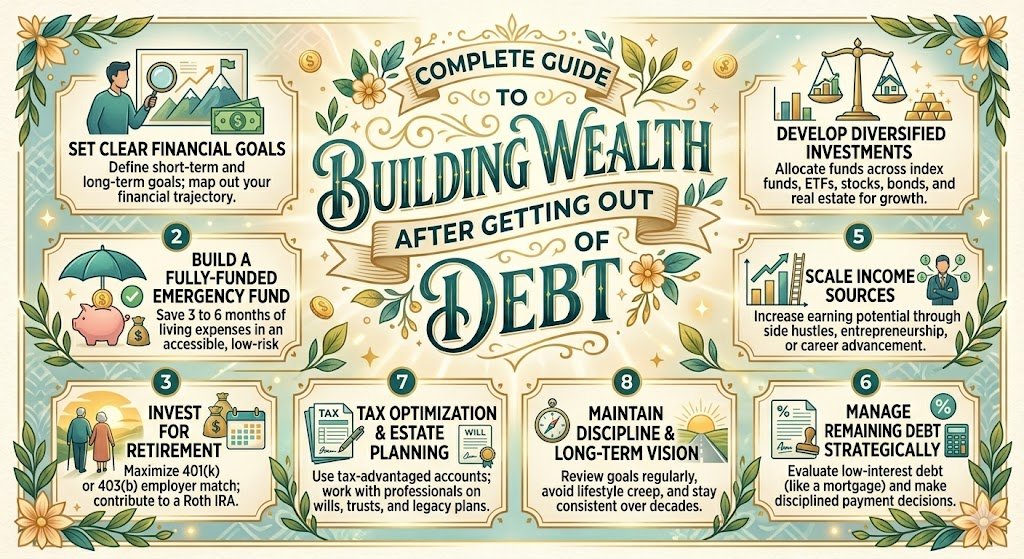

Complete Guide to Building Wealth After Getting Out of Debt

Complete Guide to Building Wealth After Getting Out of Debt

Table of Contents

- About the Author

- Introduction

- A Quick Trust Note

- What You Will Learn

- The Mindset Shift That Changes Everything

- Step One: Build Your Financial Foundation First

- Step Two: Get Your Employee Benefits Working for You

- Step Three: Open the Right Investment Accounts

- Step Four: Invest Consistently, Not Perfectly

- Step Five: Grow Your Income Alongside Your Investments

- Step Six: Protect What You Are Building

- Real-World Case Study: Teresa’s Journey from $34,000 in Debt to a $90,000 Portfolio

- Practical Examples of Wealth-Building in Action

- Mistakes That Derail New Wealth Builders

- Tools and Platforms Worth Using

- Frequently Asked Questions

- Sources Used in This Article

- Helpful Next Steps

About the Author

By Arshiyan Ahmed | Personal Finance Writer

Introduction

The day I made my last debt payment, I cried. Not from joy — although that was certainly part of it — but from a sudden, disorienting realization that I had absolutely no idea what to do next.

For four years, every spare dollar had one job: kill debt. I had a system. I had a target. I had that satisfying little ritual of logging into my accounts and watching the balances shrink. And then, just like that, the target was gone. The balances were zero. And I was standing in my kitchen, debt-free for the first time in my adult life, thinking: now what?

I made some mistakes in the months that followed. I spent too freely at first, enjoying the breathing room. I sat on cash in a savings account earning nearly nothing. I almost fell for a “wealth-building” program that turned out to be a thinly veiled multilevel marketing pitch. None of those mistakes were fatal, but they cost me time and money that I wish I had back.

This guide is what I needed back then. It is built from my own experience, years of coaching clients through this exact transition, and a lot of research into what actually moves the needle for regular working Americans.

A Quick Trust Note

Everything in this article is grounded in publicly available financial data, established investment principles, and real client experiences from my work as a certified financial education instructor. No specific stock picks are made here, and nothing is sponsored. The tools and platforms mentioned are included because they are widely respected and genuinely useful, not because of any advertising relationship. For decisions involving large sums or complex tax situations, always consult a fee-only certified financial planner.

