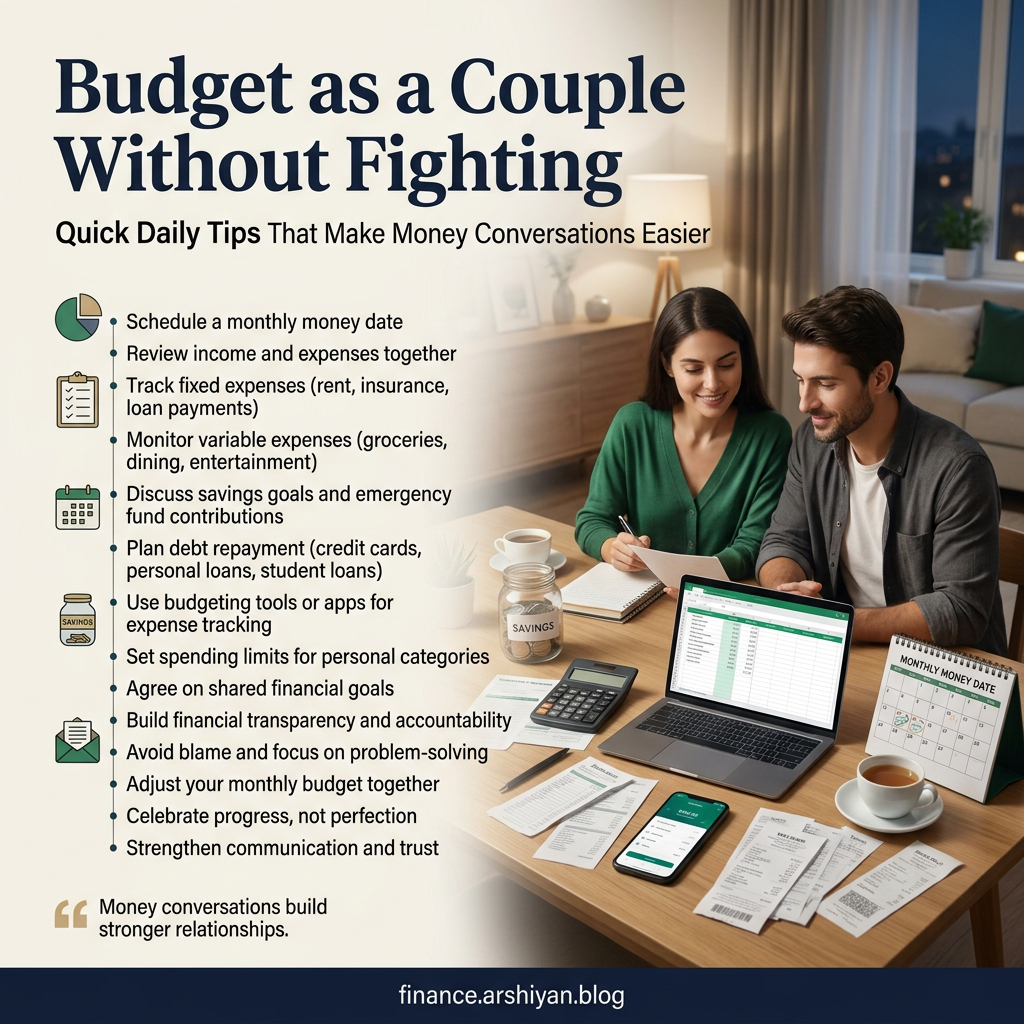

How to Budget as a Couple Without Fighting About Money

How to Budget as a Couple Without Fighting About Money

My wife and I had our worst argument ever over a $47 pizza order. Not because we couldn’t afford it, but because neither of us knew where our money was actually going. That fight wasn’t really about pizza. It was about fear, control, and the fact that we had zero system for managing our finances together.

That was six years ago. Since then, we’ve paid off $23,000 in combined debt, built a proper emergency fund, and learned to talk about money without someone sleeping on the couch. None of it happened overnight, and we made plenty of mistakes along the way. But I can honestly say that figuring out how to budget together saved more than just our bank account.

If you and your partner keep butting heads over spending, bills, or saving goals, this guide is for you. Not the textbook version. The real, messy, “we’ve been there” version.

Why Money Fights Happen (and Why They’re Rarely About Money)

Before you open a spreadsheet or download an app, you need to understand something. Most couples who fight about money aren’t actually fighting about money. They’re fighting about values, priorities, and sometimes childhood baggage they’ve never unpacked.

One partner grew up in a household where every penny was watched. The other grew up where money was never discussed at all. Put those two people together and ask them to split a grocery bill, and you’ve got a recipe for tension.

