Zero Based Budgeting for Beginners A Complete Walkthrough

Zero Based Budgeting for Beginners: A Complete Walkthrough

I still remember staring at my bank statement in 2019, genuinely confused about where $1,400 had disappeared that month. I earned decent money. I wasn’t buying designer clothes or eating lobster every night. Yet somehow, by the 25th of every month, I was scraping by. Sound familiar?

That was the month I stumbled onto zero based budgeting, and honestly, it changed my entire relationship with money. Not overnight, mind you. The first two months were messy. But once it clicked, it stuck. So let me walk you through exactly how this works, the way I wish someone had explained it to me four years ago.

What Zero Based Budgeting Actually Means

Forget the textbook definition for a second. Here’s the simplest way I can put it: every single dollar you earn gets a job before the month starts. Every. Single. One.

Most people budget loosely. They pay their rent, cover a few bills, and then wing it with whatever is left. That “winging it” part? That’s the budget killer. It’s like trying to drive cross country with no map and just hoping you end up somewhere nice.

With zero based budgeting, your income minus your expenses equals exactly zero. That doesn’t mean you spend every penny. It means every penny is accounted for. Savings gets assigned. Groceries get assigned. Even your fun money gets assigned. Nothing floats around unaccounted for, waiting to be wasted on impulse Amazon purchases at 11 PM.

Why This Method Works Better Than Most

I’ve tried the 50/30/20 rule. I’ve tried envelope stuffing. I even tried that thing where you just “pay yourself first” and hope for the best. They all worked for about six weeks before I fell off.

Zero based budgeting worked because it forced me to make decisions before the money hit my account. When you sit down and plan every dollar, you’re essentially having a conversation with yourself about what actually matters to you. And that conversation, uncomfortable as it sometimes is, builds a kind of muscle memory around spending.

There’s also a psychological trick at play here. When money has no label, spending it feels harmless. But when you know that $60 is earmarked for your electric bill, suddenly blowing it on takeout feels like stealing from yourself. That tiny mental shift is surprisingly powerful.

A Real World Example to Make This Click

Let’s say you bring home $3,200 a month after taxes. Here’s what a zero based budget might look like:

Housing and utilities: $1,100 (rent, electric, water, internet)

Transportation: $350 (car payment, gas, insurance)

Groceries: $400

Minimum debt payments: $200

Subscriptions: $45 (streaming, Spotify, cloud storage)

Phone bill: $65

Personal spending: $150 (coffee, hobbies, random wants)

Clothing: $50

Health: $90 (gym, medications, copays)

Extra debt payoff: $200

Emergency fund contribution: $300

Giving or charity: $50

Miscellaneous buffer: $100

Saving for holiday gifts: $100

Total: $3,200. Income minus outgo equals zero.

Now, your numbers will look completely different from mine. That’s the whole point. This isn’t a cookie cutter template. It’s a framework you build around your own life.

