Debt Free Living

Debt Free Living: How I Paid Off $47,000 and Finally Started Sleeping at Night

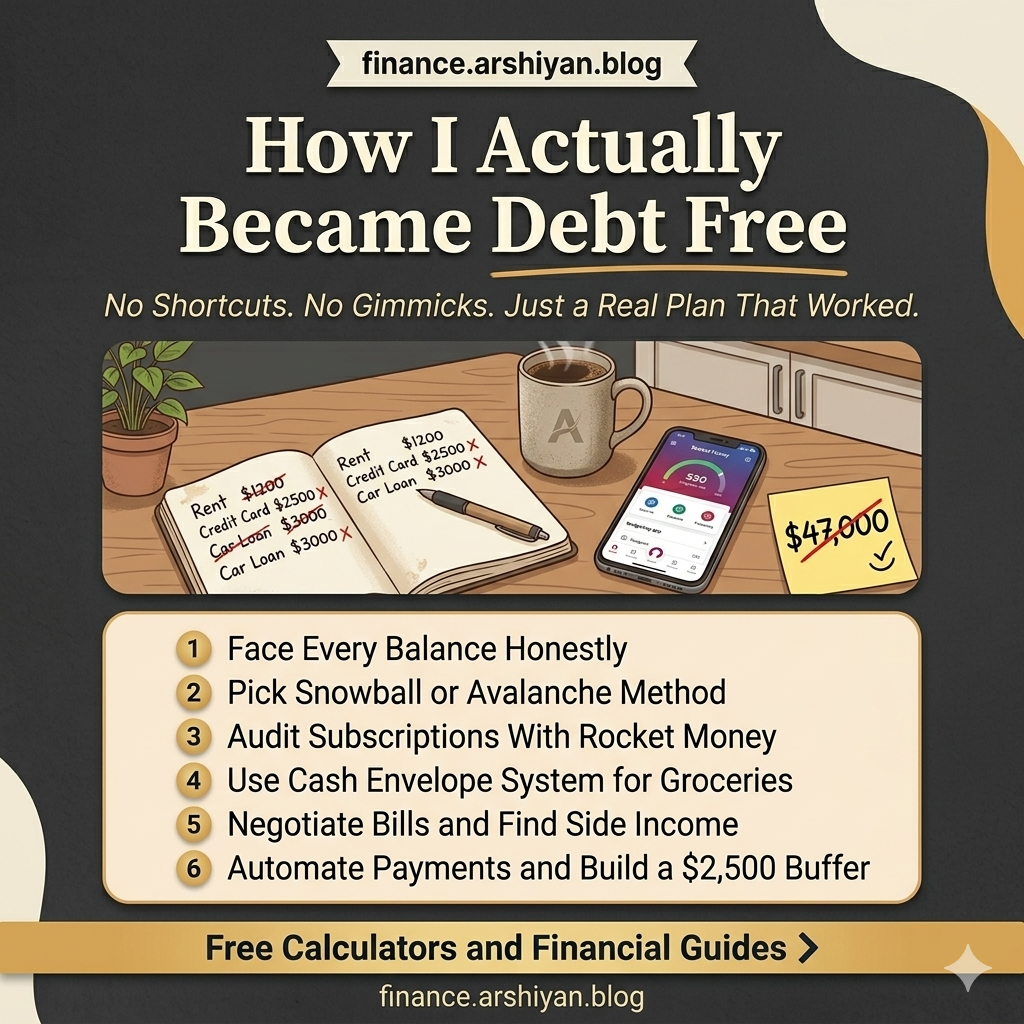

There was a Tuesday evening in 2019 when I sat at my kitchen table with a cup of cold coffee and a stack of bills that made my stomach churn. Credit cards, a car loan, medical bills from a surgery the year before, and a personal loan I took out to “consolidate” everything (spoiler: it didn’t help). The total came to $47,200. I remember the number because I wrote it on a sticky note and taped it to my bathroom mirror. That sticky note stayed there for three years, until the day I ripped it off and cried like a baby.

This article is everything I learned on that journey. Not theory. Not something I read in a textbook. This is what actually worked, what failed miserably, and what I wish someone had told me before I spent my twenties digging a financial hole with a credit card shaped shovel.

Why Most People Stay Stuck in Debt (And Think It Is Normal)

Here is the uncomfortable truth that nobody talks about at dinner parties. Debt has been completely normalized. Car payments, student loans, credit card balances carried month to month… we treat these things like they are just part of being an adult. Like gravity. Unavoidable.

