How to Budget on a Low Income Without Losing Your Mind

How to Budget on a Low Income Without Losing Your Mind

I remember sitting at my kitchen table with a stack of bills, a calculator, and a growing sense of dread. My paycheck had just hit the bank, and after rent, it felt like trying to fill a swimming pool with a garden hose. If you have ever stared at your bank balance and wondered how the math could possibly work, trust me, you are not alone.

Budgeting on a tight income is not about deprivation. It is about giving every single dollar a job so you stop feeling like money controls you. Over the years, I have made plenty of mistakes, tried dozens of methods, and slowly figured out what actually sticks when your earnings are modest. This is everything I wish someone had told me when I was starting out.

Why Most Budgeting Advice Falls Flat for Low Earners

Here is the thing that frustrated me for years: most financial advice is written by people who have never had to choose between groceries and a phone bill. “Just save 20% of your income!” they say, as if it were as easy as flipping a light switch. When your paycheck barely covers necessities, the standard 50/30/20 rule can feel like a cruel joke.

A 2022 report by the Urban Institute found that nearly 40% of American adults would struggle to cover an unexpected $400 expense. That is not a character flaw. That is a systemic reality. So instead of pretending you can follow textbook formulas, let us build something that fits your actual life.

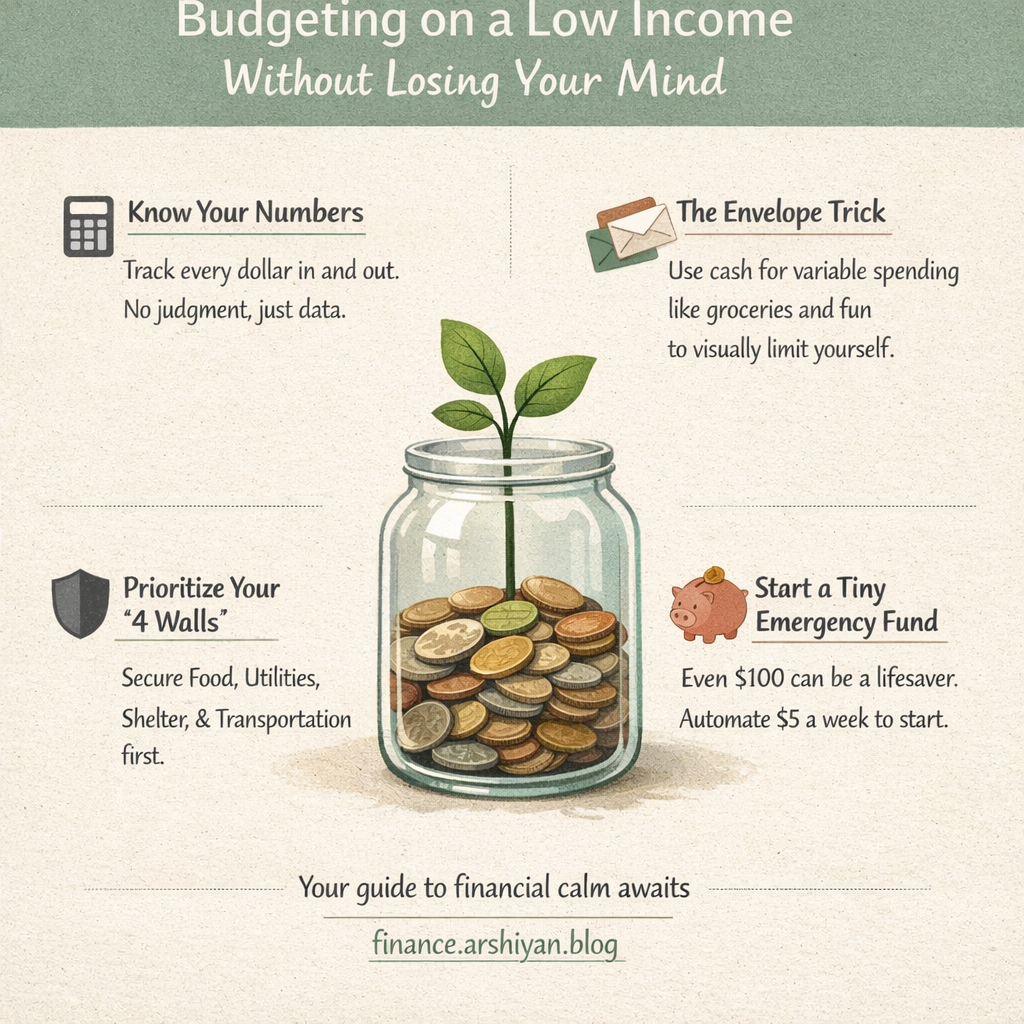

Step One: Know Exactly Where Your Money Goes

Before you can fix a leaky bucket, you need to find the holes. For one full month, track every penny you spend. And I mean every penny, the morning coffee, the impulse bag of chips at the gas station, the subscription you forgot about.