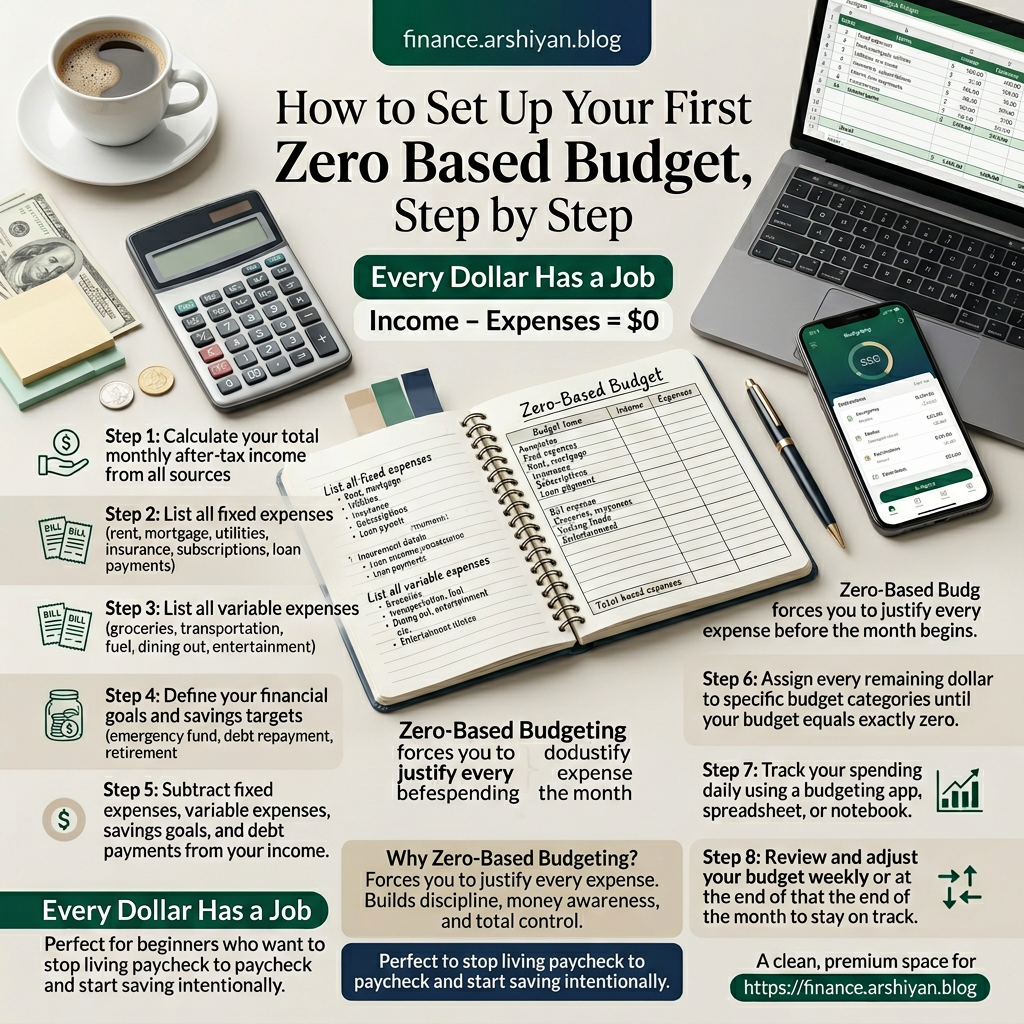

How to Set Up Your First Zero Based Budget, Step by Step

Step 1: Figure Out Your Actual Take Home Pay

Not your salary. Not your gross income. Your actual, after tax, deposited in your bank account number. If your income varies month to month (freelancers, gig workers, I see you), use the lowest amount you’ve earned in the past three months as your baseline. You can always adjust upward if a good month hits.

Step 2: List Every Single Expense You Can Think Of

I mean everything. Rent, groceries, car insurance, the $4.99 iCloud storage fee you forgot about, your kid’s soccer registration, the quarterly oil change coming up in six weeks. Pull up your bank and credit card statements from the last 90 days. You’ll be shocked at what you find hiding in there.

When I did this the first time, I discovered I was paying for two music streaming services. One was a free trial I forgot to cancel eight months earlier. That’s $9.99 a month I’d been lighting on fire.

Step 3: Assign Every Dollar a Category

Start with the essentials: housing, food, transportation, utilities, minimum debt payments. These are non negotiable. Then move to the important but flexible stuff: savings, extra debt payments, insurance. Finally, fill in the wants: dining out, entertainment, hobbies, personal spending.

If your expenses add up to more than your income, something has to go. This is the part that stings, but it’s also where the magic happens. You’re making conscious choices instead of letting money just evaporate.

If your expenses add up to less than your income, assign that leftover somewhere. Extra savings. An investment account. A vacation fund. Whatever you want, just give it a name.

Step 4: Track Everything Throughout the Month

This is where most beginners trip up. Writing the budget is the easy part. Living it is the challenge. You need a system for tracking what you spend in real time, not at the end of the month when it’s too late to course correct.

I personally use the EveryDollar app on my phone. It’s clean, simple, and built specifically for zero based budgeting. YNAB (You Need A Budget) is another fantastic option, though it has a learning curve and a subscription fee. For people who prefer spreadsheets, Google Sheets works perfectly well. There are dozens of free templates floating around that you can customize.

The key is checking in daily. It takes about two minutes. Just open the app or spreadsheet, log what you spent, and see where you stand. Think of it like stepping on a scale when you’re trying to eat healthier. The number keeps you honest.

Step 5: Adjust and Redo It Every Single Month

Here’s something nobody told me at the beginning: your budget will be different every month. February has Valentine’s Day. March might have a friend’s birthday. August has back to school expenses. December, well, December is its own beast.

Sit down a few days before each new month and build a fresh budget from scratch. Yes, from scratch. That’s the “zero based” part. You’re not just rolling last month forward. You’re deliberately choosing how to allocate money based on what’s actually coming up.

Mistakes I Made (So You Don’t Have To)

Being too aggressive with categories. My first budget had 27 separate categories. It was exhausting to track and I gave up by week two. Keep it between 10 and 15 categories to start. You can always get more detailed later.

Not budgeting for irregular expenses. Oil changes, annual subscriptions, holiday gifts, car registration. These sneak up on you like a cat stalking a laser pointer. The fix? Estimate the yearly cost, divide by 12, and set that amount aside every month in a sinking fund.

Treating the budget like a straitjacket. If you go $30 over on groceries, you don’t throw the whole thing out the window. You pull $30 from another category, maybe personal spending, and move on. Flexibility isn’t failure. Rigidity is what makes people quit.

