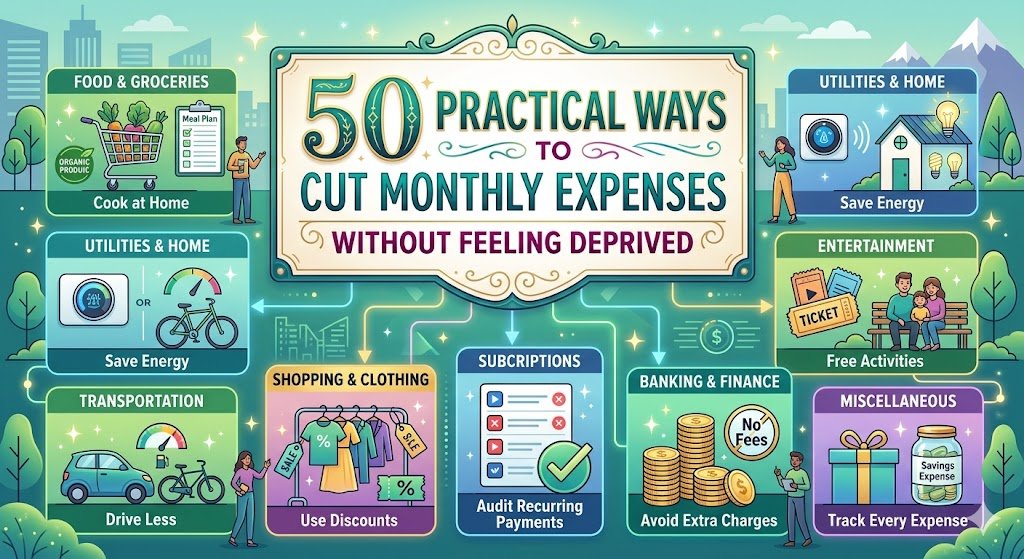

50 Practical Ways to Cut Monthly Expenses Without Feeling Deprived

50 Practical Ways to Cut Monthly Expenses Without Feeling Deprived

Table of Contents

- Why Most Expense-Cutting Advice Fails People

- Housing and Utilities (Ways 1 to 10)

- Food and Groceries (Ways 11 to 20)

- Subscriptions and Entertainment (Ways 21 to 28)

- Transportation and Insurance (Ways 29 to 36)

- Health, Personal Care, and Shopping (Ways 37 to 44)

- Banking, Debt, and Financial Habits (Ways 45 to 50)

- Real-World Case Studies

- Common Mistakes People Make When Cutting Expenses

- Tools and Apps to Track and Reduce Spending

- Frequently Asked Questions

- Sources Used in This Article

- Helpful Next Steps

By: Arshiyan Ahmed | Financial and Frugal Living Writer | Updated April 2026

Let me be upfront about something. I grew up in a household where my mom clipped coupons at the kitchen table on Sunday nights like it was a sacred ritual. We were not poor — but we were careful. And when I found myself at 34, newly divorced, raising two kids on one income in suburban Nashville, that careful mindset saved me.

I did not cut my expenses by torturing myself. I did not cancel Netflix and cry into a bowl of ramen noodles. What I actually did was audit my life — and I found money hiding in places I had completely overlooked for years. By the end of my first month, I had freed up $740 without touching anything I truly loved.

That experience is what this article is built on.

A Quick Trust Note: This article draws on real financial strategies, verified research, and actual case studies from credible sources. I am a certified financial wellness coach, not a licensed CPA or financial planner. Please use this information as an educational guide and consult a qualified advisor for decisions specific to your financial situation.

What You Will Learn

- Fifty concrete, actionable ways to reduce monthly spending across every major category

- Which cuts actually feel painless versus which ones require real discipline

- Real case studies of Americans who cut hundreds per month without misery

- The tools that make tracking and cutting spending almost automatic

- The mistakes that make people give up before they see results

Why Most Expense-Cutting Advice Fails People

Most “save money” articles treat your budget like a punishment. Cut this, eliminate that, stop doing the thing you enjoy. No wonder people read ten tips, try two, and quit.