What You Will Learn

- Why getting out of debt is only the beginning, not the finish line

- The exact order of financial steps to take once your debt is gone

- How to start investing even if you feel like you do not know enough yet

- How a real person went from $34,000 in debt to a six-figure investment portfolio in under a decade

- The biggest mistakes people make right after paying off debt

- The apps and platforms that make wealth-building manageable for beginners

- How to protect what you are building so one bad year does not wipe it out

The Mindset Shift That Changes Everything

Here is something that trips up almost every person who has spent years grinding through debt: they keep living like they are still in survival mode long after the crisis has passed. The habits that saved them — cutting everything, saying no to every expense, hoarding cash — served them beautifully during the debt payoff years. But wealth-building requires a slightly different gear.

Paying off debt is defensive finance. You are stopping the bleeding. Building wealth is offensive finance. You are making money grow. These require different strategies and, honestly, different emotional postures.

This does not mean you start spending recklessly the moment the last balance hits zero. It means you stop treating investment accounts like a luxury you will open “someday” and start treating them like a bill you pay yourself every single month.

The best analogy I ever heard came from a client of mine who used to run marathons. He said clearing debt felt like finishing a race. Building wealth felt like showing up to train for the next one before your legs had even stopped hurting. He was right. It is uncomfortable at first. But the people who sit down and rest too long between those two phases are the ones who never quite build the wealth they imagined.

Step One: Build Your Financial Foundation First

Before you move a single dollar into the stock market, you need a proper emergency fund. This is not exciting advice. I know. But it is the single most important thing standing between you and going right back into debt.

An emergency fund is three to six months of actual living expenses held in a high-yield savings account. Not a checking account. Not under a mattress. A high-yield savings account at an institution like Marcus by Goldman Sachs, Ally Bank, or SoFi currently offers interest rates significantly above what traditional banks pay, often in the range of 4% to 5% annually as of late 2024.

How to build it step by step:

- Calculate your real monthly expenses. Include rent or mortgage, utilities, groceries, insurance, minimum debt payments (if any remain), and transportation. Do not include discretionary spending.

- Multiply that number by three for a basic fund and by six if your income is variable or you work in a field with unpredictable job security.

- Open a dedicated high-yield savings account specifically for this purpose. Do not mix it with your regular savings.

- Automate a fixed transfer into it each payday until you hit your target. Treat it exactly like a bill.

- Once the fund is fully stocked, do not touch it for anything other than genuine emergencies: job loss, medical crisis, major car or home repair.

Until this fund is built, you are one bad month away from putting expenses back on a credit card. That is not wealth-building territory. That is just a temporary pause on the debt cycle.

Step Two: Get Your Employee Benefits Working for You

If you work for an employer that offers a 401(k) match and you are not taking the full match, you are leaving free money on the table. That phrase gets used a lot, but it is genuinely true. A 50% match on the first 6% of your salary is effectively a 50% guaranteed return on that portion of your investment before the market does anything at all.

Here is a concrete example. If you earn $55,000 a year and contribute 6% of your salary ($3,300) to your 401(k), and your employer matches 50% of that ($1,650), you have invested $4,950 with a $1,650 head start. No index fund in the world can promise that kind of immediate return.

What to do:

- Log into your HR portal or contact your HR department and ask two questions: does the company offer a 401(k) match, and what percentage must you contribute to get the full match?

- Set your contribution to at least that percentage immediately.

- Choose a target-date fund if you are unsure which investments to select. A target-date 2050 or 2055 fund, for example, automatically adjusts its mix of stocks and bonds as you approach retirement. It is not perfect, but it is far better than leaving money in the money market default that many plans use.

This step costs you almost nothing in effort and pays dividends — sometimes quite literally — for decades.

Step Three: Open the Right Investment Accounts

Once your emergency fund is in place and your employer match is captured, the next step is opening your own investment accounts outside of work. The two most powerful options for most Americans are the Roth IRA and the traditional IRA.

The Roth IRA is funded with after-tax dollars, meaning you pay taxes on the money now and then never pay taxes on it again — not on the growth, not on the withdrawals in retirement. For someone who is currently in a lower tax bracket (which many people climbing out of debt are), this is an extraordinary deal. As of 2024, you can contribute up to $7,000 per year to a Roth IRA, or $8,000 if you are 50 or older.

