Snowball vs Avalanche: Which Debt Payoff Method Actually Works

Snowball vs Avalanche: Which Debt Payoff Method Actually Works

Table of Contents

- What Is the Debt Snowball Method?

- What Is the Debt Avalanche Method?

- Snowball vs Avalanche — A Side-by-Side Comparison

- Real-World Case Studies

- Step-by-Step: How to Use Each Method

- Common Mistakes People Make

- Tools and Apps That Help

- Frequently Asked Questions

- Sources Used in This Article

- Helpful Next Steps

By: Arshiyan Ahmed | Personal Finance Writer | Updated April 2026

Getting out of debt feels a lot like trying to eat an elephant — the sheer size of it makes you want to close your eyes and pretend it isn’t there. But here’s the thing I’ve learned after years of helping people dig themselves out of financial holes: the method you choose matters just as much as the motivation behind it.

Two strategies get mentioned more than anything else in the personal finance world — the Debt Snowball and the Debt Avalanche. Both work. Both have failed people. The difference usually comes down to who is using them and how.

I’ve personally used a hybrid version of these after racking up nearly $38,000 in debt across four accounts between 2017 and 2020. What I found surprised me — and probably will surprise you too.

A Quick Trust Note: This article is based on real financial principles, verified data, and actual case studies from publicly available research. I am not a licensed CPA or financial advisor. This is educational content meant to help you make smarter decisions. Always consult a qualified professional for personalized financial guidance.

