Beginner’s Guide to Investing After Building Your Emergency Fund

Beginner’s Guide to Investing After Building Your Emergency Fund

By Arshiyan Ahmed | Personal Finance Writer

There is a moment that happens to a lot of people — maybe it happened to you — where you check your savings account and realize you actually did it. You built your emergency fund. Three months of expenses. Maybe six. The money is just sitting there, quiet and patient, not being touched.

And then the next question hits you like a slow wave: now what?

I remember that moment clearly. I had $11,000 sitting in a savings account earning 0.04% interest at a big national bank, feeling proud of myself while inflation quietly ate away at my purchasing power. A coworker mentioned index funds in passing one afternoon and I nodded like I knew what he was talking about. I did not.

That was the beginning of me actually learning how investing works — not from a textbook, but from making moves, watching what happened, and eventually helping other people do the same. What follows is what I wish someone had handed me on a single afternoon.

A note worth reading: Nothing in this article is personalized financial advice. I am not a licensed financial advisor. What I am sharing is based on personal experience, years of working with everyday Americans on their finances, and well-established investing principles. Always consider your own situation and consult a fee-only fiduciary advisor for major decisions.

What You Will Learn Here

- Why having an emergency fund first actually matters for investing

- The right order of financial moves before putting money in the market

- Where to start investing as a complete beginner

- Real examples of how regular people built wealth from small starts

- The most common beginner mistakes and how to sidestep them

- The best apps and platforms for new investors in the USA

- Honest answers to questions beginners are embarrassed to ask out loud

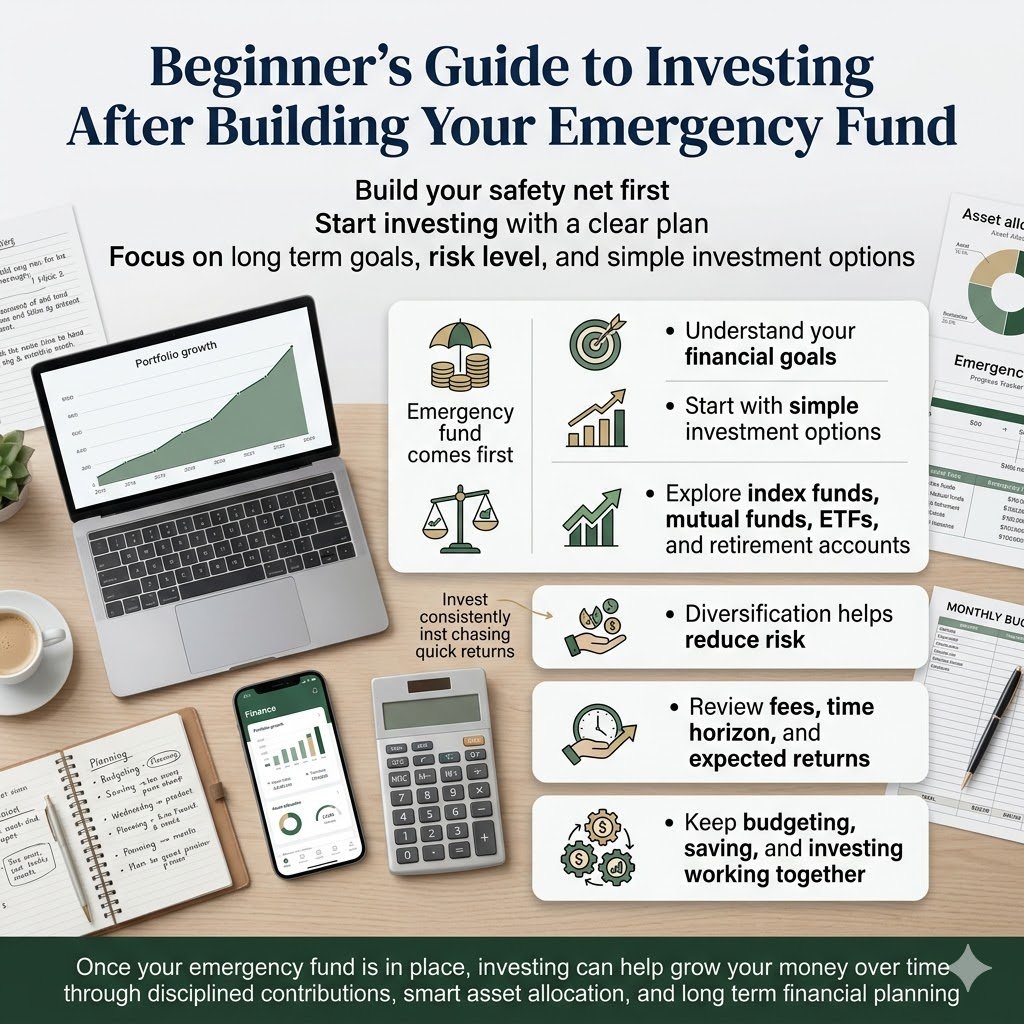

Why the Emergency Fund Changes Everything

Let me explain something that most investing articles skip right past.