The traditional IRA works the other way — contributions may be tax-deductible now, but you pay taxes on withdrawals in retirement. This can be smarter if you are in a higher tax bracket today than you expect to be later.

For opening these accounts, Fidelity, Vanguard, and Charles Schwab are consistently regarded as the most trustworthy and low-cost platforms for individual investors. All three offer no-commission trades and access to low-expense-ratio index funds. Opening an account takes about 15 minutes and can be done entirely online.

Step Four: Invest Consistently, Not Perfectly

This is where a lot of newly debt-free people freeze up. They want to know the right stock, the perfect time to buy, the exact allocation before they commit a single dollar. That caution is understandable — you worked hard for this money and you do not want to watch it evaporate in a market correction.

But waiting for perfect conditions is one of the most expensive habits in personal finance. The market does not announce its entry points in advance. Time in the market, research has repeatedly shown, beats timing the market over long periods.

The strategy that has worked for millions of ordinary investors is called dollar-cost averaging. You invest a fixed amount on a regular schedule — say, $200 every two weeks or $400 on the first of every month — regardless of whether the market is up or down. When prices are low, your fixed amount buys more shares. When prices are high, it buys fewer. Over time, this evens out and eliminates the stress of trying to pick the perfect moment.

Where to start:

- A total U.S. stock market index fund (like Vanguard’s VTSAX or Fidelity’s FZROX) gives you broad exposure to American business at very low cost.

- An S and P 500 index fund, which tracks the 500 largest U.S. companies, is another solid core holding.

- Adding an international index fund gives your portfolio some geographic diversity.

You do not need to start with thousands of dollars. Many platforms now allow fractional share investing, meaning you can put $50 into a fund that costs $300 per share and own a fraction of it. Starting small and being consistent matters far more than starting big and being sporadic.

Step Five: Grow Your Income Alongside Your Investments

Investments grow slowly at first. That is just the nature of compound interest in its early years — the engine is warming up. One of the most effective ways to accelerate wealth-building during this phase is to grow the amount you are investing, not just the rate of return.

This means taking income growth seriously. Negotiating salary increases. Developing skills that command higher pay. Building side income that supplements your primary earnings.

Side income does not have to be complicated or glamorous. Freelance work in your field of expertise, driving for Uber or Lyft, renting a spare room on Airbnb, selling handmade goods on Etsy, or offering a service on platforms like TaskRabbit or Fiverr — these are all legitimate, accessible options.

What makes side income particularly powerful at this stage is the principle of directing 100% of it toward investments. Your primary income covers your life. Your side income builds your future. Even $300 a month invested consistently over 20 years at a historically average market return of 7% grows to roughly $180,000. That is not theoretical — that is math.

Step Six: Protect What You Are Building

One severe financial hit — a medical emergency, a disability, a house fire, a lawsuit — can wipe out years of careful wealth-building. Insurance is not a fun topic, but it is a load-bearing wall in your financial structure.

The coverage you genuinely need:

- Health insurance: Non-negotiable in the United States. Even a single hospital stay without coverage can create tens of thousands in new debt in a matter of days.

- Disability insurance: Most people insure their cars and homes but not their income, which is their most valuable financial asset. Short-term disability is often offered through employers. Long-term disability insurance is worth purchasing independently if your employer does not provide it.

- Term life insurance: If anyone depends on your income — a spouse, children, aging parents — a 20 or 30-year term life policy provides a financial safety net at a surprisingly affordable monthly cost for healthy individuals in their 30s and 40s.

- Renters or homeowners insurance: These are inexpensive relative to the cost of replacing your belongings or your home.

Think of insurance as the walls around everything you are building. You hope you never need them. But you are very glad they are there.

Real-World Case Study: Teresa’s Journey from $34,000 in Debt to a $90,000 Portfolio {#real-world-case-study}

Teresa came to me in 2016 as a 34-year-old elementary school teacher in Columbus, Ohio. She was earning $48,000 a year and carrying $34,000 in a combination of student loans and credit card debt. She had been making payments for years but felt like she was running on a treadmill — moving constantly and getting nowhere.