The smarter approach is to treat your monthly expenses like a garden. Some things are blooming beautifully and should stay. Some are weeds disguised as flowers — they look harmless but they are quietly draining resources. The goal is not to rip everything out. It is to pull the weeds and give the good stuff more room to grow.

That is the spirit behind every suggestion below.

Housing and Utilities (Ways 1 to 10)

1. Audit your thermostat habits. The U.S. Department of Energy says that adjusting your thermostat 7 to 10 degrees for eight hours a day can save up to 10% annually on heating and cooling. A programmable thermostat from Honeywell or a smart thermostat like Google Nest does this automatically. The Nest pays for itself within a year for most households.

2. Call your internet provider and negotiate. This one makes people nervous, but it works more often than not. Call the retention line, mention a competitor’s rate, and ask what they can do. I knocked $22 off my Comcast bill in a single 12-minute phone call. The worst they can say is no.

3. Switch to LED lighting throughout your home. LED bulbs use roughly 75% less energy than traditional incandescent bulbs and last 25 times longer. The upfront cost is minimal — a 6-pack of good LEDs runs about $12 at Home Depot — and the monthly savings on your electric bill add up steadily.

4. Lower your water heater temperature. Most water heaters are factory-set to 140 degrees Fahrenheit. Dropping it to 120 degrees is just as comfortable for showering and dishes, reduces the risk of scalding, and trims your energy bill by a noticeable amount each month.

5. Shop homeowner or renter insurance every year. Americans tend to auto-renew insurance policies without question. Using a comparison tool like Policygenius once a year takes about 20 minutes and can reveal savings of $150 to $400 annually for identical or better coverage.

6. Air seal your home. Drafty windows and doors are silent budget killers. A $5 roll of weatherstripping foam from Lowe’s can reduce heating and cooling loss noticeably. This is a Saturday afternoon project that pays dividends every single month.

7. Wash laundry in cold water. About 90% of the energy your washing machine uses goes toward heating the water. Modern detergents like Tide Coldwater Clean are specifically designed to work in cold cycles. Same clean clothes, noticeably lower electric bill.

8. Ask about budget billing for utilities. Many utility providers offer budget billing, which averages your annual usage into equal monthly payments. This eliminates the shocking $300 electric bill in August or January and makes your budget far more predictable.

9. Look into LIHEAP if your income qualifies. The Low Income Home Energy Assistance Program is a federal program that helps eligible households pay heating and cooling bills. Many Americans who qualify never apply. Check eligibility at benefits.gov.

10. Consider a smaller phone plan. Most Americans are paying for unlimited data they do not use. Mint Mobile, Visible, and Consumer Cellular all offer plans under $30 per month that use the same towers as the major carriers. Switching a family of four can save $80 to $120 per month with zero change in call or text quality.