Forgetting to budget for fun. This one nearly killed my motivation. If your budget is nothing but bills and debt payments with zero room for enjoyment, you’ll rebel against it within a month. Give yourself permission to spend on things that bring you joy. Just do it on purpose.

What Happened After Six Months

Six months into zero based budgeting, I had paid off a $2,300 credit card balance that had been haunting me for over a year. I had $1,800 in an emergency fund, which was $1,800 more than I’d ever saved before. And I was spending less overall while somehow feeling less deprived.

The real surprise was how much calmer I felt about money. Before, every unexpected expense sent me into a mild panic. A $400 car repair would ruin my whole week. But with a budget and a small cushion, those surprises became inconveniences instead of crises. That peace of mind is worth more than any specific dollar amount.

A Case Study Worth Knowing About

Unilever, the consumer goods giant behind brands like Dove and Ben and Jerry’s, adopted zero based budgeting across their operations around 2016. Their finance team restructured spending from the ground up, requiring every department to justify costs from zero rather than simply adding a percentage to last year’s budget.

The results were notable. Unilever reported saving around 2 billion euros in cumulative cost reductions over several years while simultaneously increasing investment in marketing and product development. They didn’t just slash expenses blindly. They reallocated resources toward areas that generated the most value.

Now, obviously you’re not running a multinational corporation. But the principle translates perfectly to personal finance. When you justify every dollar from zero instead of just rolling forward old spending habits, you naturally trim the waste and funnel money toward what actually matters.

Kraft Heinz followed a similar path after their merger in 2015, implementing zero based budgeting to streamline operations. They achieved significant cost savings in their first few years, though they also learned the hard way that cutting too deeply into certain areas, like marketing and innovation, can backfire. The lesson for personal budgets? Cut the fat, not the muscle. Eliminate waste, but don’t starve the categories that fuel your quality of life.

Tools and Apps That Make This Easier

EveryDollar is my go to recommendation for beginners. The free version handles basic zero based budgeting beautifully. The premium version connects to your bank for automatic transaction importing.

YNAB is more powerful and more philosophical in its approach. It teaches you to budget only money you already have, not money you expect to earn. The annual subscription runs around $99, but many users swear the return on investment is enormous.

Goodbudget uses a digital envelope system that pairs well with zero based principles. It’s great for couples managing money together because you can sync across devices.

Google Sheets or Excel work perfectly if you like building your own system. The advantage is total customization. The disadvantage is that nobody is going to send you a notification when you overspend on dining out.

Who This Method Works Best For

Zero based budgeting shines brightest for people who feel like their money disappears without explanation. If you earn a reasonable income but can never seem to save, this approach will almost certainly reveal where the leaks are.

It’s also excellent for people paying off debt aggressively. When every dollar has an assignment, you can deliberately funnel extra cash toward your highest interest balance instead of hoping there’s something left at the end of the month.

That said, it does require more time and attention than simpler budgeting methods. If the idea of planning your spending monthly feels overwhelming right now, starting with a basic spending tracker might be a gentler first step. You can graduate to zero based budgeting once you have a few months of data to work with.

The Part Nobody Talks About

Budgeting is emotional. The first time you lay out all your numbers, you might feel embarrassed, frustrated, or even a little hopeless. That’s normal. You’re looking at reality, possibly for the first time in a while, and reality can be a tough mirror.

But here’s what I’ve learned after doing this for years: the numbers themselves aren’t the enemy. They’re just information. And information is something you can work with. You can’t fix what you can’t see, and a zero based budget shows you everything.

My finances aren’t perfect today. I still overspend sometimes. I still have months where unexpected expenses blow a hole in my plan. But I’m never lost anymore. I always know where I stand, what I owe, and where my money is going. That awareness alone has been worth every minute I’ve spent building budgets at my kitchen table with a cup of coffee and a spreadsheet.

If you’ve been putting this off, just start. Pull up a blank page, write down your income, and start giving those dollars their marching orders. Your first budget won’t be pretty. Mine certainly wasn’t. But it will be the beginning of something that actually works.

FAQ

What is zero based budgeting in simple terms?

It means you plan how to spend every dollar of your income before the month begins. Your total income minus all planned expenses equals exactly zero. Nothing is left unassigned.

Does zero based budgeting mean I spend all my money?

Not at all. It means every dollar has a purpose. Savings, emergency funds, and investments all count as assignments. Money sitting in a savings account still has a job.

How long does it take to set up a zero based budget?

Your first one might take 30 to 45 minutes because you need to dig through bank statements and list every expense. After the first month, it usually takes about 15 to 20 minutes.

What if my income changes every month?

Use the lowest amount you earned over the past three months as your starting number. If extra money comes in during the month, assign it to a category right away instead of letting it float.

How often should I update my zero based budget?

Build a brand new budget before every month starts. During the month, check your spending daily or every couple of days so you can make small adjustments before things get off track.