How to Build an Emergency Fund from Scratch

How to Build an Emergency Fund from Scratch

I remember the exact moment I realized I was one flat tire away from financial disaster. It was a Tuesday evening in March 2019, and my car made a sound no car should ever make. The repair estimate came in at $840. I had $63 in my savings account. That night, I sat in a parking lot staring at my phone, scrolling through credit card options with a knot in my stomach the size of a bowling ball.

That was my wake up call. Not a blog post, not a podcast, not some motivational quote on Instagram. A busted radiator hose and the gut punch of having absolutely nothing to fall back on.

If you’re reading this with little or nothing saved, I get it. I’ve been exactly where you are. And I want to walk you through how I went from $63 to a fully funded emergency fund in about 14 months, including every stumble and shortcut I discovered along the way.

Why an Emergency Fund Isn’t Optional

Let me be blunt. An emergency fund is not a luxury for people who have their lives figured out. It’s the single most important financial safety net you can build, and the lack of one is what keeps millions of people trapped in cycles of debt.

A 2024 report by Bankrate revealed that only 44% of Americans could cover an unexpected $1,000 expense from their savings. The rest would need to borrow, use a credit card, or scramble to find the money somewhere. That statistic isn’t just a number. It represents real people facing real panic when a medical bill shows up or a job disappears without warning.

The Federal Reserve’s Survey of Household Economics and Decisionmaking painted a similar picture. Roughly 37% of adults said they would struggle to handle a $400 emergency expense. Four hundred dollars. That’s a minor car repair, a trip to urgent care, or a broken appliance.

An emergency fund changes the entire equation. It turns a crisis into an inconvenience. It lets you sleep at night knowing that life’s inevitable surprises won’t send you spiraling into credit card debt or borrowing from relatives.

How Much Do You Actually Need?

You’ve probably heard the advice to save three to six months of living expenses. That’s solid guidance for a fully built fund, but if you’re starting from zero, that number can feel paralyzing. It’s like someone telling you to climb Everest when you haven’t even laced up your hiking boots.

So forget the big number for now. Your first target is $1,000. That’s it. One thousand dollars sitting in an account you don’t touch unless something genuinely unexpected happens.

Why $1,000? Because it covers the most common financial emergencies people face. A car repair, a medical copay, a busted water heater, a last minute flight for a family emergency. It won’t cover everything, but it handles the hits that send most people reaching for plastic.

Once you hit $1,000, then you start building toward one month of essential expenses. Then two months. Then three. Think of it like planting a garden. You don’t harvest tomatoes the week you put seeds in the ground. You water consistently, and eventually the growth surprises you.

Step One: Figure Out Where Your Money Is Actually Going

Before you can save anything, you need to know where your cash disappears to every month. And I promise, it’s disappearing somewhere you don’t expect.

When I first tracked my spending, I was convinced I didn’t have any room to save. I was wrong. I found $11.99 going to a streaming service I hadn’t opened in four months. Another $9.99 for a meditation app I used exactly twice. I was spending about $185 a month on coffee shop visits and takeout lunches that I barely remembered eating.

Here’s what I did. I pulled up my bank statements for the previous 60 days and went through every single transaction. I highlighted anything that wasn’t a fixed bill or a true necessity. It was uncomfortable, kind of like stepping on a scale after the holidays, but it gave me a clear picture.

You can use apps like Mint (now part of Credit Karma), PocketGuard, or even a plain notebook. The tool doesn’t matter as much as the honesty. Be ruthless with yourself for those 60 days of data. You’re not judging your past choices. You’re finding opportunities hiding in plain sight.

Step Two: Open a Separate Savings Account

This step sounds simple, and it is, but skipping it is one of the biggest mistakes people make. If your emergency fund sits in the same checking account you use for daily spending, it will get spent. Not because you’re irresponsible, but because money that’s visible and accessible tends to find a purpose.

Open a high yield savings account at a separate bank. I use Ally Bank, but Marcus by Goldman Sachs, Discover, and Capital One 360 are all solid options. As of early 2025, many of these accounts offer interest rates between 4% and 5% APY, which means your money actually grows while it sits there.

The key is separation. When your emergency fund is at a different institution than your everyday checking, there’s a built in speed bump. It takes one to two business days to transfer money, which gives you time to ask, “Is this really an emergency?”

Name the account something specific. Don’t just call it “Savings.” Call it “Emergency Fund” or “Do Not Touch” or “Flat Tire Insurance.” When it has a name, it has a purpose, and that makes it psychologically harder to raid.

Step Three: Automate a Small Amount Immediately

The biggest myth about building an emergency fund is that you need to save large amounts. You don’t. You need to save consistently.

When I started, I set up an automatic transfer of $25 every Friday from my checking account to my Ally savings account. Twenty five dollars. That’s roughly the cost of a mediocre pizza delivery. I barely noticed it leaving my checking account, but after 10 weeks, I had $250 saved without thinking about it.

Most banks let you schedule recurring transfers. Set it up once and forget about it. If $25 feels like too much, start with $10. Even $5. The amount genuinely does not matter at the beginning. What matters is building the habit. You’re training your brain to treat saving as automatic, like paying rent or a phone bill.