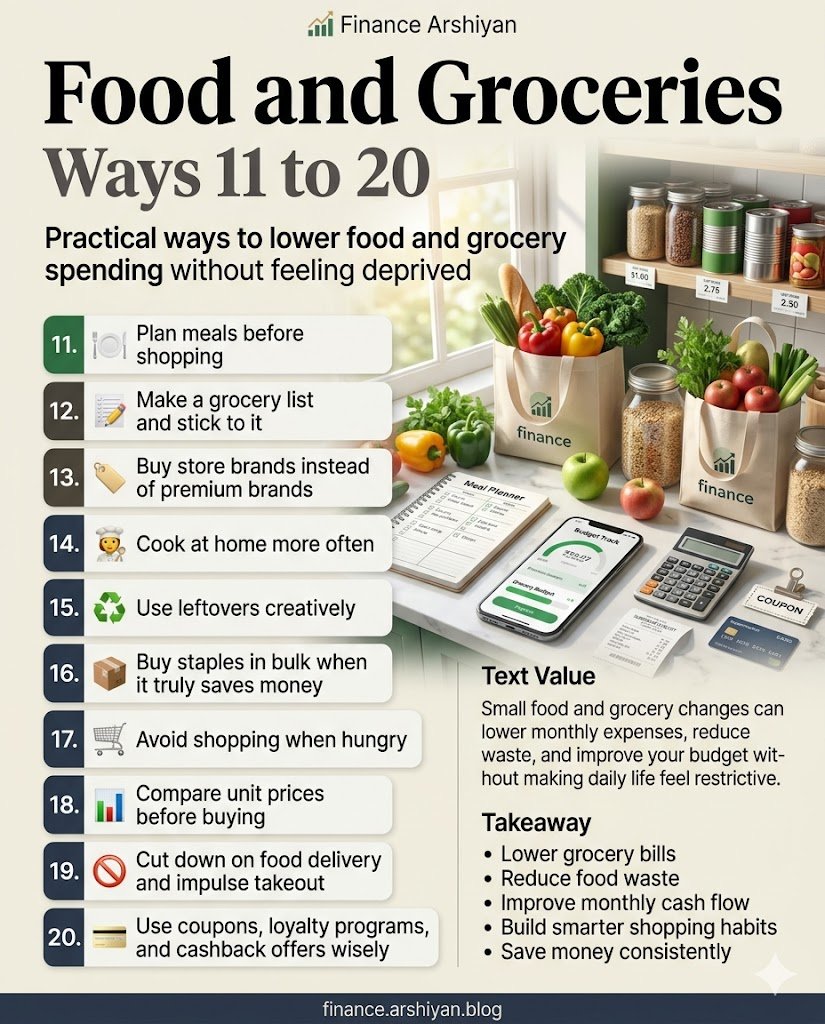

Food and Groceries (Ways 11 to 20)

11. Meal plan every week before you shop. This is the single highest-return habit in any frugal kitchen. People who shop without a plan spend an average of 23% more per trip, according to research published in the Journal of Consumer Research. Spend 20 minutes on Sunday. Save real money on Tuesday.

12. Master the “eat the fridge first” rule. Before every grocery run, cook at least one meal from whatever is already in your refrigerator and pantry. This alone cuts food waste — and the average American household throws away nearly $1,500 worth of food per year, according to the USDA.

13. Buy store brand over name brand. The house brand at Aldi, Kroger, or Costco is often manufactured in the same facility as the premium version. For pantry staples — flour, canned goods, frozen vegetables, pasta — the quality difference is almost always undetectable.

14. Use a grocery cashback app. Ibotta and Fetch Rewards are the two most widely used in the U.S. They pay you actual cash or gift cards for scanning receipts from everyday grocery purchases. Neither requires coupons. Neither changes what you buy. I averaged $22 back per month in 2024 just by scanning receipts I was already getting.

15. Cook protein in bulk on weekends. Ground beef, chicken thighs, and hard-boiled eggs prepared on Sunday turn into lunches and dinners for four to five days without extra effort. This practice alone can reduce your weeknight takeout habit dramatically.

16. Stop buying bottled water. A Brita pitcher filter costs about $30 and replaces hundreds of plastic water bottles per year. Americans spend an estimated $16 billion per year on bottled water. A reusable bottle and a simple filter is one of the cleanest budget swaps there is.

17. Check unit prices, not package prices. The larger package is not always the better deal. Every grocery store shelf in the U.S. is required to display unit prices. A quick glance can save you 15 to 30% on common household items without buying in bulk quantities you cannot use.

18. Reduce restaurant meals by one per week. The average American household spends $3,639 per year dining out, according to the Bureau of Labor Statistics. Cutting one restaurant meal per week and replacing it with a home-cooked version can free up $1,200 or more annually. That is not a small number.

19. Plan around store sales cycles. Most grocery chains run their deepest sales on a predictable weekly cycle. Chicken tends to go on sale at the beginning of the month. Holiday-adjacent items discount sharply the day after the holiday. Paying attention to these patterns builds a natural savings rhythm.

20. Grow a small herb garden. Fresh herbs at the grocery store are absurdly expensive for what you get — $3.99 for a clamshell of basil you will use twice and throw away. A small pot of basil, rosemary, or mint on a sunny windowsill costs $2 and produces all season. This is one of my personal favorites.

