How to Create a Monthly Budget That Actually Works

How to Create a Monthly Budget That Actually Works

By Arshiyan ahmed | Personal Finance Writer

Most budgets die before the second week of the month. I know this firsthand because mine did — three times — before I finally figured out what I was doing wrong. It was not a math problem. It was not a willpower problem. I was just building something I could not actually live inside.

After spending several years working as a financial counselor in Chicago and helping hundreds of families get a handle on their spending, I want to share what works in real life — not what looks clean on a spreadsheet.

A note you can trust: The advice in this article comes from real client situations, personal experience, and well-established personal finance principles. No sponsored content. No affiliate magic tricks. Just what genuinely works for regular Americans trying to make their money behave.

What You Will Learn Here

- Why most budgets fail and how to avoid those traps

- A step-by-step process to build a budget you will actually stick to

- Real numbers from real people

- The best free tools to make it easier

- Common mistakes that quietly wreck your finances

- Answers to the questions people are too embarrassed to ask

Why Budgets Fail Before They Even Start

Before we talk about how to build one, let us be honest about the usual problems.

Most people sit down, write out all their income, subtract all their bills, and think the number left over is what they have to work with. But they forget about the irregular stuff: the car registration in March, the dentist visit in October, the holiday gifts in December. These are not surprises. They are scheduled. We just pretend they are not.

The other big trap is perfection paralysis. Someone makes a budget, overspends on groceries by forty dollars in week one, and throws the whole thing out. That is like getting a flat tire and then slashing the other three.

A working budget is not a perfect budget. It is a living document that gets adjusted as you go.

Step 1: Know Your Actual Income

This sounds obvious, but most people do not know their real take-home number. Write down what actually hits your bank account each month after taxes, health insurance, and retirement contributions come out.

If you have irregular income — maybe you drive for Lyft on weekends, do freelance work, or earn tips — take the average of the last three months. Do not use your best month. Do not use your worst. Use the middle.

Example: Sarah, a server in Nashville, made between $2,400 and $3,800 a month depending on the season. For years she budgeted based on her good months and scrambled every slow January. Once she started budgeting from her average of $2,900, everything changed. She built a cushion instead of burning through one.

Step 2: List Every Single Expense — Including the Sneaky Ones

Pull up your last two or three bank statements and credit card bills. Go line by line. You will probably find some surprises: that streaming service you forgot about, the gym membership you keep meaning to cancel, the subscription box that felt like a deal in September.

Group your expenses into categories:

Fixed expenses — same amount every month: rent or mortgage, car payment, minimum loan payments, insurance premiums.

Variable necessities — changes month to month but cannot be avoided: groceries, gas, utilities, healthcare costs.

Discretionary spending — the stuff that makes life enjoyable: dining out, clothing, entertainment, hobbies.

Irregular expenses — things that come up a few times a year: car maintenance, holiday gifts, annual subscriptions, vet bills.

That last category is where most budgets get ambushed. If your car registration is $200 a year, that is not a $200 expense in one month. It is a $17 expense every month that you should be setting aside.