The reason the emergency fund comes first is not just about safety. It is about psychology. When your car breaks down and you have no cushion, the tempting move is to sell your investments to cover it. That is exactly the wrong time to sell — usually when markets are unpredictable and you are making emotional decisions, not rational ones.

Your emergency fund is the firewall between your life and your portfolio. Without it, the first inconvenience destroys the whole strategy. With it, you can leave your investments alone long enough for them to actually grow.

Now that yours is in place, you have permission to think longer-term. That shift in mental posture is more valuable than any stock tip.

Step 1: Clean Up Before You Invest

Before a single dollar goes into a brokerage account, take a look at your existing financial picture.

Pay off high-interest debt first. Credit card debt at 22% annual interest is a guaranteed negative return. No index fund can reliably beat that. Paying off a $3,000 credit card balance before investing is itself a 22% return on that money — you just will not see it on a chart.

A good rule of thumb: if the interest rate on a debt is above 7%, pay it off before investing. Below 5%, investing alongside it often makes more sense mathematically. Between 5% and 7%, it is genuinely a judgment call.

Check your employer’s 401(k) match. If your employer matches contributions to your retirement account — say, 50 cents for every dollar you put in up to 6% of your salary — that match is a 50% instant return on that money. Capturing the full match before doing anything else is almost always the smartest first move.

Step 2: Understand the Accounts Available to You

This is where a lot of beginners get tangled up. There are several different account types and they behave very differently from a tax perspective.

401(k) or 403(b): Offered through your employer. Contributions come out of your paycheck before taxes, reducing your taxable income today. You pay taxes when you withdraw in retirement. If your employer offers a match, this is your first stop.

Traditional IRA: An Individual Retirement Account you open yourself. Similar tax structure to a 401(k). Contributions may be tax-deductible depending on your income and whether you have a workplace plan.

Roth IRA: Contributions go in after taxes — meaning you do not get a deduction now — but the money grows tax-free and withdrawals in retirement are completely tax-free. For most people in their 20s and 30s who expect to be in a higher tax bracket later, the Roth IRA is a gift. The 2024 contribution limit is $7,000 per year, or $8,000 if you are 50 or older.

Taxable brokerage account: No tax advantages, but no restrictions either. You can put in as much as you want and take money out whenever you want without penalties. This becomes relevant once you have maxed out your tax-advantaged options.

For most beginners, the order looks like this: Get the full 401(k) employer match first. Then max out a Roth IRA. Then go back and contribute more to the 401(k). Then open a taxable brokerage account if you have more to invest.

Step 3: Pick Your First Investment

Here is where people freeze up. Thousands of stocks. Hundreds of funds. Endless opinions online.

Let me make this simple.

For the vast majority of new investors, a low-cost index fund is the right starting point. An index fund does not try to pick winners. It buys a little piece of everything in a particular market index — like the S&P 500, which includes 500 of the largest American companies — and holds it.

The math behind this is genuinely compelling. According to S&P Dow Jones Indices, over any given 15-year period, roughly 88% of actively managed large-cap funds underperformed the S&P 500 index. Professional fund managers with research teams and enormous resources still could not beat the market consistently. Buying the whole market instead of trying to outsmart it is not a lazy strategy. It is a logical one.

Two funds that get recommended by serious investors over and over:

VTSAX — Vanguard Total Stock Market Index Fund. Covers the entire US stock market. Available at Vanguard directly or as an ETF version (VTI) at most brokerages.

FZROX — Fidelity Zero Total Market Index Fund. Similar coverage to VTSAX with a 0% expense ratio. Only available at Fidelity.

The expense ratio matters more than most beginners realize. A fund charging 1% annually versus 0.03% might sound like a rounding error, but over 30 years on a $50,000 investment that difference costs you tens of thousands of dollars in compounding returns.

Step 4: Set Up Automatic Contributions

The secret weapon of wealth building is not stock picking. It is consistency.

Set up an automatic transfer on payday — before you have a chance to spend that money — into your investment account. Even $50 a month matters. Time in the market is almost always more valuable than timing the market.

This approach has a fancy name: dollar-cost averaging. What it means in plain terms is that you buy more shares when prices are low and fewer when prices are high, automatically, without needing to think about it. Over time this smooths out the bumps and removes emotion from the equation entirely.

A Real Case Study: How Marcus Built $40,000 Starting From Zero

Marcus was 28, living in Atlanta, working as a project manager earning $62,000 a year. He had spent his mid-20s paying off $18,000 in student loans and a credit card balance. By 27, the debt was gone and he had built a $9,000 emergency fund sitting in a Marcus by Goldman Sachs high-yield savings account earning around 4.5%.

He came to me confused about where to start. We sat down for about two hours.