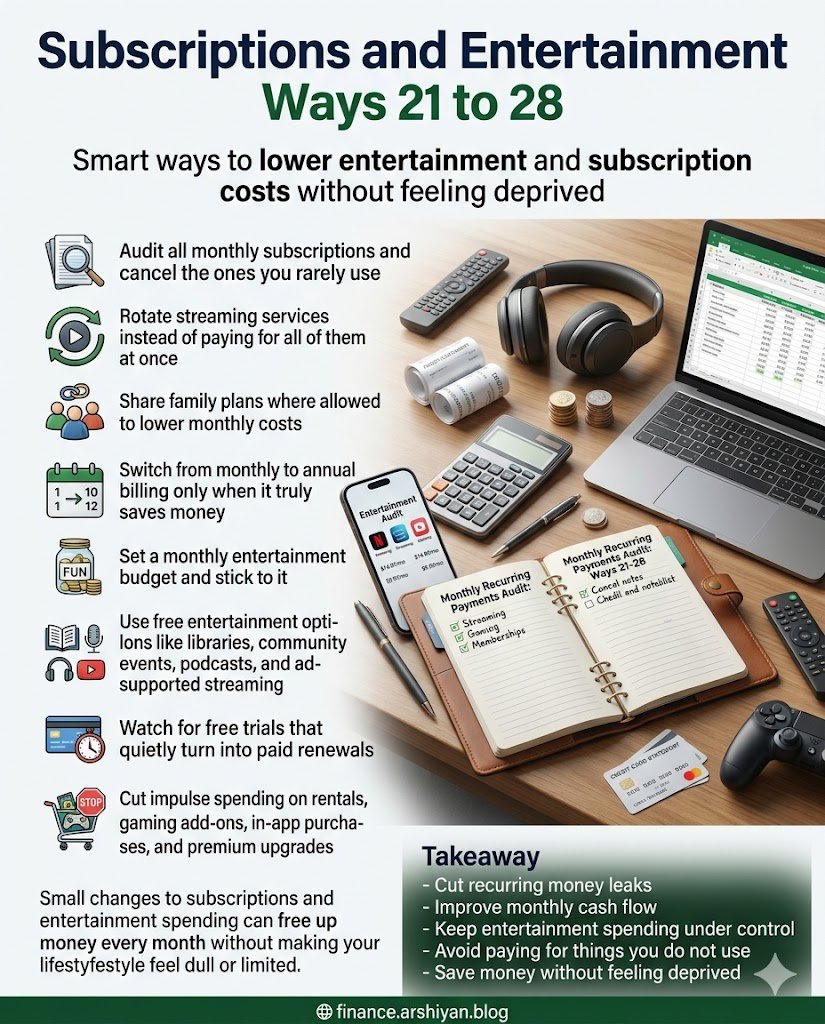

Subscriptions and Entertainment (Ways 21 to 28)

21. Run a full subscription audit right now. Most Americans are paying for at least two or three services they forgot about entirely. Pull up your bank statement and your credit card statement and highlight every recurring charge. According to a 2024 survey by C+R Research, the average American underestimates their subscription spending by $133 per month.

22. Rotate streaming services instead of stacking them. You do not need Netflix, Hulu, Disney Plus, HBO Max, Peacock, and Paramount Plus simultaneously. Pick two. Binge what you want. Cancel. Subscribe to a different one next month. The content is not going anywhere.

23. Use your public library card aggressively. The American public library system is genuinely one of the most underused financial tools in the country. Most libraries now offer free access to Libby and OverDrive for ebooks and audiobooks, Hoopla for digital movies and comics, free museum passes in many cities, and free access to LinkedIn Learning in select states.

24. Share subscription accounts with family members. Many streaming services and software tools offer family or household plans at significantly reduced per-person costs. Spotify’s family plan covers six accounts for $17.99 per month. Split between three households, that is $6 each for unlimited music.