I started by simply keeping a small notebook in my back pocket. Every purchase got scribbled down. It was eye opening. I discovered I was spending almost $45 a month on vending machine snacks at work, money that was basically evaporating into thin air.

If pen and paper is not your style, free apps like Mint (now Credit Karma) or the EveryDollar app work well. EveryDollar is especially useful because it follows a zero based budget model, which we will get to in a moment.

How to track for one month:

- Collect every receipt and keep them in an envelope or snap a photo.

- At the end of each day, log your spending in a notebook or app.

- Categorize everything: rent, utilities, groceries, transportation, entertainment, personal care, and miscellaneous.

- At month’s end, add up each category and look at the total with fresh eyes.

You might be surprised. Most people are.

Step Two: Separate the Must Haves from the Nice to Haves

Once you see where the money goes, it is time to get honest. Ruthlessly honest. Divide your expenses into two columns: essentials and everything else.

Essentials are the things that keep a roof over your head and food on your plate. Rent, utilities, basic groceries, transportation to work, minimum debt payments, and necessary medications. Everything else, streaming services, dining out, gym memberships, new clothes, falls into the second column.

Now, I am not saying you should live like a monk. Cutting out every small pleasure is a recipe for burnout and budget abandonment. But you need to see the full picture before making choices.

When I did this exercise, I realized I was paying for three streaming services and only regularly watching one. Cancelling two of them freed up $25 a month. That does not sound like much, but over a year it is $300, enough to cover a car repair or a modest emergency.

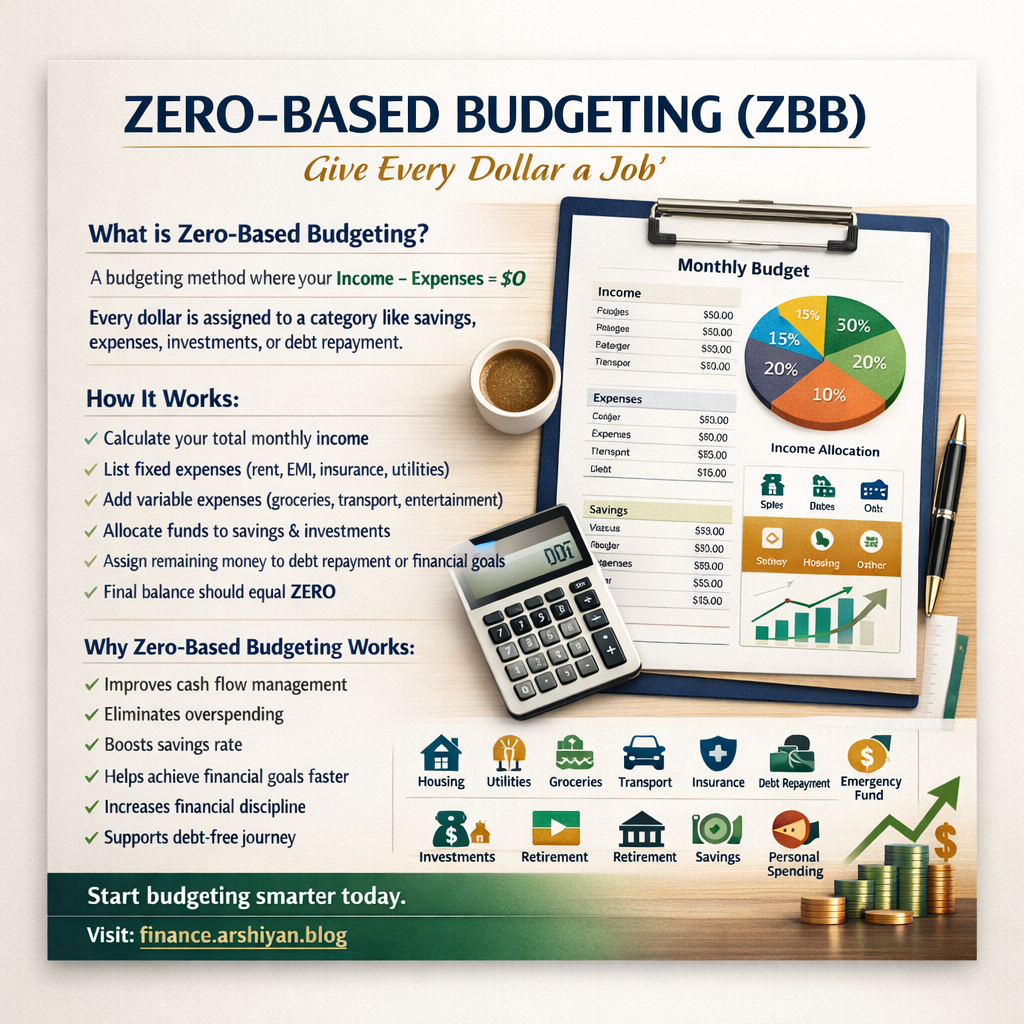

Step Three: Try the Zero Based Budget (It Changed My Life)