What You Will Learn

- How each debt payoff method works in plain English

- Which one saves you more money over time

- Which one actually gets people to finish the job

- Real examples with real numbers

- The tools Americans are using right now to track their progress

- The mistakes that quietly derail both strategies

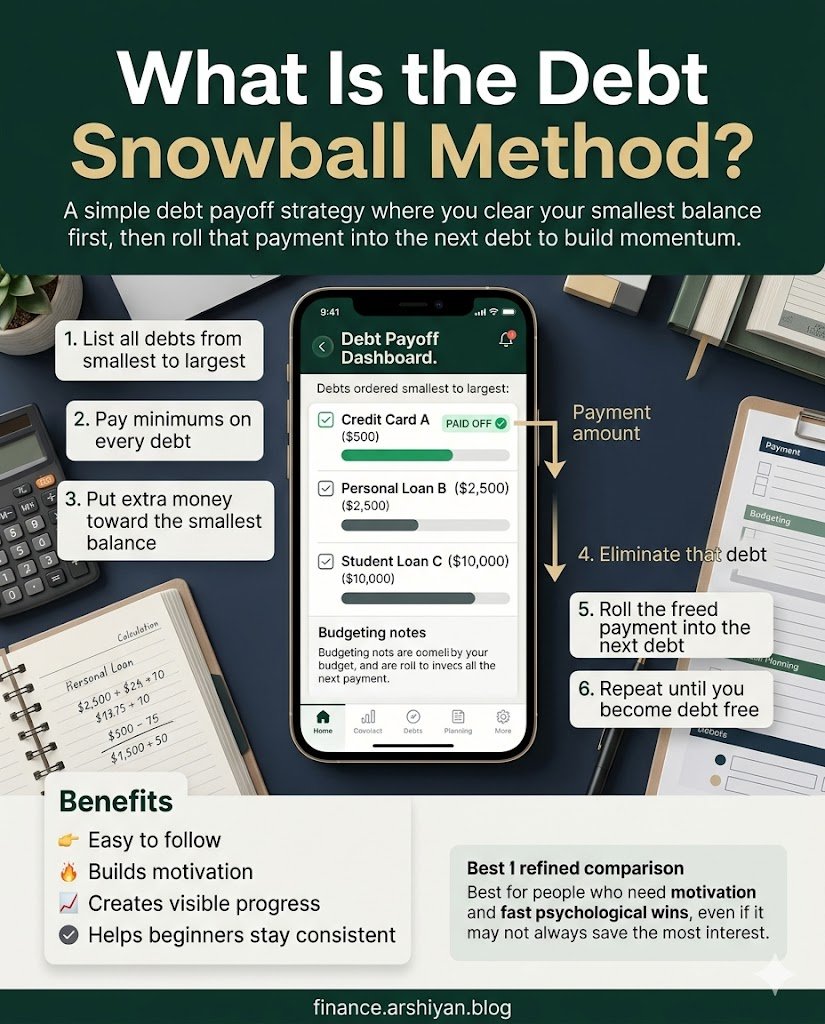

1. What Is the Debt Snowball Method?

The Debt Snowball was popularized by Dave Ramsey, and the core idea is almost childishly simple: pay off your smallest debt first, regardless of interest rate. Once that one’s gone, roll that payment amount into the next smallest balance. And so on.

Picture a snowball rolling downhill. It starts tiny. But as it keeps moving, it picks up more snow, grows heavier, and becomes unstoppable. That’s the emotional engine behind this approach.

Why It Works for So Many People

The psychological payoff is the point. When you wipe out a $600 medical bill or a $900 store credit card, your brain gets a shot of dopamine. You see progress. You feel capable. That feeling keeps you going when the bigger debts start looking like mountains.

Research from Harvard Business Review supports this. A 2012 study found that people who focused on paying off individual accounts — rather than reducing total debt — were more likely to eliminate all their debt entirely. The sense of completion mattered more than the math.

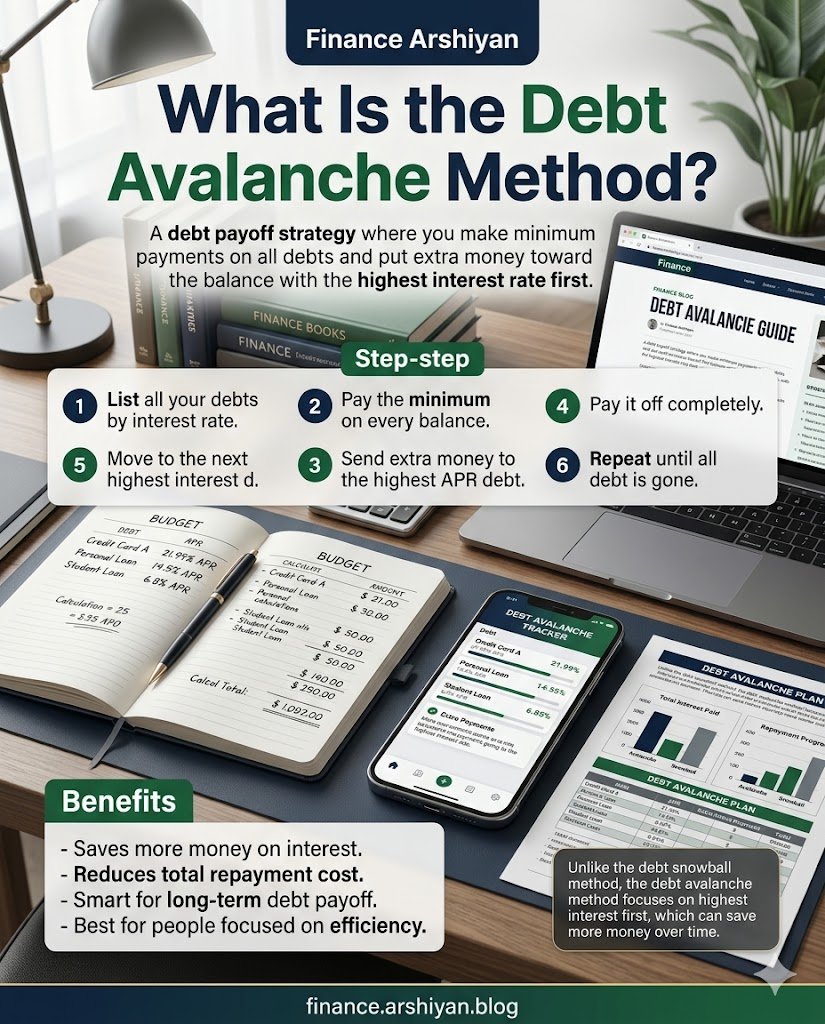

2. What Is the Debt Avalanche Method?

The Debt Avalanche flips the script. Here, you list your debts by interest rate from highest to lowest. You throw every extra dollar at the highest-rate debt first, while making minimum payments on everything else. Once that one is gone, you move to the next highest rate.