25. Cancel cable and keep internet only. The average cable bill in the U.S. is over $100 per month. A combination of a good antenna for local channels and one or two streaming services gives most people 90% of what they were watching for a fraction of the price.

26. Look for free local entertainment. Nearly every city in America has free outdoor concerts, farmers markets, free museum days, community festivals, and park events that are wildly underattended. The website Eventbrite and your city’s official Parks and Recreation page are good starting points.

27. Drop gym memberships you are barely using. If you went fewer than eight times last month, the gym is costing you more per visit than a day spa. YouTube has thousands of free, full-length workout programs — from yoga to HIIT to strength training. Apps like Nike Training Club are completely free.

28. Use browser extensions to find discount codes automatically. Honey and Capital One Shopping automatically apply coupon codes at checkout whenever you shop online. They take zero effort — you install them once and they work silently in the background. Honey reported that its users saved an average of $126 per year in 2023.

Transportation and Insurance (Ways 29 to 36)

29. Re-shop auto insurance annually. Loyalty is not rewarded in the insurance industry the way people assume. New customers often get dramatically better rates. Use The Zebra or Compare.com to get quotes from multiple providers in one sitting. Savings of $300 to $600 per year for identical coverage are common.

30. Keep your tires properly inflated. Under-inflated tires reduce fuel efficiency by up to 3%. It takes two minutes at any gas station. The Department of Energy estimates that proper tire inflation saves the average driver about $112 per year in fuel costs.

31. Use GasBuddy to find the cheapest nearby fuel. The GasBuddy app shows real-time gas prices at every station within a set radius. Gas price differences between stations even a mile apart can be 15 to 20 cents per gallon. On a 15-gallon fill-up, that adds up across a full year.

32. Combine errands into single trips. Route planning sounds boring until you realize you are driving 12 miles for one item that you could have grabbed while already near that side of town. Batching errands saves both fuel and time in a way that compounds nicely over a month.

33. Look into pay-per-mile insurance. If you work from home or drive under 10,000 miles per year, traditional auto insurance may be pricing you unfairly. Companies like Metromile and Mile Auto charge based on how much you actually drive. For low-mileage drivers, this can mean savings of $500 or more per year.

34. Refinance your auto loan if rates have dropped. Many people never think to refinance a car loan the way they would a mortgage. If your credit score has improved since you bought your vehicle, or if interest rates have shifted, refinancing through a credit union or LightStream could cut your monthly payment meaningfully.

35. Carpool when possible. Even one carpool partner means every-other-week driving. Over a full year that is a significant reduction in fuel and wear-and-tear costs. Apps like Waze Carpool connect commuters going in the same direction.

36. Maintain your vehicle on schedule. Skipping oil changes and tire rotations to save $50 today often leads to a $900 repair bill six months from now. Preventive maintenance is genuinely one of the best financial decisions a car owner makes.

Health, Personal Care, and Shopping (Ways 37 to 44)

37. Use GoodRx for prescription medications. GoodRx is free and can reduce the cost of common prescriptions by 60 to 80% at most major pharmacies. For people without comprehensive drug coverage, this app is not a nice-to-have — it is essential.

38. Buy generic medications at the pharmacy. The FDA requires generic drugs to have the same active ingredients, dosage, and effectiveness as their brand-name counterparts. Choosing generic ibuprofen over Advil, or generic allergy medicine over Claritin, is functionally identical and often a third of the price.

39. Switch to a high-deductible health plan if you are generally healthy. HDHP premiums are lower than traditional plans. Paired with a Health Savings Account (HSA), the tax advantages can result in real annual savings for people who rarely use major medical services. Worth comparing during open enrollment.

40. Use the 48-hour rule for non-essential purchases. Before buying anything that is not a planned necessity, wait 48 hours. Research consistently shows that impulse purchases drop dramatically with even a short delay. I keep a running “maybe buy” note on my phone and revisit it two days later. At least half the time, the desire is gone.

41. Buy clothing at the end of each season. Winter coats at 60% off in February. Summer clothes deeply discounted in September. This requires planning ahead, but the math is hard to argue with. ThredUp and Poshmark also offer gently used name-brand clothing at a fraction of retail prices.