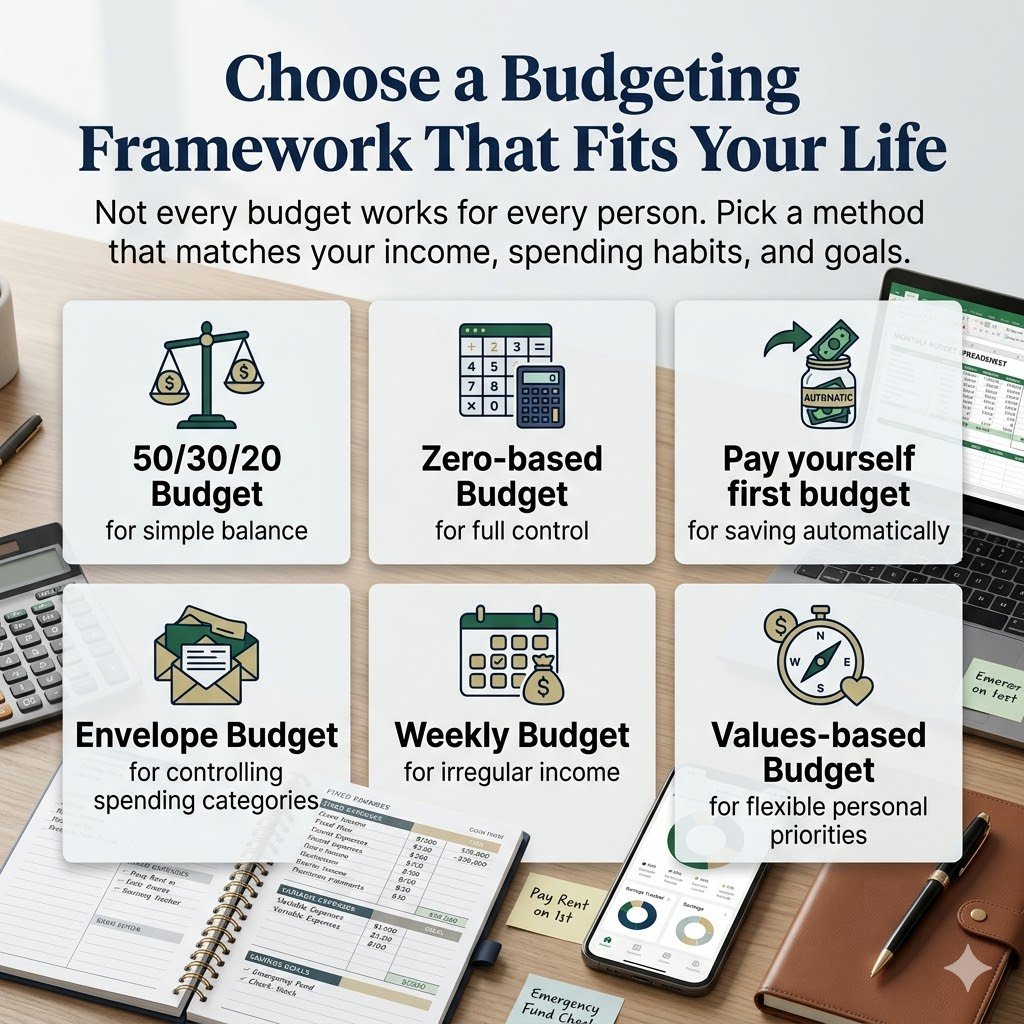

Step 3: Choose a Budgeting Framework That Fits Your Life

There is no single right method. Here are three that actually get used:

The 50/30/20 Rule

Fifty percent of your take-home goes to needs, thirty percent to wants, and twenty percent to savings and debt repayment. It is simple, flexible, and forgiving enough that most people can stick to it.

This works especially well for people new to budgeting who find detailed tracking overwhelming. It gives structure without a spreadsheet full of categories.

Zero-Based Budgeting

Every dollar gets a job. You take your monthly income and assign it all — living expenses, savings, fun money, everything — until you hit zero. Not zero in your account. Zero unassigned dollars.

This method requires more attention, but it makes you genuinely intentional about every dollar. The app YNAB (You Need a Budget) is built specifically around this approach and is worth the $15 a month subscription for people serious about turning their finances around.

The Cash Envelope System

Old school but surprisingly powerful for people who overspend because swiping a card does not feel real. You withdraw cash for your variable spending categories — groceries, restaurants, entertainment — and put the physical bills in labeled envelopes. When the envelope is empty, you are done spending in that category for the month.

I have seen this work wonders for people who tried every app imaginable but still overspent. There is something about handing over a twenty dollar bill that makes the transaction feel real in a way that tapping a phone never does.

Step 4: Build Your Budget Numbers

Now that you know your income and your expenses, you can write the actual budget.

Start with your fixed expenses. These are non-negotiable, so plug them in first.

Next, set your savings target. Yes, before your discretionary spending. This is the principle of paying yourself first, and it genuinely changes the math. If you wait to see what is left after spending to save, nothing will be left.

Then assign your variable and discretionary categories. Be realistic. Do not write $150 for groceries if you have three kids and a habit of buying organic. Write what you actually spend, then look for places to trim — but do not torture yourself.

A sample monthly budget for a single person earning $3,500 take-home in a mid-size American city might look like this:

| Category | Monthly Amount |

|---|---|

| Rent | $1,050 |

| Car payment | $280 |

| Utilities and internet | $130 |

| Groceries | $320 |

| Gas | $90 |

| Health insurance (out of pocket) | $80 |

| Phone | $65 |

| Streaming services | $35 |

| Dining out and entertainment | $200 |

| Clothing | $50 |

| Emergency fund contribution | $175 |

| Sinking fund (irregular expenses) | $75 |

| Retirement contribution | $150 |

| Total | $2,700 |

| Remaining buffer | $800 |

That $800 buffer is not free money to blow. It is breathing room. Some months utilities spike. Some months you need new tires. Having that cushion means you adjust the budget rather than blowing it up.