A 2023 study by Ramsey Solutions found that money is the number one issue married couples argue about. They surveyed over 1,000 adults in committed relationships and discovered that couples who said they had a “great” marriage were almost twice as likely to talk about money daily or weekly compared to couples who described their marriage as “okay” or “in crisis.” The takeaway wasn’t that happy couples never disagree. It was that they kept the conversation open.

So the first step isn’t making a budget. It’s having an honest conversation about your relationship with money itself.

Step One: Have “The Money Talk” Before You Touch a Single Number

Sit down with your partner, no phones, no distractions, maybe with a cup of coffee or tea, and take turns answering these questions:

What did money look like in your house growing up? Were your parents open about finances, or was it a secret? What scares you most about money right now? What does financial security look like to you? Is there any debt you haven’t told me about?

That last question is a big one. A National Endowment for Financial Education survey found that roughly 43% of adults in relationships admitted to some form of financial deception with their partner. Sometimes it’s a hidden credit card. Sometimes it’s a student loan they’re embarrassed about. Getting everything on the table, without judgment, is the foundation everything else gets built on.

When my wife and I had this conversation, I learned she’d been carrying $4,500 in credit card debt she felt too ashamed to mention. I wasn’t angry. I was relieved she told me. And it completely changed how we approached our plan.

Step Two: Pick a Budgeting Style That Fits Both of You

Here’s where most couples go wrong. One person Googles “best budgeting method,” picks one, and tries to force their partner into it. That almost never works.

Instead, look at a few options together and pick something you both feel comfortable with.

The Percentage Method is the simplest starting point. You take your combined take home pay and divide it roughly into categories. About 50% goes to needs like rent, groceries, utilities, and insurance. Around 30% covers wants like dining out, hobbies, and entertainment. The remaining 20% is directed toward savings, investments, and paying down debt. This is flexible and doesn’t require tracking every single purchase, which works well for couples where one person hates being micromanaged.

Zero Based Budgeting means every dollar gets a job before the month starts. Income minus all planned expenses equals zero. This works great for couples who want tight control and are both willing to plan ahead. It takes more effort but leaves very little room for surprises.

The Envelope System is old school but effective. You withdraw cash for variable categories like groceries, entertainment, and clothing, and put each amount in a labeled envelope. When the envelope is empty, you’re done spending in that category. Some couples swear by this because the physical act of handing over cash feels different than tapping a card.

My wife and I started with the percentage method because it was less intimidating. After a year, once we got comfortable, we shifted toward zero based budgeting. There’s no rule that says you have to pick one and stick with it forever.

Step Three: Choose a Tool You’ll Both Actually Use

The best budgeting tool is the one both of you will open more than once. I’ve seen couples buy fancy planners that collect dust, or sign up for apps they never log into after the first week.

Here are some tools that real couples use and stick with:

YNAB (You Need A Budget) is excellent for couples who want to be hands on. It follows the zero based approach and lets you link accounts, set goals, and see everything in one place. It costs about $14.99 per month, but many users say it pays for itself within the first month because of how much awareness it creates.

Goodbudget is a digital version of the envelope system. It’s free for basic use and works well if one of you prefers simplicity. You don’t link bank accounts, which some people actually prefer for privacy reasons.

Google Sheets is what we used for the first two years. Free, customizable, and accessible from any device. We created a shared spreadsheet with tabs for each month. Nothing fancy, just columns for income, fixed expenses, variable spending, and savings. It worked because we could both edit it in real time.

Honeydue is built specifically for couples. It lets you see shared accounts, split bills, set spending limits, and even send each other emoji reactions on purchases. It adds a lighthearted touch to something that can feel heavy.

Whatever you pick, the key is that both partners have access and both partners use it. A budget that lives in only one person’s head isn’t a shared budget. It’s a dictatorship.

Step Four: Set Up “Yours, Mine, and Ours” Accounts

This is the structure that saved us from 90% of our arguments.

We have three accounts. One joint checking account for all shared expenses like rent, groceries, utilities, insurance, and savings goals. Then we each have a personal spending account.

Every payday, our agreed upon contributions go into the joint account first. Whatever is left in our personal accounts is ours to spend however we want, no questions asked.

This means if my wife wants to spend $60 on candles that smell like a forest in autumn, that’s her call. And if I want to buy a ridiculously overpriced board game, nobody bats an eye. Personal spending money removes the need to justify every small purchase, which eliminates a huge source of friction.

Dave and Rachel, a couple from Austin, Texas, shared their experience on the EveryDollar community forum. They’d been fighting weekly over “unnecessary” purchases until they set up separate fun money accounts with $150 each per month. Dave wrote, “It’s like we gave each other permission to be human.” They reported that their money arguments dropped from several times a week to maybe once a month.