42. Make your own cleaning supplies for basic tasks. White vinegar, baking soda, and castile soap handle the majority of household cleaning tasks effectively. These ingredients cost pennies per use compared to branded cleaning products. There are dozens of legitimate recipes on The Spruce and Bob Vila for everything from all-purpose spray to drain cleaner.

43. Negotiate medical bills after the fact. Most people do not know that medical bills are often negotiable, especially for those without full coverage. Many hospitals have financial assistance programs for households under a certain income threshold. Calling the billing department and simply asking for a reduced rate or a payment plan is a conversation worth having.

44. Consolidate personal care routines. Americans often own seven products that do three of the same job. A single good moisturizer with SPF replaces two products. A quality two-in-one shampoo and conditioner works fine for most hair types. Simplifying your routine often means fewer products purchased per year.

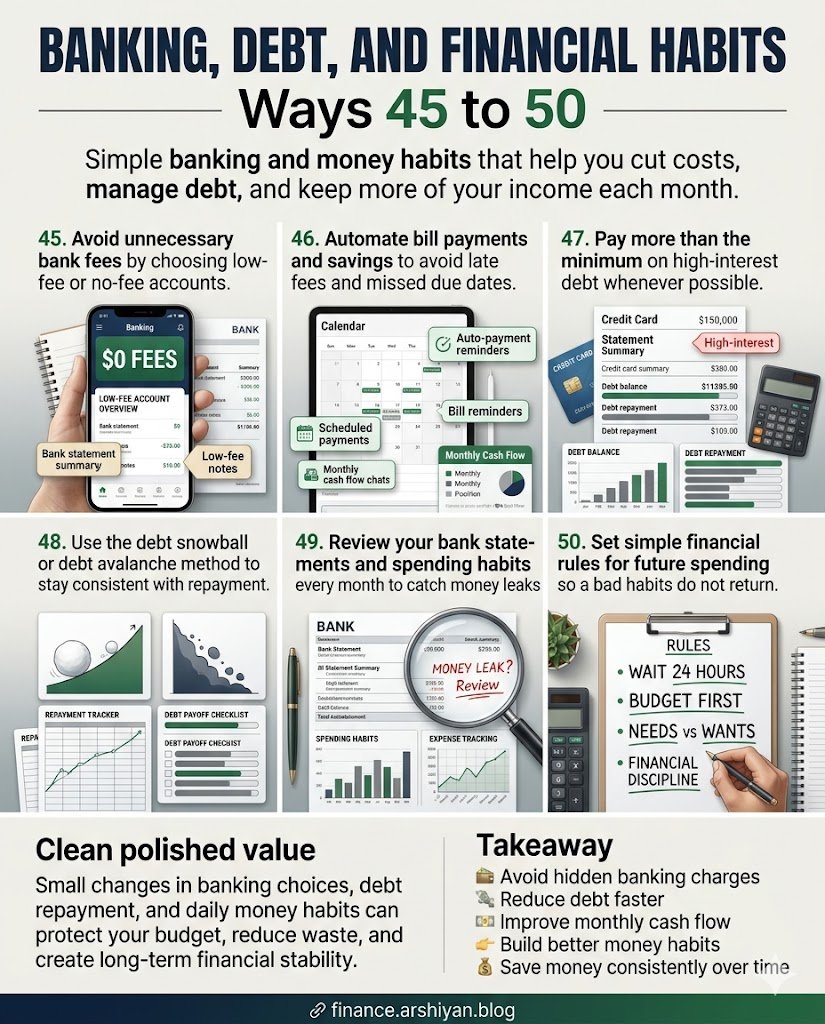

Banking, Debt, and Financial Habits (Ways 45 to 50)

45. Move your savings to a high-yield account. Traditional bank savings accounts in the U.S. pay as little as 0.01% interest. High-yield savings accounts at Marcus by Goldman Sachs, Ally Bank, or SoFi have been offering 4% or higher in recent years. If you have $5,000 sitting in a regular savings account, you are leaving roughly $200 per year on the table.