But they are not.

The reason most people stay trapped is not because they are bad with money. It is because the entire system around them, from advertising to social pressure to the way banks market “minimum payments,” is designed to keep them borrowing. When every friend finances a new car and every coworker talks about their home renovation funded by a HELOC, choosing to live differently feels almost rebellious.

I am not going to sugarcoat this. Choosing a debt free life means swimming against a very strong current. But once you feel what it is like to have your paycheck actually belong to you, going back feels impossible.

Related Post: How to Build an Emergency Fund from Scratch

The Real Cost of Carrying Debt (Beyond the Interest Rate)

Everyone focuses on interest rates, and yes, paying 22% on a credit card is financial self harm. But the real cost of debt goes way deeper than percentages.

Mental bandwidth. When you owe money, a tiny part of your brain is always occupied by it. You are doing mental math at the grocery store. You are anxious when your phone rings from an unknown number. You are avoiding opening your mail. That low level stress eats away at your productivity, your relationships, and your health.

Opportunity cost. Every dollar that goes toward a minimum payment is a dollar that could be invested, saved, or spent on something that actually matters to you. I calculated once that the interest I paid on my credit cards over five years could have funded a two week trip to Portugal. That stung.

Decision paralysis. Debt makes you afraid to make moves. You stay in a job you hate because you cannot afford the risk of switching. You skip the dentist because you are already stretched thin. You say no to experiences because “next month will be better.” Except next month never is.

Step by Step: How I Actually Became Debt Free

I tried a lot of methods before finding what clicked. Let me walk you through the process that actually moved the needle.

Step 1: Face the Monster

I know it sounds dramatic, but this was genuinely the hardest part. I logged into every single account, every credit card, every loan portal, and wrote down four things for each debt: the total balance, the interest rate, the minimum monthly payment, and the due date.

I used a simple Google Sheet for this. Nothing fancy. Four columns. If spreadsheets make your eyes glaze over, even a notebook works. The tool does not matter. The honesty does.

Pro tip: Do not round the numbers down to make yourself feel better. I tried that. It only delays reality.

Step 2: Pick a Payoff Strategy (And Actually Stick With One)

There are two popular approaches, and both work. The key is picking one and committing to it like it is your new religion.

The Snowball Method means paying off the smallest balance first, regardless of interest rate. You make minimum payments on everything else and throw every extra penny at the smallest debt. Once that is gone, you roll that payment into the next smallest. The wins come fast, and that momentum is addictive.

The Avalanche Method means targeting the highest interest rate first. Mathematically, this saves you the most money over time. But psychologically, it can feel slow if your highest rate debt is also your largest balance.

I started with the avalanche method because I am a numbers person. After two months of feeling like I was getting nowhere, I switched to snowball. Paying off that first $800 medical bill gave me a rush I was not expecting. Sometimes the “less optimal” strategy is actually the best one because you will stick with it.

Related Post: Snowball vs Avalanche: Which Debt Payoff Method Actually Works

Step 3: Create Breathing Room in Your Budget

You cannot throw extra money at debt if there is no extra money. This is where most advice gets vague and unhelpful. “Just spend less!” Great, thanks, very illuminating.

Here is what I actually did:

Audited my subscriptions. I used an app called Rocket Money (it was called Truebill back then) to find recurring charges. I discovered I was paying for two music streaming services, a meditation app I used twice, and a cloud storage plan I completely forgot about. That freed up about $45 a month. Not life changing, but $45 a month is $540 a year.

Switched to a cash envelope system for groceries and dining. I withdrew a set amount each week and when it was gone, it was gone. This one change cut my food spending by nearly 30%. There is something about physically handing over cash that makes you think twice about that fancy cheese.

Negotiated bills. I called my internet provider and my car insurance company. With the internet provider, I simply said I was considering switching, and they knocked $15 off my monthly bill. The car insurance company matched a lower quote I found on Policygenius. Two phone calls, about 40 minutes total, saved me over $600 a year.

