Budgeting for Irregular Income: A Freelancer’s Survival Guide

Budgeting for Irregular Income: A Freelancer’s Survival Guide

Some months, freelancing feels like a well watered garden. Clients reply fast, invoices get paid on time, and your bank app looks almost cheerful.

Other months, it feels like you planted tomatoes in sand.

I know that rhythm too well. I have had months where I felt clever, capable, and almost annoyingly organized. I have also had months where three clients paid late at once, a yearly software renewal hit my card, and I stared at my account like it had personally betrayed me.

That is the strange little circus of irregular income. The work can be real, the pipeline can be healthy, and still the timing can turn your budget into jelly.

The good news is this: budgeting on freelance income is absolutely possible. You just cannot use the same playbook people use for a fixed paycheck. If you try to budget like a salaried employee, freelancing will keep pulling the rug out from under your feet.

What saved me was not working harder. It was building a system that expected uneven income instead of panicking every time it showed up.

First, stop expecting your money to act like a salary

This was my biggest early mistake.

I used to build a budget based on my best month, not my normal month. If I made a strong amount in one month, my brain instantly upgraded my lifestyle. I would think, great, this is the new standard now. Then the next month would be quieter, and suddenly I was doing mental gymnastics over groceries, subscriptions, and tax money I should have set aside already.

Freelance income is not broken because it changes. It is just irregular. The Consumer Financial Protection Bureau defines irregular income as money that comes in inconsistent amounts and on an inconsistent schedule. It also notes that a cash flow budget matters even more when income is seasonal, one time, or uneven because it helps spread money across the weeks or months when cash is thin.

That idea changed everything for me.

I stopped asking, “How much did I make this month?”

I started asking, “How long does this money need to last?”

That one question can save you from a lot of dumb decisions.

The budget that finally worked for me

I do not budget from expected income anymore. I budget from money already in hand.

That means if I have received money this month, I assign each part of it a job. Rent. Food. Utilities. Internet. Transport. Software. Taxes. Savings. Then I leave the rest alone.

This feels boring at first, which is usually a sign that it is working.

Upwork recommends calculating an average monthly income using the last six to twelve months as a baseline for budgeting because freelancing rarely comes with a fixed paycheck. That is a smart starting point.

Here is the simple version of how I do it.

Step 1: Find your survival number

This is not your dream lifestyle number. It is not your “I had a great month so let me celebrate with new gadgets” number.

It is the number that keeps your lights on and your stress below boiling point.

Sit down and write out your essential monthly costs:

Rent or mortgage

Utilities

Groceries

Phone

Internet

Transport

Insurance

Minimum debt payments

Software you genuinely need for work

Basic personal expenses

Now total them.

Let us say your essentials come to 1,200 dollars a month.

That 1,200 is your survival number. It is the amount your budget has to protect first, before anything fun, fancy, or flattering gets a vote.

When I first did this, I realized I had mixed up business comfort with business necessity. I had tools I barely used, subscriptions I forgot about, and “small” convenience spending that behaved like termites. One by one is nothing. Together, they eat the porch.

Step 2: Separate your money into buckets

This is the part that made my budget stop feeling like guesswork.

I keep my money in simple buckets. Not literal cash envelopes, though you can do that if it helps. I use separate savings spaces inside my bank account.

My core buckets are:

Bills

Taxes

Emergency fund

Business expenses

Personal spending

Future slow month buffer

When money comes in, I split it right away. I do not wait until the end of the month because that is how money gets blurry.

A useful real world example comes from Rob Phelan, who described using multiple savings buckets so he and his wife could stop scrambling when irregular bills showed up. Their system gave separate homes to specific expenses instead of letting everything float in one account like soup. That same idea works beautifully for freelancers because irregular income and irregular expenses often arrive together like two uninvited cousins.

If your bank supports savings spaces, buckets, or goals, use them. Many do. A checking account plus a high yield savings account setup is often enough.

Step 3: Pay yourself a steady amount

This was the closest thing to magic for me, though it is really just discipline wearing a plain shirt.

Instead of spending directly from whatever came in this week, I started paying myself a fixed amount from my income pool each month.

For example, if my freelance income over several months supported it, I might pay myself 1,500 dollars each month into my personal account. In a stronger month, the extra stayed in the buffer. In a weaker month, the buffer filled the gap.

This changed my day to day money stress more than any budgeting app ever did.

Your freelance income can stay irregular. Your personal spending does not have to.

Think of it like building a small reservoir. Rain does not fall on your schedule. But if you store it properly, your plants still get watered.

Step 4: Build a slow month fund before you chase big goals

A lot of freelancers skip this because saving feels impossible when income is patchy. I get it. But an uneven income without a buffer is like driving with no spare tire and calling it confidence.