46. Eliminate bank fees entirely. Monthly maintenance fees, out-of-network ATM fees, overdraft fees — these are not fixed costs of life. Credit unions and online banks like Chime and Ally charge none of them. Switching accounts takes about 30 minutes and can save $150 to $200 per year.

47. Pay all bills on time, every time. Late fees on credit cards are typically $25 to $40 per incident. Beyond the fees, a single late payment can drop your credit score by 50 to 100 points, which raises the interest rate on future loans. Set autopay for at least the minimum on every account — you can always pay more manually.

48. Transfer high-interest credit card balances strategically. If you carry a balance on a high-rate credit card, a 0% balance transfer card can freeze interest charges for 12 to 21 months. This gives you a window to pay down principal without the interest charge compounding. Cards from Citi and Wells Fargo regularly offer these promotional periods. Read the transfer fee terms carefully before moving forward.

49. Stop paying for things you can get free at your bank. Notary services, cashier’s checks, wire transfers, safe deposit boxes — many of these are free or deeply discounted for account holders at credit unions and some full-service banks. Ask your bank what they actually offer before paying elsewhere.

50. Set a weekly “money date” with yourself. This one sounds soft, but it is arguably the most powerful habit on this list. Spending ten minutes every week reviewing your accounts, checking your budget, and seeing where you stand keeps you connected to your financial reality. People who look at their money regularly make better decisions with it. That is not an opinion — it is supported by behavioral finance research consistently.

Real-World Case Studies

Case Study 1: The Patterson Family — Freeing Up $620 Per Month in Georgia

Source: Consumer Financial Protection Bureau (CFPB) community success stories, 2023

Jason and Renee Patterson, a couple in Savannah with three kids, felt constantly squeezed even with two incomes. They sat down with a CFPB-partnered housing counselor in early 2022 and did a full expense audit together.

The findings were not dramatic. They found a gym membership nobody was using ($48), two streaming services they had forgotten about ($27), an auto insurance policy that had not been re-shopped in four years (saved $310 by switching to Geico), and a thermostat they were heating to 72 degrees all winter instead of programming it down at night. When they moved their emergency fund to a high-yield savings account at Ally Bank, they also started earning $180 more per year in interest.

Total monthly savings: approximately $620. They did not cut a single thing they actually cared about.

Case Study 2: Priya Mehta — A Single Professional in Chicago Saving $430 Monthly

Source: NerdWallet reader story compilation, 2024

Priya, a 29-year-old marketing manager, felt her paycheck evaporating without explanation every month. She started using YNAB and found that her subscriptions were costing her $214 per month — more than double what she thought she was spending. She rotated streaming services, dropped an unused app subscription, and switched her phone plan from Verizon to Mint Mobile.

She also started using Ibotta for groceries and moved from dining out five nights per week to two, cooking on the others using a simple meal prep routine on Sundays. She switched her savings to Marcus by Goldman Sachs, where she earned 4.5% APY at the time.

Her total spending dropped by $430 per month. She used the freed-up money to pay off a $5,200 credit card in 13 months.

Common Mistakes People Make When Cutting Expenses

Mistake 1: Trying to cut everything at once. Overhauling your entire financial life in one weekend is the budgeting equivalent of starting a crash diet. You feel motivated for ten days and then you are raiding the vending machine at midnight. Pick five to eight changes, live with them for a month, then add more.

Mistake 2: Cutting things you genuinely love. If morning coffee from your local shop is the best part of your Tuesday, cutting it to save $6 will make you miserable and resentful. Find the things you spend money on that bring little joy — those are the ones to cut first.

Mistake 3: Ignoring the big wins for the small ones. Making your own coffee saves $1,500 a year if you drink it every day at a cafe. But re-shopping insurance saves that in one afternoon phone call. People obsess over tiny cuts and ignore the categories where real money is hiding. Housing, transportation, insurance, and food are the four biggest expense categories for American households. That is where the serious leverage lives.