Related Post: 50 Practical Ways to Cut Monthly Expenses Without Feeling Deprived

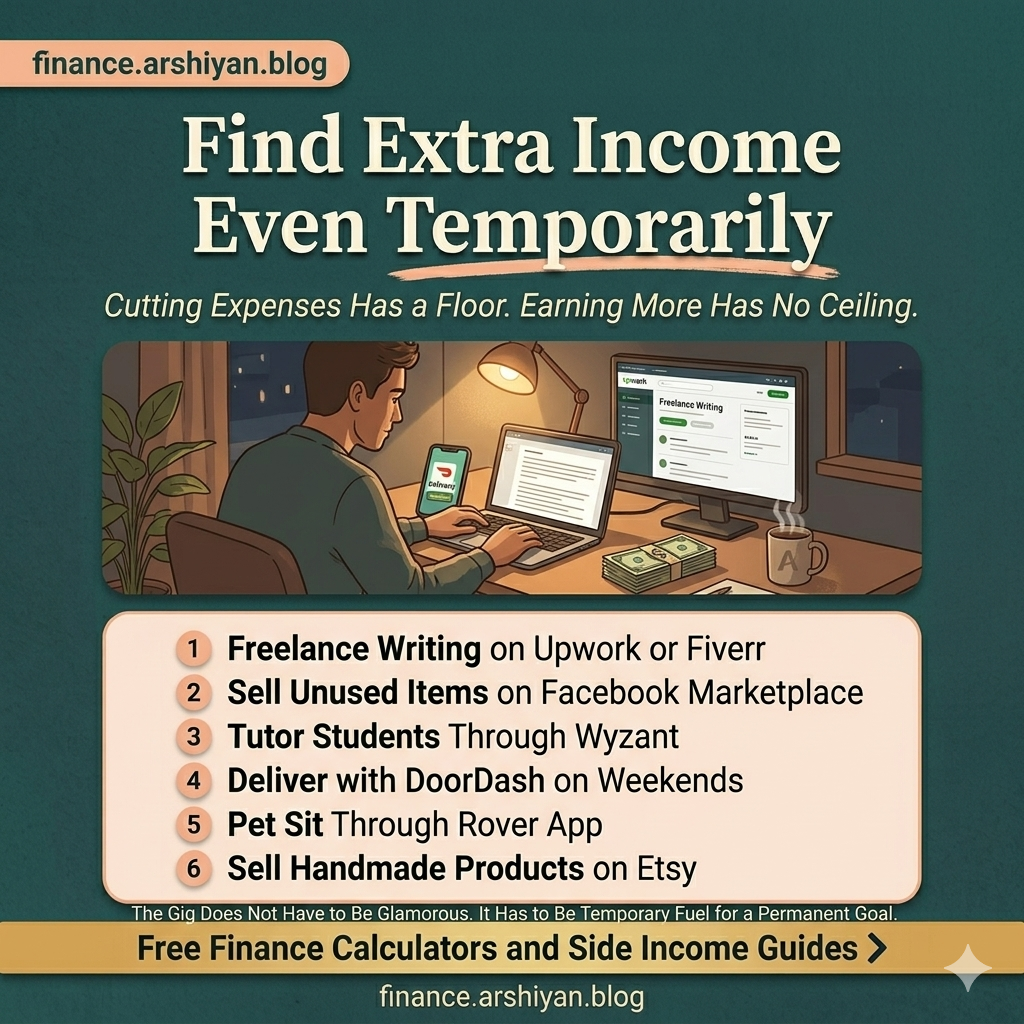

Step 4: Find Extra Income (Even Temporarily)

Cutting expenses has a floor. You can only reduce so much before life becomes miserable. But earning more has no ceiling.

During my debt payoff journey, I picked up freelance writing on the side. I also sold a bunch of stuff on Facebook Marketplace, things that had been collecting dust in my garage for years. Old furniture, a treadmill I used as a coat rack, power tools I inherited but never touched. That decluttering alone brought in about $2,100 over two months.

Other ideas that friends of mine used successfully: tutoring on Wyzant, driving for DoorDash on weekends, pet sitting through Rover, and selling handmade items on Etsy. The gig does not have to be glamorous. It has to be temporary fuel for a permanent goal.

Step 5: Automate Everything You Can

Willpower is a limited resource. I set up automatic payments for every minimum payment so I would never miss a due date. Then I set up a separate automatic transfer to my “debt attack” fund, a savings account I used purely as a staging area before making extra payments.

Every payday, money moved before I could touch it. Out of sight, out of mind. This removed the temptation to “borrow” from my debt payoff money for things that felt urgent but were not.