The CFPB says an emergency fund is cash set aside for financial emergencies such as repairs, medical bills, or loss of income. Bankrate notes that people with unstable or self employed income may need more than the usual savings cushion because cash flow is less predictable.

When I was new, I aimed for a huge savings target too early and failed. What worked better was this:

First goal was 500 dollars

Second goal was one month of essential expenses

Third goal was three months of essential expenses

After that, I kept building

That first 500 mattered more than I expected. It covered a small emergency without forcing me to reach for a credit card like it was a life raft.

Step 5: Budget for taxes every single time

Nothing ruins a good freelance month faster than forgetting who else wants a slice of it.

I learned this the hard way once. I saw a healthy payment land, relaxed for five minutes, then remembered a decent chunk of it was never really mine.

Now I move tax money the same day I get paid.

No debate. No optimism. No “I will sort it later.”

Just move it.

If your platform allows automatic rules, use them. If not, make it a ritual. Payment arrives, tax portion moves, then I breathe.

For tools, I have seen freelancers manage this well with simple combinations like a bank account, Google Sheets, Notion, Wave, QuickBooks, or YNAB. You do not need a spaceship. You need a repeatable habit.

A practical example from real freelance life

Let us say Sara is a freelance designer.

In January she earns 3,000 dollars

In February she earns 900 dollars

In March she earns 2,400 dollars

In April she earns 1,300 dollars

Before budgeting properly, Sara spends freely in January because it felt like a strong month. By late February, she is tense, behind on tax savings, and using March income to patch holes from February. That is how freelancers end up living in permanent catch up mode.

Now let us run the same income through a better system.

Sara calculates her essential monthly costs at 1,100 dollars.

She decides her steady personal pay will be 1,300 dollars a month once her buffer is built. For now, she stays cautious and sets 1,100 as her monthly pay.

In January, she does this with her 3,000 dollars:

1,100 to personal pay

600 to taxes

500 to emergency savings

300 to business expenses

500 stays in buffer

In February, when only 900 comes in, she does not panic. Her January buffer helps cover the gap. She still pays herself from the system, not from her mood.

This is the whole point. The budget absorbs the chaos so your nervous system does not have to.