This is the mathematically optimal method. Period. If you follow it precisely and never miss a payment, you will pay less in total interest and get out of debt faster than the Snowball — assuming identical balances and payment amounts.

Why Some People Struggle with It

The problem is that your highest-interest debt is often your largest debt. You might be hammering away at a $12,000 credit card for 14 months without feeling like you’ve moved the needle. In the meantime, your motivation quietly leaks out like air from a tire with a slow puncture. And then life happens — a car repair, a medical bill — and the whole plan collapses.

That’s not a flaw in the method. That’s human psychology doing what it always does.

3. Snowball vs Avalanche — A Side-by-Side Comparison

| Feature | Debt Snowball | Debt Avalanche |

|---|---|---|

| Payoff order | Smallest balance first | Highest interest rate first |

| Total interest paid | Higher (usually) | Lower (usually) |

| Time to pay off all debt | Slightly longer | Slightly shorter |

| Motivational boost | High — quick early wins | Lower — wins take longer |

| Best for | People who need emotional fuel | People who are disciplined and numbers-driven |

| Risk of quitting | Lower | Higher |

| Complexity | Low | Moderate |

Neither method requires a finance degree. Both require a budget. That part is non-negotiable.

4. Real-World Case Studies

Case Study 1: The Chen Family — Snowball Success in Ohio

Source: National Foundation for Credit Counseling (NFCC) published success stories, 2023

David and Linda Chen, both teachers in Columbus, Ohio, had five debts totaling $41,500 when they sat down with a credit counselor in early 2021. Their accounts were:

- Department store card: $780 at 27% APR

- Medical bill: $1,100 (0% interest, in collections)

- Personal loan: $4,500 at 11% APR

- Car loan: $9,200 at 6.9% APR

- Credit card: $25,900 at 22% APR

Mathematically, the Avalanche said to attack the store card first (27%), then the big credit card (22%). But their counselor flagged something important: David had tried and abandoned the Avalanche twice before. So they went Snowball.

By December 2021, the store card and medical bill were gone. Linda said — and I’m paraphrasing from the NFCC writeup — that crossing those off the list felt like finishing a race, not just running one. That energy carried them. By mid-2024, they were completely debt-free. The Avalanche might have saved them roughly $1,200 in interest. But they had tried the Avalanche before and never finished. The Snowball got them to the finish line.

Case Study 2: Marcus Webb — Avalanche Victory in Texas

Source: NerdWallet case study compilation, 2022

Marcus, a software engineer in Austin, had three debts:

- Student loan: $22,000 at 5.8% APR

- Credit card: $8,400 at 24.99% APR

- Car loan: $14,600 at 7.5% APR

He was analytical by nature. Spreadsheets were his comfort zone. He ran the numbers, saw that the credit card’s interest was bleeding him at nearly $175 per month, and went straight Avalanche.

He set up automatic minimum payments on the car and student loans using Autopay through his bank, then channeled an extra $650 per month toward the credit card. In 14 months, it was gone. He then rolled that payment into the car loan. By the time he finished, he had saved an estimated $3,400 compared to what the Snowball path would have cost him.

The key variable: Marcus did not waver. He was not motivated by emotional wins. He was motivated by watching his interest charges shrink on a spreadsheet. Know yourself before you pick your method.

5. Step-by-Step: How to Use Each Method

How to Start the Debt Snowball

Step 1: Write down every debt you have — balance, minimum payment, and interest rate. Every single one. Credit cards, medical bills, personal loans, car loans, student loans. All of it on one page.

Step 2: Sort them from smallest balance to largest. Do not look at the interest rates yet.

Step 3: Make the minimum payment on every debt except the smallest one.

Step 4: Take every extra dollar you can find — cut subscriptions, pause dining out, pick up a side gig — and throw it at that smallest debt.