Step 6: Build a Tiny Emergency Buffer (Yes, Even While Paying Off Debt)

This is where I disagree with some financial gurus. The popular advice is to save only $1,000 as a starter emergency fund and then go all in on debt. I tried that. Then my car needed new brakes, and guess what? Right back on the credit card.

I kept $2,500 in a high yield savings account (I used Marcus by Goldman Sachs at the time) as a buffer. It slowed my debt payoff by maybe two months, but it prevented me from creating new debt every time life threw a curveball. And life throws a lot of curveballs.

Mistakes I Made That You Should Avoid

Let me save you some pain by sharing where I tripped up.

Trying to do too much at once. I went through a phase where I was working my day job, freelancing at night, meal prepping every Sunday, tracking every single penny, and reading personal finance books before bed. I burned out in six weeks. Sustainable progress beats frantic sprinting every time.

Not telling anyone. I kept my debt payoff journey a secret for almost a year because I was embarrassed. When I finally opened up to a close friend, she told me she was doing the same thing. We started checking in with each other monthly, sharing wins and setbacks. That accountability made a massive difference.

Depriving myself completely. I went through a three month stretch where I said no to literally everything. No coffee out, no social plans, no small treats. I ended up binge spending on a random weekend out of sheer frustration. The lesson? Budget a small amount for “fun money” so the pressure valve has a release. Even $30 a month for something you enjoy can prevent an expensive emotional blowout.

Ignoring the emotional side. Debt is not just a math problem. It is tangled up with shame, identity, childhood money stories, and self worth. I started journaling about my relationship with money, and that simple practice helped me understand why I overspent in the first place. If journaling feels weird, even talking to a financially savvy friend or a financial therapist can be transformative.

What Life Actually Looks Like on the Other Side

I paid off my last debt, a credit card with a $3,400 balance, in November 2022. The feeling was not what I expected. I thought there would be fireworks and confetti. Instead, there was this quiet, deep sense of calm. Like putting down a heavy backpack after a long hike.

Here is what changed:

My stress levels dropped dramatically. I did not realize how much mental energy debt was consuming until it was gone. I started sleeping better almost immediately.

I started saying yes to things that mattered. A weekend trip with friends. A nicer gift for my mom’s birthday. Signing up for a pottery class just because it sounded fun. These are small things, but when you have been saying no for years, they feel enormous.

My savings grew shockingly fast. All that money I was throwing at debt? It did not disappear. It just changed direction. Within eight months of being debt free, I had a fully funded emergency fund and had started investing through a Roth IRA on Fidelity.

I became less impulsive. Going through the discipline of paying off debt rewired how I think about purchases. I ask myself “do I need this or do I want to feel something right now?” more often than I would like to admit. But it works.