After two months, I bumped my transfer to $40 per week. Three months later, $60. By the time I hit my $1,000 goal, the habit was so ingrained that increasing the amount felt natural rather than painful.

Step Four: Find Extra Money Without Getting a Second Job

I know, I know. “Find extra money” sounds like advice from someone who has never looked at an empty fridge. But hear me out. There are real, practical ways to squeeze cash out of your existing life without working yourself into the ground.

Sell what you’re not using. I made $430 in one weekend by listing old electronics, clothes, and furniture on Facebook Marketplace and OfferUp. That broken laptop collecting dust? Someone wants it for parts. Those jeans you haven’t worn since 2021? Someone will pay $15 for them.

Negotiate your bills. I called my internet provider and told them I was considering switching. They knocked $20 off my monthly bill for a year. That’s $240 saved without changing a thing about my lifestyle. The same approach works for insurance, phone plans, and subscription services.

Do a “no spend” challenge. For one week each month, I committed to spending nothing beyond absolute necessities. No eating out, no online shopping, no impulse buys. It felt restrictive the first time, almost like a financial fast. But it saved me around $120 to $150 each round, and it reset my spending habits in a surprisingly lasting way.

Use cashback apps on purchases you’d make anyway. Rakuten, Ibotta, and Fetch Rewards won’t make you rich, but they redirect small amounts back into your pocket. Over the course of a year, I earned about $180 in cashback just from groceries and household items I was already buying.

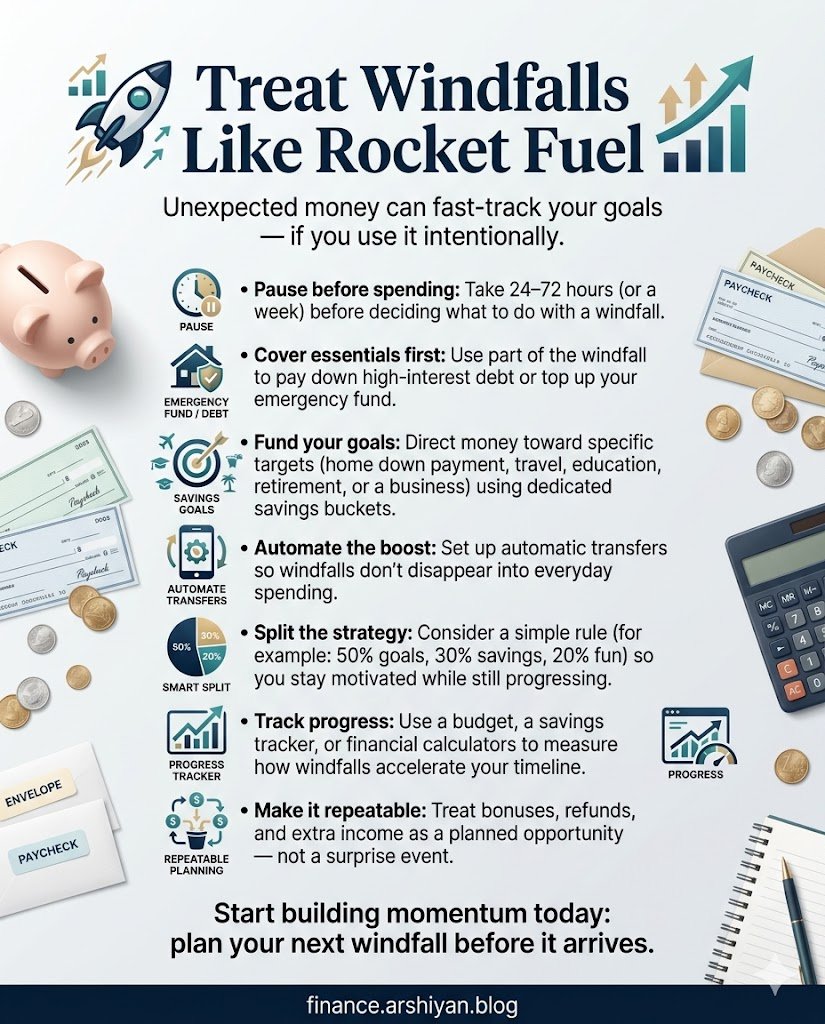

Step Five: Treat Windfalls Like Rocket Fuel

Tax refunds. Birthday cash. Bonuses at work. Rebate checks. The occasional $20 you find in a coat pocket from last winter.

Most people treat these as “bonus money” and spend them instantly. When you’re building an emergency fund, these windfalls are rocket fuel. They accelerate your progress in ways that regular weekly transfers can’t.

The year I got serious about my fund, I received a $1,600 tax refund. Old me would have spent it on new clothes or a weekend trip. Instead, I sent $1,200 straight to my emergency fund and gave myself $400 to enjoy guilt free. That single move jumped my balance forward by months.

You don’t have to be extreme about it. I’m not suggesting you live like a monk. But funneling even 50% to 75% of unexpected cash into your fund makes an enormous difference.