Of all the methods I have tried, zero based budgeting is the one that finally made things click. The concept is simple: your income minus your expenses should equal zero. Every dollar gets assigned to a category before the month begins. Not a single dollar is left floating around without a purpose.

Here is an example using a monthly take home pay of $1,800:

| Category | Amount |

|---|---|

| Rent | $650 |

| Utilities | $120 |

| Groceries | $250 |

| Transportation | $150 |

| Phone | $45 |

| Minimum debt payments | $100 |

| Personal care | $30 |

| Savings (even tiny amounts count) | $50 |

| Entertainment | $40 |

| Clothing | $25 |

| Miscellaneous buffer | $40 |

| Remaining assigned to debt or savings | $300 |

The magic is not in the specific numbers. It is in the intentionality. When you tell your money where to go beforehand, you stop wondering where it went afterward.

Dave Ramsey’s team popularized this method widely, and regardless of what you think about his other advice, the zero based approach has helped millions of people regain control. A Ramsey Solutions study found that people who budget consistently are 50% more likely to report feeling “in control” of their finances compared to those who do not.

Step Four: Use the Envelope System for Trouble Categories

Old school? Absolutely. Effective? Unbelievably so.

If you tend to overspend on groceries or eating out, withdraw the budgeted cash for that category and put it in a labeled envelope. When the envelope is empty, you are done spending in that category until next month. No negotiations, no “I will make it up next week.”

I used this for groceries and dining out for nearly two years. It felt strange at first, almost primitive in a world of tap to pay. But holding physical cash forced me to think twice before every purchase. There is something about watching bills leave your hand that a card swipe simply does not replicate.

If physical cash feels too inconvenient, apps like Goodbudget replicate the envelope system digitally. You create virtual envelopes and allocate your income across them.

Step Five: Attack Your Grocery Bill Strategically

Groceries are one of the most flexible categories in any budget, and also one of the easiest places to hemorrhage money. When I was at my tightest, I brought my grocery spending from $350 down to $200 a month for two people. Here is how.

Meal plan before you shop. Sounds tedious, but spending 20 minutes on Sunday planning the week’s meals prevents those desperate “what is for dinner” moments that lead to expensive takeout. I use a simple notepad, though apps like Mealime can generate plans with shopping lists automatically.

Buy store brands relentlessly. In most cases, store brand products are made in the same factories as name brands. Aldi and Lidl built entire empires on this principle. A jar of store brand pasta sauce might save you $1.50 compared to the national brand. Multiply that across 30 items and the savings are real.

Shop the sales cycle. Most grocery stores run sales on a predictable rotation, usually every 6 to 8 weeks. Stock up on non perishables when they hit their lowest price.

Embrace beans, rice, eggs, and frozen vegetables. These are nutritional powerhouses that cost pennies per serving. A bag of dried black beans, a bag of rice, a dozen eggs, and a bag of frozen broccoli can create meals for days. It is not glamorous, but it is honest eating that keeps both your body and your wallet in good shape.

Step Six: Trim Bills You Thought Were Fixed

People assume that bills like insurance, phone plans, and internet are set in stone. They are not. Almost everything is negotiable or replaceable.

Call your car insurance company and ask about discounts. Shop around every six months. I switched from a big name insurer to a smaller regional company and saved $60 a month for the same coverage.

Look at your phone plan. If you are paying $80 a month for a major carrier, consider prepaid options. Mint Mobile, Visible, or Tello often provide the same network coverage for $15 to $30 per month. I switched my family to Mint Mobile three years ago and have never looked back. The savings across two lines was roughly $100 per month.

For internet, call your provider and mention you are considering switching. Retention departments often have unadvertised deals. If that does not work, check whether a competitor offers a promotional rate. Even saving $20 a month adds up to $240 a year.

Step Seven: Build a Micro Emergency Fund First

Financial experts love to talk about three to six months of living expenses tucked away in savings. When you are earning $1,800 a month, that number feels absurd, like being told to climb Everest when you are still learning to walk uphill.

So start absurdly small. Aim for $500. Then $1,000. That is it.