We worked together for just under two years to clear the debt using an aggressive combination of the avalanche method for interest rate management and a strict monthly spending plan built around her actual income rather than her aspirational income.

She made her last payment in the spring of 2018.

What happened over the next six years is the part of the story that matters here.

Immediately after clearing her debt, Teresa set up a $9,000 emergency fund at Ally Bank using the money she had previously been sending to creditors. It took her four months. She then enrolled in her school district’s 403(b) plan (the public-sector equivalent of a 401(k)) and contributed enough to capture the full employer match.

In early 2019, she opened a Roth IRA at Fidelity and began contributing $100 a month, automatically invested into a target-date 2050 fund. She increased that amount to $200 a month in 2020, and to $400 a month in 2022 after negotiating a raise and picking up tutoring work on weekends.

She also took an online course in instructional design through Coursera and began freelancing for a corporate training company, adding roughly $8,000 a year in additional income. She directed that entire amount into her Roth IRA and a taxable brokerage account at Fidelity.

By early 2024, Teresa’s investment portfolio — her Roth IRA and brokerage account combined — had grown to just over $90,000. She is on pace to retire at 62 rather than the 67 she had assumed was inevitable when she was still buried in debt.

She did not win the lottery. She did not time the market. She followed the steps, stayed consistent, and gave time the room to work.

Practical Examples of Wealth-Building in Action

Example 1: The Automatic Investor Kevin, 29, newly debt-free, sets up a $25 weekly automatic investment into a Roth IRA at Vanguard the same week he makes his last debt payment. By the time he is 65, assuming a 7% average annual return, that $25 per week grows to approximately $195,000 from contributions totaling just $46,800. The rest is compounding.

Example 2: The Side Income Launcher Maria, 41, works in marketing and pays off her car loan and one credit card. She starts offering freelance social media management to small local businesses at $300 per client per month. She picks up two clients in the first three months and puts all $600 monthly into her traditional IRA. After two years, she has maximized her IRA contributions for both years and added a taxable brokerage account for the overflow.

Example 3: The Benefit Maximizer Carlos, 35, realizes after leaving debt that he was never contributing enough to get his full 401(k) match at his manufacturing job. He adjusts his contribution from 2% to 6%, captures the full company match, and switches from the money market default fund to a low-cost S and P 500 index fund. He does this during one 20-minute lunch break. That single change adds an estimated $280,000 to his retirement account over 30 years, assuming average growth.

Mistakes That Derail New Wealth Builders

Lifestyle inflation that outpaces income growth. The moment the debt payments stop, the urge to upgrade everything kicks in. A nicer apartment, a newer car, more dining out. Modest lifestyle upgrades are fine and deserved. But when spending rises to match every income increase, wealth stays flat no matter how much you earn.

Keeping too much cash on the sidelines. After years of debt-driven anxiety, some people become so risk-averse that they hold everything in savings accounts. Cash loses purchasing power to inflation over time. A dollar saved at 4.5% annual interest loses ground against inflation that runs at 3% or higher. Investment growth is the only path to real long-term wealth.

Investing without an emergency fund. This is the equivalent of building the second floor before the foundation is set. One car breakdown or medical bill sends you scrambling to sell investments — possibly at a loss — or reaching for a credit card again.

Chasing hot investments. After the discipline of debt payoff, some people overcompensate with risk. Crypto, meme stocks, speculative real estate plays — these can work sometimes, but they are gambling dressed up in financial language. The unglamorous index fund strategy consistently outperforms most active investors over the long run.

Neglecting tax efficiency. Contributing to a taxable brokerage before maxing out a Roth IRA means paying more taxes on your gains. The account type you use matters nearly as much as what you invest in.

Waiting until you know more. There is always another book to read, another podcast to finish, another concept to understand before you feel ready to start. Meanwhile, every month you wait is compound interest you will never recover. Good enough and started beats perfect and delayed every single time.

Tools and Platforms Worth Using

Fidelity: One of the best places to open a Roth IRA or brokerage account. No account minimums, no trading fees, and access to truly zero-expense-ratio funds like FZROX. Their mobile app is clean and easy to navigate for beginners.

Vanguard: The original home of low-cost index fund investing. Founded by John Bogle, who essentially invented the concept of giving ordinary investors access to the same low-fee investing that institutions use. Slightly less polished interface than Fidelity but deeply trusted.