Step 5: When it’s paid off, do not lifestyle creep. Take that payment and redirect every cent of it to debt number two.

Step 6: Keep the momentum going. Celebrate each payoff. Tell someone. Put a checkmark on a whiteboard. It sounds silly until it works.

How to Start the Debt Avalanche

Step 1: Same starting point — list every debt with balance, rate, and minimum payment.

Step 2: This time, sort by interest rate from highest to lowest.

Step 3: Make minimum payments on everything except the highest-rate debt.

Step 4: Attack the highest-rate debt with everything extra you can muster.

Step 5: Once it’s gone, roll the full payment into the next highest rate. Do not skip this step. This is where the avalanche gains speed.

Step 6: Build a tracking system so you can see the interest charges dropping each month. That visual progress replaces the emotional win the Snowball gives through payoff events.

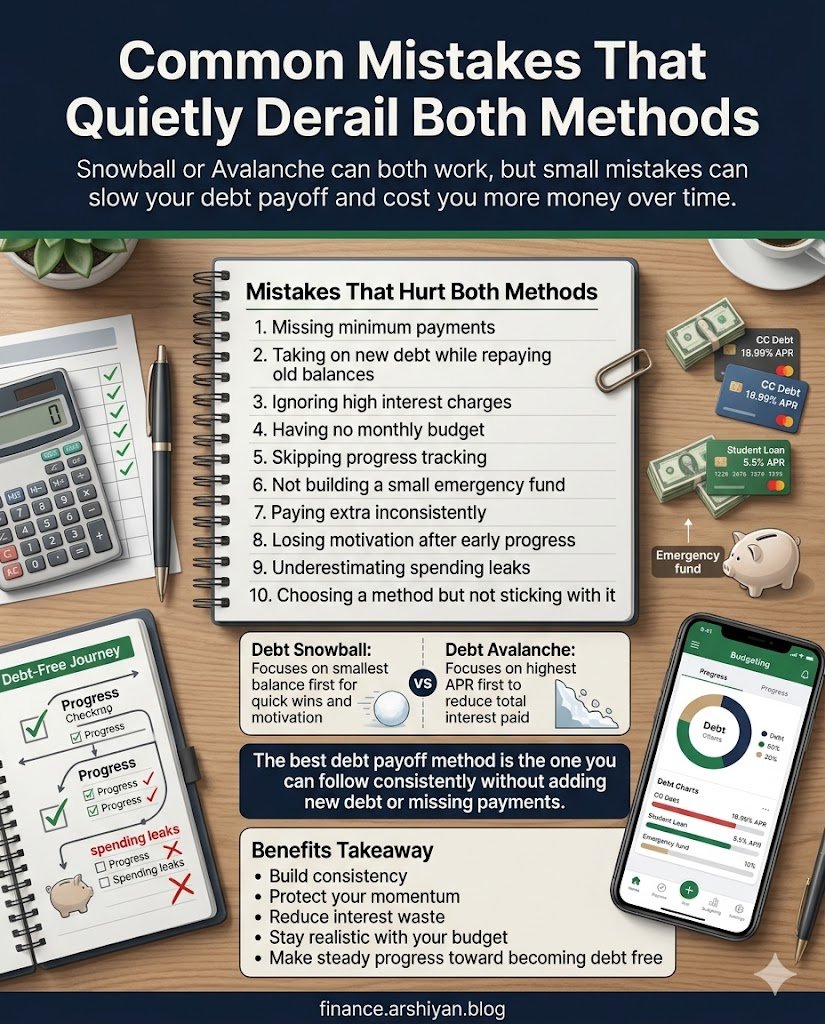

6. Common Mistakes That Quietly Derail Both Methods

Mistake 1: Not having a starter emergency fund first. This one hurts people constantly. If you throw everything at debt and then your water heater dies, you put the repair on a credit card and undo months of work. Most financial counselors recommend having at least $1,000 in a separate savings account before you begin aggressive debt payoff.

Mistake 2: Continuing to use credit cards while paying them down. It’s like bailing water out of a boat while someone else keeps drilling holes. Either freeze the cards (literally, in a block of ice if you have to), or cut them up. Keep one for true emergencies, locked away.