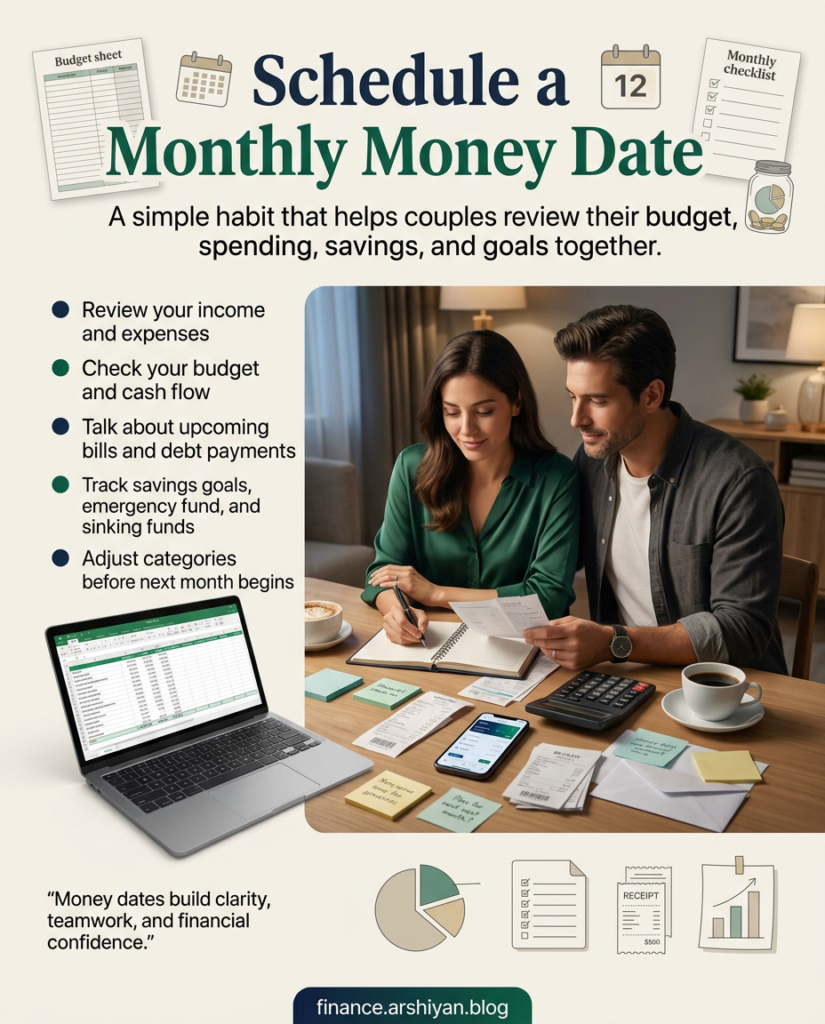

Step Five: Schedule a Monthly Money Date

This sounds cheesy, and it kind of is, but it works better than almost anything else.

Pick one evening a month. Order takeout or make a nice dinner. Pour a glass of whatever you like. Then sit down and review the past month together.

Go through what you spent, what you saved, what surprised you, and what you want to adjust. Celebrate the wins, even small ones. Paid off a credit card? That’s worth a toast. Stayed under budget on groceries? High five.

The goal is to make this feel like a team meeting, not a courtroom. Nobody is on trial. You’re both looking at the same numbers and figuring out the next move together.

We do ours on the last Sunday of every month. It takes about 30 to 45 minutes. Sometimes we realize we overspent on eating out. Sometimes we find extra money we can throw at a savings goal. Either way, it keeps us aligned and prevents small issues from snowballing into big blowups.

Common Mistakes Couples Make (and How to Dodge Them)

Keeping score. “I make more, so I should have more say.” This attitude poisons everything. A budget works when both people feel equal ownership, regardless of income differences. If one person earns significantly more, consider contributing proportionally rather than equally. Someone making $70,000 and someone making $40,000 don’t need to split bills 50/50 to be fair.

Being too strict too fast. Going from zero budgeting to tracking every cent overnight is like going from the couch to running a marathon. Start with broad categories. Tighten up gradually. Give yourselves grace in the first three months.

Not accounting for irregular expenses. Car registration, annual subscriptions, holiday gifts, vet bills. These are predictable even though they don’t happen monthly. Estimate the annual cost and divide by 12. Set that amount aside each month in a sinking fund. This one change alone prevented more arguments for us than anything else.