A $1,000 emergency fund covers most of life’s common curveballs: a flat tire, an urgent dental visit, a broken appliance. According to a report from the Federal Reserve’s Survey of Household Economics and Decisionmaking, having even a small financial cushion dramatically reduces stress and prevents people from spiraling into high interest debt when something unexpected hits.

Automate this savings if you can. Set up an automatic transfer of even $10 or $20 per paycheck into a separate savings account. Out of sight, out of mind. I use a high yield savings account through Ally Bank, which earns a small return while keeping the money accessible.

The Mistakes I Made (So You Do Not Have To)

Mistake 1: Being too aggressive too fast. The first time I tried budgeting, I slashed everything to the bone. No eating out, no entertainment, no fun money at all. I lasted three weeks before going on a frustrated spending spree that wiped out a month of progress. Budgets need breathing room, even small amounts, or they snap like a rubber band pulled too tight.

Mistake 2: Not budgeting for irregular expenses. Oil changes, annual subscriptions, birthday gifts, back to school supplies. These are not surprises, but I treated them that way. Now I add up all my irregular annual expenses, divide by twelve, and set aside that amount each month in a “sinking fund” category.

Mistake 3: Comparing myself to others. Social media is a highlight reel. Watching friends post vacation photos while I was clipping coupons made me feel like a failure. But comparison is the thief of joy, and it is also the thief of financial progress. Everyone’s situation is different. The only race worth running is the one against your former spending habits.

A Real World Case Study: The Earn More, Save More Project

In 2019, researchers at Washington University in St. Louis conducted a study on low income families participating in a structured budgeting and savings program. Families earning below the federal poverty line were given access to matched savings accounts (where every dollar saved was matched by the program) and simple budgeting coaching.

After 18 months, participants had saved an average of $1,500, a life changing amount for families who previously had no safety net at all. More importantly, 70% of participants reported reduced financial anxiety and improved household stability. The study demonstrated that the barrier for low income families is not motivation or discipline. It is access to the right tools and a plan that respects their reality.

This mirrors what I have seen in my own experience and in the stories of friends and readers who have shared their journeys with me. Small, consistent steps beat grand gestures every single time.

Tools and Apps Worth Trying

You do not need anything fancy. But the right tool can make the process less painful.

EveryDollar (free version): Clean, simple zero based budgeting. You enter your income and assign every dollar. The free version requires manual entry, which some people actually prefer because it forces awareness.

Goodbudget: Digital envelope budgeting. Great for couples who want to share envelope balances across devices.

YNAB (You Need A Budget): This one costs about $14.99 per month (or $99 per year), so it is a harder sell on a tight budget. But they offer a 34 day free trial, and many users swear it pays for itself within the first month by changing spending behavior. They also offer free access for students.

A plain spreadsheet: Google Sheets is free and surprisingly powerful. You can build a custom budget tracker in an hour. There are hundreds of free templates available online.

Cash and envelopes: Zero cost. Maximum accountability. Sometimes the oldest tools are the sharpest.

When the Numbers Still Do Not Work

Sometimes, even after trimming and optimizing and tracking, the math still does not add up. If your income genuinely does not cover basic needs, that is not a budgeting failure. That is a signal that the income side of the equation also needs attention.

Explore whether you qualify for assistance programs. SNAP benefits, utility assistance through LIHEAP, Medicaid, and local food banks exist for exactly this reason. There is no shame in using resources that are designed to help. A study from the Center on Budget and Policy Priorities found that SNAP benefits alone lifted 3.4 million people out of poverty in a single year.

Simultaneously, even small income boosts can create margin. Selling unused items on Facebook Marketplace, doing occasional gig work through platforms like TaskRabbit, or picking up a few hours of freelance work can provide the breathing room your budget desperately needs.

The Mindset Shift That Makes It All Stick

Budgeting on a low income is as much a mental game as it is a mathematical one. The numbers matter, but so does how you talk to yourself about money.

Instead of thinking “I cannot afford that,” try reframing it as “that is not a priority right now.” The first phrase makes you feel powerless. The second puts you in the driver’s seat.

Celebrate small wins. Paid all your bills on time this month? That is worth acknowledging. Managed to put $25 into savings? You are building a habit that will serve you for the rest of your life. Financial health is not a destination you arrive at one day with trumpets and confetti. It is a direction you walk in, one step at a time, one month at a time.

I am not going to pretend that budgeting on a tight income is fun. Some months it feels like assembling a jigsaw puzzle where the pieces do not quite fit. But every month you stick with it, the picture gets a little clearer, the stress drops a little lower, and you sleep a little better knowing that you, not your bills, are the one calling the shots.

And honestly, that peace of mind is worth more than any dollar amount you will ever put in a spreadsheet.