit card statement. Look at the interest rate, the current balance, and the “time to pay off if minimum payments only” disclosure — most issuers are now required to show this. Stare at it. Let it motivate you.

Step 2: Log into your card account and switch autopay from “minimum payment” to “statement balance” if you have not already.

Step 3: Download one budgeting app — YNAB, Monarch, or even just your bank’s built-in tool — and connect your accounts.

Step 4: Set a real spending cap for your card this month. Write it down. Tell someone about it if that helps you stick to it.

Credit cards used correctly are one of the few consumer financial products that genuinely pay you back. Used carelessly, they are one of the most effective wealth-draining mechanisms ever invented. The difference between those two outcomes is almost entirely about systems, habits, and awareness — none of which require a high income or an economics degree.

You have got this.

This article is intended for informational purposes only and does not constitute personalized financial advice. Please consult a certified financial planner or credit counselor for guidance specific to your situation.