The Mistakes I Made (So You Don’t Have To)

Dipping into the fund for non emergencies. A concert is not an emergency. A sale at your favorite store is not an emergency. A craving for sushi is definitely not an emergency. I learned this the hard way after “borrowing” $200 for a weekend getaway. That $200 took me six weeks to rebuild. Define what counts as an emergency before you need the money, and write it down. Actual emergencies include job loss, medical expenses, urgent home or car repairs, and essential travel for family crises.

Trying to save too aggressively too fast. I once tried saving $200 a week on a $2,800 monthly income. I lasted three weeks before I was so strapped for daily cash that I resented the whole process. Slow and steady genuinely wins here. Pushing too hard leads to burnout and backlash spending.

Not celebrating milestones. When I hit my first $500, I barely acknowledged it. That was a mistake. Celebrating small wins keeps you motivated. Buy yourself a coffee. Tell a friend. Do a little victory dance in your kitchen. Whatever makes you feel like you accomplished something, because you did.

A Case Study Worth Knowing About

A 2022 study conducted by Commonwealth, a nonprofit focused on financial security, tested a program called SaverLife with over 50,000 participants. The program encouraged low to moderate income workers to save small amounts through automatic deposits and offered small incentives for consistent saving behavior.

The results were striking. Participants who saved just $25 per paycheck were 78% less likely to miss a bill payment after six months. More importantly, when unexpected expenses hit, savers in the program were far less likely to resort to payday loans or high interest credit cards compared to a control group. The study showed that even modest, consistent saving fundamentally changed how people handled financial shocks.

What stood out to me about this study is that it wasn’t about wealthy people or high earners. It focused on real families earning between $25,000 and $50,000 annually. People who thought they couldn’t afford to save proved themselves wrong with amounts as small as $10 to $25 per paycheck.

What Happens After You Hit Your Goal

Once you reach three to six months of expenses, your emergency fund is built. Congratulations. You’ve accomplished something that most people never do. But don’t just let that money sit there forever without a plan.

Review your fund once or twice a year. Has your rent gone up? Have your expenses changed? Adjust the target amount accordingly. Keep the fund in a high yield account so inflation doesn’t silently eat away at its value.

And then, here’s the beautiful part, redirect that savings habit toward other goals. You’ve already proven to yourself that you can set money aside consistently. Now aim it at retirement contributions, a house down payment, an investment account, or whatever dream has been sitting on the shelf waiting for its turn.

The discipline you built creating your emergency fund doesn’t disappear. It becomes the foundation for everything else.

Frequently Asked Questions

How long does it take to build an emergency fund? It depends entirely on your income and how much you can set aside. Saving $25 per week gets you to $1,300 in a year. Saving $50 per week puts you at $2,600. Most people can build a solid starter fund of $1,000 within three to six months if they stay consistent and redirect any extra cash they come across.

Should I pay off debt first or build an emergency fund? Both, but start with a small emergency cushion. Having even $500 to $1,000 saved prevents you from going deeper into debt when surprises pop up. Once that starter fund is in place, attack your highest interest debt aggressively while maintaining the cushion.

Where should I keep my emergency fund? A high yield savings account at an online bank is the sweet spot. It earns interest, stays accessible within one to two business days, and remains separate from your daily spending. Avoid keeping it in a checking account, under your mattress, or in any investment account where the value can drop.

What counts as a real emergency? Job loss, unexpected medical bills, essential car or home repairs, and emergency travel for family crises. A new phone because yours has a cracked screen? Probably not, unless you genuinely cannot function without it. A good test is asking yourself, “Will waiting 30 days make this situation significantly worse?” If the answer is no, it’s likely not an emergency.

Can I build an emergency fund on a low income? Absolutely. The Commonwealth SaverLife study demonstrated that people earning well below the median income successfully built savings with amounts as small as $10 per paycheck. The key is consistency, not size. Automate whatever you can, even if it’s $5 a week, and increase the amount whenever your situation allows.

Should I invest my emergency fund? No. Emergency funds need to be liquid and stable. Investing in stocks, crypto, or anything with market volatility defeats the purpose. If the market drops 30% the same week your furnace dies, you’ll be in worse shape than if you had no fund at all. Keep it boring. A savings account earning 4% to 5% is plenty.

What if I keep dipping into my emergency fund for non emergencies? This is common, and it usually means the fund is too easy to access or you haven’t clearly defined what qualifies as an emergency. Move the account to a separate bank, remove the app from your phone’s home screen, and write a short list of approved emergency categories. Some people even keep a sticky note on their debit card as a physical reminder.

The Part Nobody Tells You

Building an emergency fund isn’t exciting. Nobody throws you a party when you hit $2,000 in savings. There’s no dramatic before and after photo. It’s quiet, unglamorous work that happens in the background of your regular life.

But the feeling of security it gives you is worth more than almost any purchase I’ve ever made. The first time I faced an unexpected $600 car repair after building my fund, I paid it, shrugged, and moved on with my week. No panic. No credit card applications. No calling my parents. Just a minor inconvenience handled by a system I’d built one small transfer at a time.

That peace of mind? You can’t put a price tag on it. But you can build it, starting today, with whatever you’ve got.