Step 5: Track and Review — Weekly, Not Monthly

The biggest mistake I see is people building a budget, filing it away, and checking in at the end of the month when the damage is already done.

Spending ten minutes every Sunday evening with your bank app open is genuinely transformative. Look at what you spent. Adjust your expectations for the rest of the month. Move money between categories if you need to. This is not failure — this is budgeting actually working.

Tools that make this easier:

Mint — free, connects to your bank, automatically categorizes spending. Best for beginners who want a hands-off overview.

YNAB — paid, built on zero-based budgeting principles, has the best community support and educational resources of any budgeting tool. Worth it if you are serious about changing habits.

Every Dollar — from Dave Ramsey’s team, has a free version and a paid version. Clean interface, easy to use.

A simple Google Sheets template — for people who want full control and zero subscription fees. Just search “Google Sheets budget template” and pick one that matches your categories.

A Real Case Study: The Martinez Family, Phoenix, Arizona

Marco and Diana Martinez came to me in 2021 with a household income of around $87,000 a year and nothing to show for it. They were not reckless spenders. They were just unaware. No one was watching the water leak out of the bucket.

We pulled six months of bank statements. They were spending $940 a month on restaurants and takeout — not because they loved eating out, but because both worked long hours and grocery shopping felt overwhelming. Their grocery budget was only $400 a month, which was not enough for a family of four, so they kept filling gaps with Doordash.

The fix was not dramatic. We raised their grocery budget to $700, lowered their restaurant budget to $350, and they started doing a Sunday afternoon prep session to make weeknight cooking easier. They saved $290 a month just from that one adjustment — more than $3,400 a year.

By the end of 2022, they had paid off a $6,200 credit card balance and had three months of expenses sitting in a high-yield savings account. Same income. Different awareness.