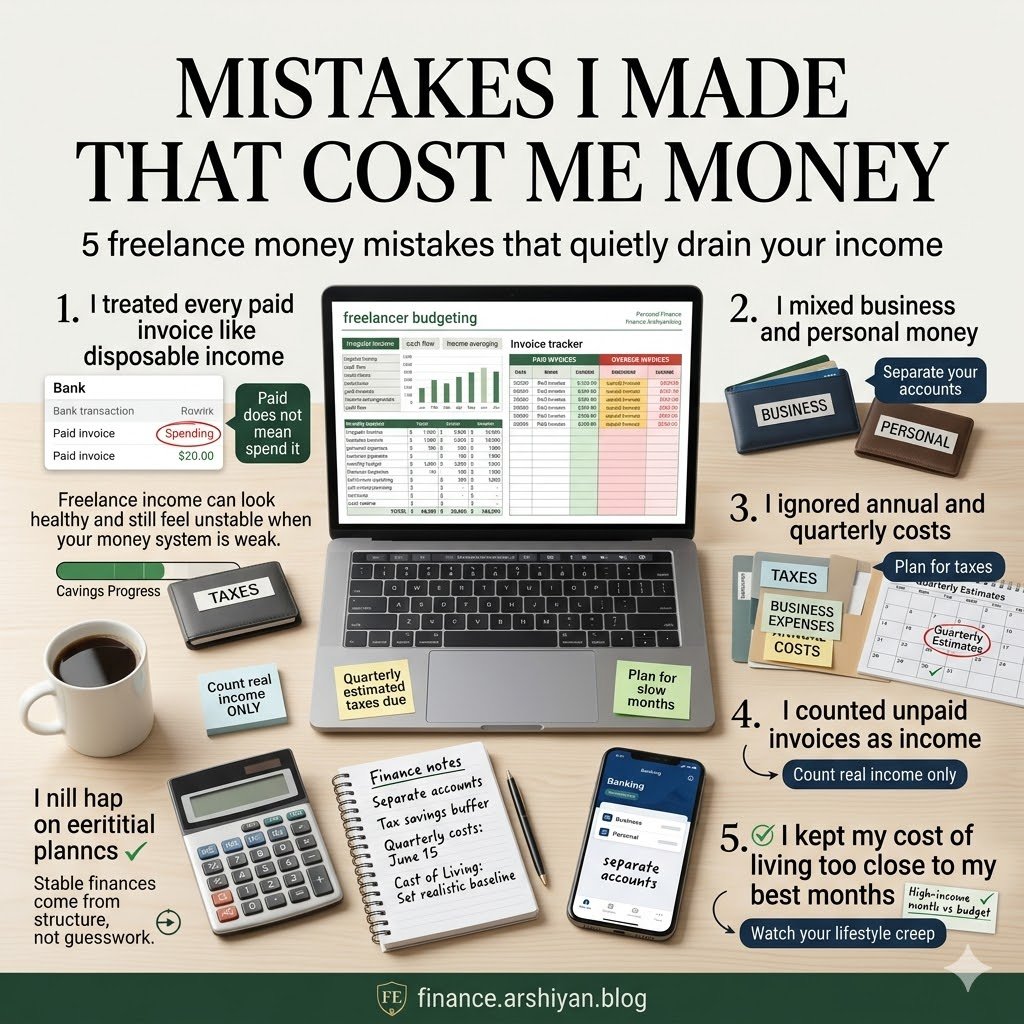

Mistakes I made that cost me money

I wish I could say I figured this out elegantly. I did not. I learned it the same way many freelancers do, by tripping over my own shoelaces.

I treated every paid invoice like disposable income

A paid invoice is not spending money. It is raw material. Some of it belongs to taxes. Some belongs to next month. Some belongs to software renewals you will pretend to forget until they hit.

I mixed business and personal money

This made everything muddy. My account looked fuller than it really was because client money, tax money, and grocery money were all swimming together like one confused fish tank.

I ignored annual and quarterly costs

Domain renewals, hosting, insurance, equipment replacements, membership fees, quarterly tax payments. These are not surprises. They are scheduled ambushes.

Now I divide annual costs by twelve and save a little each month.

I counted unpaid invoices as income

Never again.

Money is income when it lands, not when it is promised. Until then, it is just a polite hope wearing a blazer.

I kept my cost of living too close to my best months

This is a trap. One writer I came across described keeping living costs low on self employed income so income swings were easier to handle and savings could stay healthy. That is not glamorous advice, but it is sturdy advice.

Freelancers do better when their baseline life is lighter than their peak income suggests.

A trustable case study worth paying attention to

One of the most useful ideas I have seen in practice is bucket budgeting. In a Business Insider essay, Rob Phelan explained that he and his wife used multiple savings buckets after realizing they were always scrambling when irregular bills showed up. Their bucket system gave each expense a clear home and reduced that last minute panic.

Why does this matter for freelancers?

Because our problem is rarely just low income. It is uneven timing.

A bucket system solves a timing problem. It lets money wait in the right place until real life comes calling. That same structure can be used for tax money, slow season savings, equipment replacement, annual subscriptions, and time off.

I use a simpler version myself, and the results are easy to feel.

Less panic before bill dates

Fewer surprise shortfalls

More clarity when deciding whether I can actually afford something

Better sleep, which is not a spreadsheet metric but should be

The apps and tools that actually help

You do not need all of these. Pick one or two and keep moving.

YNAB is great if you want to assign every dollar a job and budget only what you already have.

Google Sheets is perfect if you like seeing your numbers clearly and want full control.

Notion is useful if you want a simple freelance dashboard with income tracking, invoice dates, and monthly planning.

Wave works well for invoicing and basic accounting.

QuickBooks can help if your bookkeeping is getting messier than your desk drawer.

A plain savings account with labeled spaces is still one of the best tools in the whole setup.

Fancy tools do not rescue messy habits. Plain tools used well often do.

FAQ

How much should a freelancer save before feeling safe?

Start with 500 dollars if that is realistic. Then aim for one month of essential expenses. After that, work toward three months and build from there. If your income swings wildly, a bigger buffer is often wiser.

Should I use an average income to budget?

Yes, but use a cautious average. Look at the last six to twelve months and avoid building your lifestyle around your top earning month.

What if I have one terrible month?

That is exactly why the buffer exists. Cut spending to essentials, pause non urgent purchases, chase receivables, and let the system carry part of the load.

Is zero based budgeting good for freelancers?

It can be, especially if you are budgeting money already received. The key is not forcing a fixed income model onto a variable income life. Bankrate notes that zero based budgeting can help, but it is also something many people need to learn gradually.

Should I pay myself weekly or monthly?

Either can work. Monthly feels simpler to me because most bills are monthly. Weekly can be useful if it helps you control spending better.

What changed after I finally got serious about this

The biggest result was not that I became rich overnight. I did not.

The biggest result was that I stopped feeling ambushed by my own career.

Late payments still happen. Quiet months still happen. A laptop battery can still die at the worst possible moment because apparently electronics enjoy drama. But now those events are problems to solve, not financial thunderstorms rolling through my chest.

Freelancing gets easier when your budget is built like a greenhouse, not a picnic table. A picnic table works only when the weather is kind. A greenhouse expects weather and keeps going anyway.

That is really the whole game.

You do not need a perfect income to feel stable. You need a system that respects the fact that freelance money arrives when it arrives, and still keeps your life standing upright when the wind changes.