Avoiding the topic entirely. Silence around money isn’t peace. It’s a pressure cooker. The couples who never talk about finances tend to have the biggest explosions when something finally goes wrong.

What to Do When You Still Disagree

You will disagree. That’s normal and even healthy. The question is how you handle it.

A few ground rules that have served us well: Never make a financial decision over a certain amount without discussing it first. For us, that number is $100. You might set yours at $50 or $200. The exact figure matters less than the agreement itself.

If you reach an impasse, table it. Seriously. Sleep on it. Revisit the topic in 48 hours with fresh eyes. Most financial decisions aren’t emergencies, even when they feel like one in the moment.

And if money fights are frequent, intense, or connected to deeper relationship issues, consider seeing a financial therapist. Yes, that’s a real thing. The Financial Therapy Association has a directory of certified professionals who specialize in the emotional and relational side of money. It’s not just for couples in crisis. It’s for anyone who wants to build a healthier dynamic around finances.

A Real World Case Study That Might Sound Familiar

Marcus and Leah, a couple profiled by NerdWallet in their “Couples and Money” series, had a combined income of about $95,000 but were living paycheck to paycheck. Leah was a saver by nature. Marcus was a spender who didn’t see the harm in small daily purchases. Their fights were constant.

They started with one change: tracking every purchase for 30 days without trying to cut anything. Just observing. At the end of the month, Marcus was stunned to see he’d spent over $600 on convenience store runs, coffee shops, and impulse buys. Leah realized she’d been hoarding money in a savings account while ignoring a high interest credit card balance.

That single month of awareness led them to restructure everything. Within 18 months, they’d paid off $11,000 in debt and started contributing to retirement accounts. Marcus still buys his coffee, but now it comes from a designated “no guilt” spending category. Leah still saves aggressively, but she directs it strategically.

The lesson? Awareness comes before change. And change works best when it doesn’t feel like punishment.

Quick Tips That Make Daily Life Easier

Use round numbers when budgeting. Saying “we’ll spend around $500 on groceries” is easier to remember and track than $487.32.

Automate everything you can. Set up auto transfers to savings, auto pay for bills, and auto contributions to retirement. The less you have to manually decide each month, the fewer opportunities there are for disagreement.

Keep a “wish list” instead of impulse buying. When either of you wants something that’s not in the budget, write it down. Revisit the list during your monthly money date. If you still want it and can afford it, go for it. You’d be surprised how many things lose their shine after a few weeks.

Thank each other. It sounds small, but saying “hey, I noticed you packed lunch all week instead of eating out, that’s awesome” goes a long way. Positive reinforcement beats nagging every single time.

Frequently Asked Questions

Should couples combine all their finances or keep everything separate? There’s no single right answer. Many couples do well with a hybrid approach: a joint account for shared responsibilities and individual accounts for personal spending. The key is transparency. Whatever structure you choose, both partners should know the full financial picture.

How do you budget together when one person earns much more than the other? Proportional contributions tend to feel fairer than a straight 50/50 split. If one person makes 60% of the household income, they contribute 60% to shared expenses. This way, both partners have a similar percentage of personal money left over.

What if my partner refuses to budget at all? Start by asking why. Sometimes resistance comes from anxiety, past trauma, or feeling controlled. Try starting small with just one goal you both care about, like a vacation fund. Once they see the benefit, the resistance often fades. If it doesn’t, a financial counselor can help facilitate the conversation.

How often should couples review their budget? Once a month is the sweet spot for most people. Weekly check ins work for couples paying off debt aggressively. Less than monthly tends to let things drift too far off track.

What’s the best free budgeting app for couples? Goodbudget and Honeydue are both strong free options. Google Sheets is also completely free and gives you total control over the format. The best app is whichever one both of you will consistently use.

How do you handle unexpected expenses without fighting? Build an emergency fund together, even if it starts small. Having even $500 to $1,000 set aside takes the panic out of surprise car repairs or medical bills. When you have a cushion, unexpected costs become inconveniences instead of crises.

Is it okay to have financial secrets from your partner? Small surprises like saving for a birthday gift are fine. But hiding debt, secret accounts, or major purchases erodes trust and usually makes problems worse over time. Honesty is always the cheaper option.

One Last Thought

Budgeting as a couple isn’t about perfection. It’s about partnership. You’ll have months where everything goes according to plan and months where life throws you a curveball that wrecks your spreadsheet. That’s okay.

What matters is that you keep showing up to the conversation. That you treat each other as teammates, not opponents. And that you remember the pizza isn’t really about the pizza. It never was.

Start where you are. Use what you have. Talk more than you think you need to. And give each other the kind of grace you’d want for yourself on your worst financial day.

That’s how you budget without the battles.