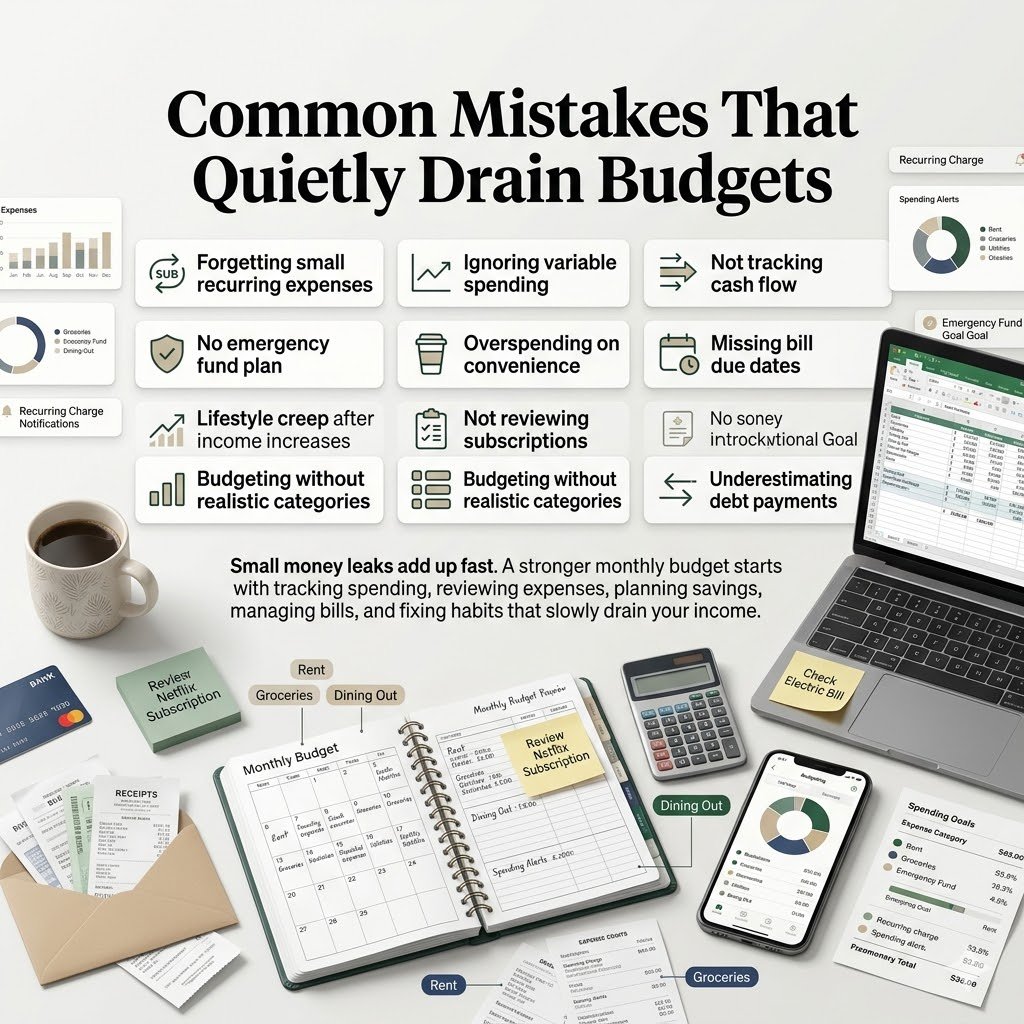

Common Mistakes That Quietly Drain Budgets

Forgetting annual expenses. Divide them by 12 and set that amount aside monthly. Car registration, Amazon Prime, holiday gifts, back-to-school shopping — all of these are predictable. Treat them that way.

Underestimating groceries. The USDA’s official “low-cost food plan” for a family of four in 2024 was around $1,050 a month. If you are writing $400, you are setting yourself up to fail before you start.

Not budgeting for fun. A budget with no breathing room is a punishment, not a plan. Give yourself guilt-free spending money, even if it is modest. Fifty dollars a month you can spend on whatever you want without tracking is worth more to your budget’s survival than that fifty dollars saved.

Treating debt minimum payments as the whole plan. Minimum payments are designed to keep you in debt as long as possible. If you can throw even an extra $50 a month at a credit card balance, it makes a real difference over time.

Expecting the first budget to be perfect. It will not be. The first few months are data collection. You are learning how you actually live, not how you think you live.

Tools Worth Knowing About

Rocket Money — great for identifying and canceling subscriptions you forgot about. Has helped many people find $50 to $150 a month in forgotten charges.

Chime or Ally Bank — both offer high-yield savings accounts where you can set up separate savings buckets for different goals, which makes the sinking fund concept much easier to manage.

Credit Karma — free credit score monitoring and a useful overview of your debts in one place.

Personal Capital (now Empower) — better for people who want to track net worth and investment accounts alongside their spending.

Frequently Asked Questions

How much should I have in an emergency fund? Three to six months of living expenses is the standard guidance. If your job is stable and you have a dual income household, three months is fine to start. If you are self-employed or work in a volatile industry, aim for six.

What if my income changes month to month? Budget from your lowest expected monthly income. Put anything extra directly into savings or toward debt. This feels restrictive on good months but gives you real stability on bad ones.

Should I budget if I am already in debt? Especially then. A budget is how you find the money to get out.

Is a joint budget different when you are married or partnered? It requires more communication, but the mechanics are the same. The most effective approach is a joint account for shared expenses with each partner retaining a small personal allowance — no questions asked — for individual spending.

How long until budgeting starts feeling natural? Give it three months of genuine effort. The first month is a mess. The second month starts to click. By the third, you stop dreading it.

Sources Used in This Article

- USDA Food Plans: Cost of Food, 2024 — usda.gov

- Consumer Financial Protection Bureau: Budgeting and Saving — consumerfinance.gov

- Bureau of Labor Statistics: Consumer Expenditure Survey, 2023 — bls.gov

- YNAB Educational Resources — youneedabudget.com

- National Foundation for Credit Counseling — nfcc.org

Helpful Next Steps

If this is all new to you, do not try to do everything at once. Start here:

This week, pull up your last month of bank statements and simply add up what you spent in each category. No changes yet. Just look at the numbers without judgment.

Next week, write a simple budget using the 50/30/20 method. One page. Real numbers.

The week after, set up a free account on Mint or Every Dollar and connect your bank account.

By the end of the month, you will have more financial clarity than most Americans ever get — and you will have built the foundation for everything else: savings goals, debt payoff, home ownership, retirement. None of it is possible without knowing where your money is going.

Budgeting is not about being a miser. It is about being the one in charge. Your money goes where you tell it to go — or it goes somewhere else entirely without your permission. The choice, genuinely, is yours.