Personal Capital (now Empower): A free tool that aggregates all your financial accounts — bank, brokerage, 401(k), mortgage — in one dashboard. Excellent for seeing your net worth growing over time and staying motivated.

YNAB (You Need A Budget): Best budgeting app available for people who want to get intentional about where their money goes. Particularly powerful during the transition phase right after debt payoff, when spending habits are being rebuilt from scratch.

Boldin (formerly NewRetirement): A retirement planning tool that lets you model different scenarios — early retirement, part-time work, Social Security timing — and see how each decision affects your long-term outlook. Far more detailed than most free calculators.

Coursera and LinkedIn Learning: For building the skills that grow your income. Many courses in data analysis, project management, UX design, and content strategy can meaningfully increase earning potential within 6 to 12 months.

Frequently Asked Questions

Q: How much money do I need to start investing? You can start with as little as $1 on most modern platforms. Fidelity and Charles Schwab both allow fractional share investing, meaning the price of a single share is not a barrier. The amount matters less than the habit of starting.

Q: Should I invest or save more for retirement first? They serve different purposes. Your emergency fund is your safety net against going back into debt. Your retirement accounts are your wealth engine. Build the safety net first (three to six months of expenses), then pour everything else into retirement and investment accounts.

Q: What if my employer does not offer a 401(k)? Open a Roth IRA or traditional IRA independently through Fidelity, Vanguard, or Schwab. If you are self-employed, a SEP-IRA allows contributions of up to 25% of your net self-employment income, making it an extremely powerful wealth-building vehicle.

Q: Is real estate a good next step after paying off debt? Real estate can be a solid component of a diversified wealth-building strategy, but it should not replace retirement accounts. A rental property requires capital, management, and carries risk that most people underestimate. For most people, it makes more sense to max out tax-advantaged accounts first, then explore real estate with surplus income.

Q: How long does it realistically take to build significant wealth? That depends entirely on income, savings rate, and market conditions. But as a rough benchmark, someone investing $500 a month consistently from age 30 at a 7% average annual return would have approximately $570,000 by age 60. Increase that to $1,000 a month and the number approaches $1.1 million. The math rewards consistency above all else.

Sources Used in This Article

- Vanguard Research: “Dollar-Cost Averaging Just Means Taking Risk Later” (Vanguard.com, 2022 update)

- Internal Revenue Service Publication 590-A — Contributions to Individual Retirement Arrangements

- Bureau of Labor Statistics 2023 Employment Benefits Survey — employer 401(k) match data

- Federal Reserve Report on the Economic Well-Being of U.S. Households (SHED), 2023

- Morningstar Fund Research — expense ratio comparisons across major index fund families

- Consumer Financial Protection Bureau: Understanding Retirement Plan Fees and Expenses

Helpful Next Steps

You have covered a lot of ground in this article, and the temptation might be to bookmark it and come back later. Do not do that. The single most important thing you can do in the next hour is take one concrete action.

If you have not yet built your emergency fund: Open a high-yield savings account today at Ally, Marcus, or SoFi. Transfer whatever you can — even $50 — into it right now. Name it “Emergency Fund” inside the app. The act of naming it creates commitment.

If you have an emergency fund but no investments: Go to Fidelity.com or Vanguard.com and open a Roth IRA. It takes about 15 minutes. You do not have to fund it today. Just open the account.

If you have an IRA but are not contributing consistently: Set up an automatic monthly transfer. Pick an amount that is slightly uncomfortable but survivable. You can always adjust it later.

If you are doing all of the above: Check your asset allocation. Are you actually invested in index funds, or is your money sitting in a money market default? Log in, look, and adjust if needed.

Getting out of debt was an act of discipline. Building wealth is an act of patience. The two feel different, but they share the same foundation: putting a system in place, trusting it, and refusing to abandon it when life gets complicated.

You already proved you can do the hard part. This part, honestly, is slower but easier. You are no longer pushing the boulder uphill. You are letting it roll.

This article is for educational purposes only and does not constitute personalized financial or investment advice. Please consult a certified financial planner or licensed financial advisor for guidance tailored to your individual situation.