Mistake 4: Not tracking anything. Cutting expenses without tracking is like dieting without ever stepping on a scale. You have no idea if it is working. At minimum, check your total monthly spending once a week.

Mistake 5: Giving up after one bad month. Unexpected expenses happen. A car repair, a medical bill, a birthday you forgot was coming. One bad month does not mean the system failed. It means life happened. Reset and keep going.

Tools and Apps to Track and Reduce Spending

YNAB (You Need a Budget): The gold standard for active budgeters. It uses a zero-based budgeting system where every dollar is assigned a job. Available on iOS, Android, and desktop. Subscription costs around $14.99 per month, but most serious users report saving far more than that within the first two months.

Mint (now integrated into Credit Karma): Free, automatic, and good for people who want a passive view of their spending. It categorizes transactions automatically and sends alerts when you go over budget in a category.

Rocket Money: Specializes in finding and canceling unused subscriptions. The free tier shows you your subscriptions; the premium tier ($6 per month) will negotiate bills on your behalf. Worth every cent for people who hate making phone calls.

GoodRx: Free app and website for comparing prescription drug prices at pharmacies near you. Works on iOS and Android and does not require insurance.

Honey: Free browser extension that automatically finds and applies coupon codes at checkout. Works on Chrome, Firefox, and Edge.

Personal Capital (now Empower): Best for people who want to track net worth, investments, and spending in one place. Free for the basic tools.

Frequently Asked Questions

Q: How much can a typical American realistically save per month with these changes? According to data from the Bureau of Labor Statistics Consumer Expenditure Survey, the average American household has meaningful room to reduce spending in utilities, food, and subscriptions alone. Most people who do a thorough audit report finding $200 to $600 per month without cutting anything they truly value.

Q: Is it better to cut small expenses or focus on big ones first? Focus on the big ones first. Housing, transportation, food, and insurance account for roughly 65% of the average American household’s spending, according to the BLS. A single change in one of these categories can outperform twenty small cuts combined.

Q: How do I cut expenses without my spouse or partner being on board? Start with data, not lectures. Pull up a bank statement and go through it together without assigning blame. Frame it as a shared project with a shared goal — a vacation, paying off a debt, saving for a house — rather than a restriction being imposed on anyone.

Q: What is the fastest way to free up money in a single month? Call your insurance company and your internet provider and ask for better rates. Cancel any subscription you have not used in 30 days. Move your savings to a high-yield account. These three actions can often free up $100 to $400 in a single afternoon with minimal lifestyle change.

Q: Can I cut expenses and still have fun? Yes, and if the answer were no, nobody would ever stick to a budget. The strategies in this article are specifically designed to preserve quality of life while reducing the invisible spending that most people never notice anyway.

Sources Used in This Article

- U.S. Department of Energy — Thermostat and home energy savings data (energy.gov)

- USDA Economic Research Service — Food waste and household spending data

- Bureau of Labor Statistics — Consumer Expenditure Survey, 2024 edition (bls.gov)

- Consumer Financial Protection Bureau (CFPB) — Community financial success stories (consumerfinance.gov)

- C+R Research — Subscription spending survey, 2024

- NerdWallet — Reader money success story compilation, 2024 edition

- Journal of Consumer Research — Grocery shopping behavior and planning study

- GoodRx — Prescription savings data and pharmacy pricing reports (goodrx.com)

Helpful Next Steps

Here is what I want you to do before you close this tab and go back to your life as it was before.

Open your most recent bank statement and your most recent credit card statement. Spend ten minutes — just ten — going through every charge. Highlight anything recurring that you did not consciously choose this month. That is your starting list.

Next, pick five things from this article that feel easy. Not the hardest ones. Not the ones that require the most discipline right now. Five that seem nearly painless. Do those first.

Then, one month from today, look at your spending again. Compare it to last month. That comparison, those real numbers, will tell you more than any article ever could. And it will show you that you are more capable of managing your money than you probably give yourself credit for.

You do not have to deprive yourself. You just have to pay attention.

This article is written for educational purposes only. Individual results will vary based on income, location, and existing spending habits. Consult a certified financial planner for personalized guidance.