Related Post: How to Start Investing After Paying Off Debt

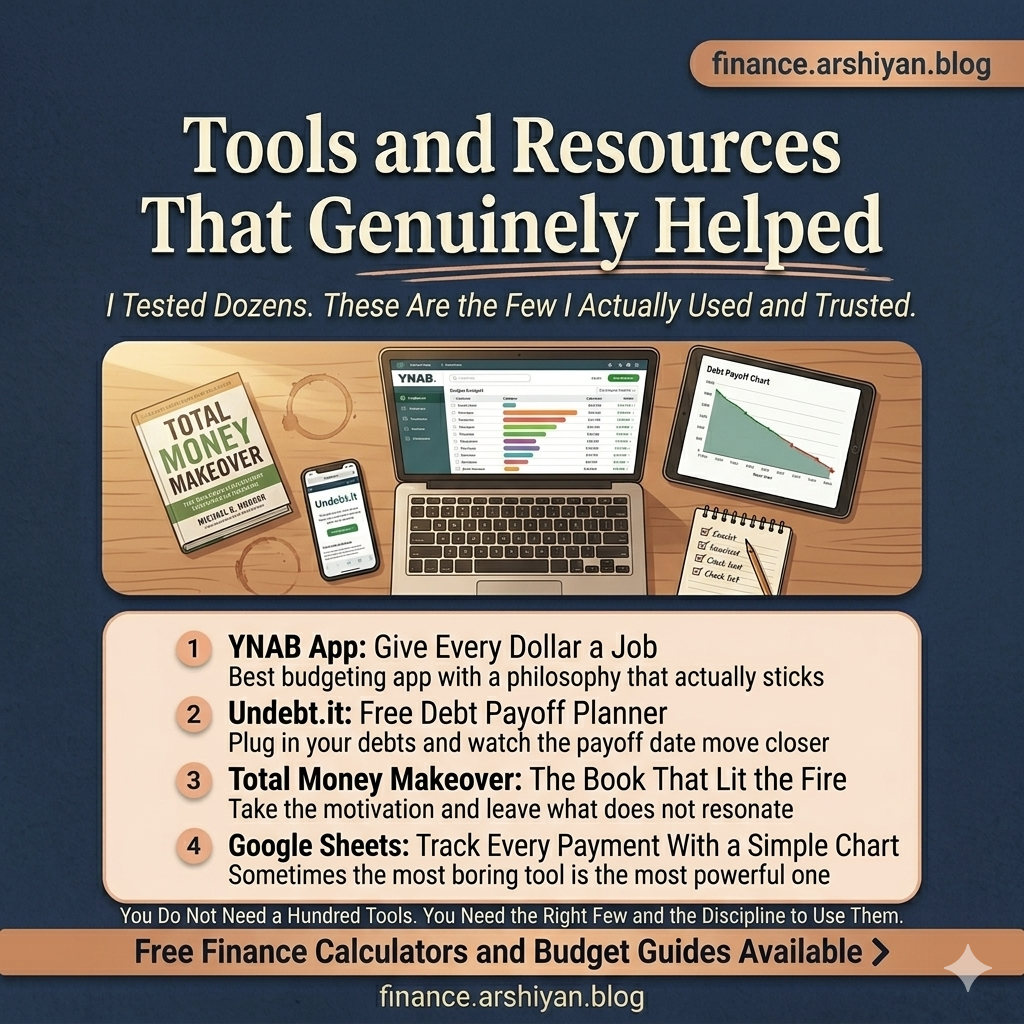

Tools and Resources That Genuinely Helped

I am not someone who recommends a hundred different tools. Here are the few that I actually used and found valuable.

YNAB (You Need a Budget): This budgeting app changed the way I think about money. It is not free, and the learning curve takes a couple of weeks, but it is worth every penny. The philosophy of giving every dollar a job clicked for me in a way that no other budgeting method did.

Undebt.it: A free online tool where you plug in all your debts and it creates a payoff plan using whatever strategy you choose. Watching the projected payoff date move closer as you make extra payments is incredibly motivating.

The “Total Money Makeover” by Dave Ramsey: I know Dave Ramsey is polarizing, and I do not agree with everything he says. But this book lit a fire under me when I needed it most. Take the motivation, leave the parts that do not resonate.

A simple spreadsheet: Sometimes the best tool is the most boring one. I tracked every payment in Google Sheets with a simple chart showing my total debt going down over time. On tough months, looking at that downward trend reminded me how far I had come.

The Mindset Shift That Makes It Last

Paying off debt is one thing. Staying debt free is another game entirely. The difference comes down to identity.

When you start seeing yourself as someone who does not do debt rather than someone who is temporarily restricting spending, the whole game changes. It is like the difference between a dieter and someone who genuinely enjoys eating healthy. One is fighting themselves. The other has simply changed what feels normal.

I still use a credit card for certain purchases. But I pay it off in full every single month, no exceptions. The moment a balance starts to carry over is the moment the old habits creep back. I treat that line like an electric fence.

Related Post: How to Use Credit Cards Without Going Into Debt

This Is Not About Perfection

I want to be honest about something. My journey was not a straight line. There were months where unexpected expenses ate into my progress. There were moments of doubt where I wondered if the sacrifice was worth it. There were arguments with my partner about spending priorities.

But every single difficult moment was worth it for the freedom on the other side. Not financial freedom in the “retire on a beach at 35” sense. Freedom in the everyday sense. Freedom to breathe. Freedom to choose. Freedom to live without that constant weight pressing on your chest.

If you are sitting where I was in 2019, staring at a number that feels impossible, I want you to know something. You are not bad with money. You are not broken. You just need a plan, some patience, and the willingness to do things differently than everyone around you.

That sticky note on my bathroom mirror? I kept it. It lives in a drawer now, folded up, a little faded. Every once in a while I take it out and look at it. Not to celebrate. Just to remember that the version of me who wrote that number down had no idea what she was capable of.

You probably do not know yet either. But you will.

Related Post: Complete Guide to Building Wealth After Getting Out of Debt