First, his employer offered a 4% 401(k) match and he was only contributing 2%. We bumped that up immediately, capturing the full match. That alone was essentially a $1,240 annual raise he had been leaving on the table.

Next, we opened a Roth IRA through Fidelity. He set up a $200 monthly automatic contribution into FZROX — their zero-fee total market fund. He barely noticed the money leaving.

He also started putting an extra $100 a month into a taxable brokerage account through Fidelity, buying shares of VTI, the Vanguard Total Stock Market ETF.

At 33, five years later, the combination of his 401(k) contributions and employer match, his Roth IRA, and his taxable account had grown to just over $40,000. He had never tried to pick a single stock. He had never panicked and sold during a down market, because his emergency fund meant he never needed to. He had just shown up every month and let the math do its work.

The Mistakes That Cost Beginners the Most

Waiting for the perfect moment. There is no perfect moment. People who waited for the market to “calm down” before investing in 2009, 2016, 2020, and 2022 missed enormous recoveries. The best time to start was yesterday. The second best time is today.

Picking individual stocks right away. Picking one company to bet on when you are still learning how markets work is like learning to swim in a riptide. Start with index funds. Give yourself two or three years before touching individual stocks, and even then keep it to a small percentage of your portfolio.

Checking your portfolio every day. This is not investing. This is anxiety with a brokerage account. Markets fluctuate constantly. Looking daily trains your brain to react emotionally to noise rather than staying committed to a long-term strategy.

Ignoring tax efficiency. Putting investments in the wrong accounts costs real money. High-growth assets belong in Roth accounts where gains are never taxed. Bond funds or dividend-heavy investments often make more sense in traditional retirement accounts.

Cashing out when you change jobs. When you leave an employer, you can roll your 401(k) into an IRA without taxes or penalties. Cashing it out instead means paying income tax plus a 10% early withdrawal penalty. This is one of the most expensive financial mistakes I see people make.

Tools and Platforms Worth Using

Fidelity — best overall for beginners. No account minimums, no fees to buy their index funds, excellent educational resources, and their app is clean and easy to navigate.

Vanguard — the gold standard for index fund investing. Interface is a bit older but the funds are legendary and the company is structured to keep costs low permanently.

Schwab — solid option with no minimums and good customer service. Their S&P 500 index fund (SCHB) has a very low expense ratio.

Robinhood — fine for a taxable brokerage account once you understand the basics, but the app design encourages frequent trading, which tends to hurt long-term returns. Use it carefully.

Empower (formerly Personal Capital) — free financial dashboard that pulls together your 401(k), IRA, and bank accounts in one place so you can see your net worth growing over time. Genuinely motivating to watch.

Investopedia — not a brokerage but an educational resource. When a term confuses you, this is where to look it up. The explanations are clear and advertisement-free.

Frequently Asked Questions

How much do I need to start investing? Fidelity and Schwab both allow you to open accounts with no minimum. You can start with $25 a month if that is what you have. Starting small and building the habit matters more than starting big.

Is investing risky right after building my emergency fund? All investing carries some risk. But keeping your emergency fund untouched in a high-yield savings account and investing separately means a market downturn does not threaten your basic financial stability.

Should I invest if I have student loans? It depends on the interest rate. Federal student loans under 5% are generally worth investing alongside rather than aggressively paying off first. At 7% or above, paying down the debt first often makes more mathematical sense.

What is a good return to expect? The S&P 500 has historically averaged around 10% annually before inflation over long periods. After inflation, closer to 7%. These are averages across decades, not guarantees — some years are up 30%, some years are down 20%.

What if the market crashes right after I start? Keep investing. This is not a pep talk — it is arithmetic. When markets drop, your monthly contributions buy more shares at lower prices. Investors who kept buying during the 2020 pandemic crash saw enormous gains by the end of that same year.

Sources Used in This Article

- SPIVA U.S. Scorecard, S&P Dow Jones Indices — spglobal.com

- IRS Retirement Topics: IRA Contribution Limits 2024 — irs.gov

- Vanguard Principles for Investing Success — investor.vanguard.com

- Fidelity Viewpoints: Getting Started — fidelity.com

- Consumer Financial Protection Bureau: Saving and Investing — consumerfinance.gov

Helpful Next Steps

If you are ready to move forward, here is a simple path that does not require doing everything at once.

This week, find out if your employer offers a 401(k) match and whether you are capturing the full amount. If not, increase your contribution.

Next week, open a Roth IRA at Fidelity or Vanguard. Takes about 15 minutes online.

Within the month, set up an automatic monthly contribution — even $100 to start — into a total market index fund.

Then leave it alone. Check in once a quarter. Let compounding do the heavy lifting while you get on with your life.

The emergency fund you built proved you can be patient and consistent with money. That same quality is the only real skill investing requires. The financial industry sells complexity because complexity is profitable for them. For you, simple and steady wins every time.

You already did the hard part. Now let your money start doing some of the work.