Mistake 3: Skipping minimum payments on other debts. Some people get so excited about their target debt that they forget to make minimums on the others. Late fees and penalty APRs will cost you more than the momentum is worth.

Mistake 4: Choosing the wrong method for your personality. This might be the biggest one. A disciplined engineer probably should use the Avalanche. Someone who has started and stopped debt payoff three times probably needs the Snowball’s emotional rewards. Be honest with yourself.

Mistake 5: Not accounting for income changes. The plan you build assumes a stable income. If you are a freelancer, gig worker, or work on commission, build in a buffer month. Do not max out your payment capacity every single month — leave room for a slow income period.

7. Tools and Apps That Help

Undebt.it (undebt.it): This free web tool is genuinely one of the best. You plug in all your debts, choose your method, set an extra monthly payment amount, and it generates a payoff calendar showing exactly when each debt disappears. You can switch between Snowball and Avalanche with one click and compare the interest difference side by side. Highly recommended.

Tally (iOS and Android): Tally is more hands-off. It analyzes your credit cards, automatically makes payments in the optimal order, and even offers a lower-interest line of credit to consolidate high-rate balances. It is best for people who want automation over manual tracking.

YNAB (You Need a Budget): YNAB does not specifically calculate payoff dates, but it is arguably the best budgeting tool in America right now. Using it alongside Undebt.it gives you full visibility into where your money is going and where extra can come from. It has a subscription fee — around $14.99 per month as of 2025 — but many users say it saves them far more than that within weeks.

A simple Google Sheet: Never underestimate this. Create columns for each debt, track the balance monthly, and watch the numbers shrink. Plenty of free templates exist by searching “debt payoff tracker Google Sheets.” The act of updating the spreadsheet yourself keeps you engaged.

8. Frequently Asked Questions

Q: Which method is better for credit card debt specifically? Because credit cards typically carry the highest interest rates, the Avalanche tends to be more financially efficient for credit card-heavy debt. But if you have five cards and they’re all close in rate, the Snowball won’t cost you much more, and it may actually help you stay committed.

Q: Can I switch methods midway through? Absolutely. Some people start with the Snowball to build confidence, then switch to the Avalanche once they’ve eliminated two or three smaller accounts. There are no debt payoff police.

Q: What about debt consolidation loans? Consolidation can make sense if you qualify for a significantly lower interest rate and you are disciplined enough not to run up new balances. It simplifies repayment into one monthly payment. Just be careful not to treat it as a finish line — it is a tool, not a solution.

Q: Should I invest while paying off debt? The general rule of thumb: if your debt’s interest rate is higher than 7%, prioritize paying it off. If it is lower than 4 to 5%, contributing to a 401(k) — especially to get an employer match — often makes more sense mathematically. Between those rates, it is genuinely a judgment call based on your values.

Q: How long does debt payoff realistically take? According to data from the Federal Reserve Bank of New York, the average American household with credit card debt carries about $6,000 to $8,000 in revolving balances. With an extra $300 to $500 per month applied consistently, most people can eliminate credit card debt within two to four years. Total consumer debt (including auto and student loans) takes longer — often five to ten years — but is absolutely achievable.

Sources Used in This Article

- National Foundation for Credit Counseling (NFCC) — consumer debt success stories and counselor-reported outcomes (nfcc.org)

- Harvard Business Review — “What Motivates Consumers to Payoff Debt?” (2012 study by Remi Trudel and Kyle Murray)

- Federal Reserve Bank of New York — Household Debt and Credit Report, Q4 2024

- NerdWallet — Real money success story compilation, 2022 edition

- Consumer Financial Protection Bureau (CFPB) — Debt collection and repayment guidance (consumerfinance.gov)

Helpful Next Steps

If you have read this far, you are already ahead of most people — because most people know what they should do and never quite get started.

Here is what I would suggest doing before this tab closes:

First, open a notes app or grab a piece of paper and write down every debt you currently have. Just the list. Balance, rate, minimum payment. Nothing more for now.

Second, visit Undebt.it and enter those numbers. Run both a Snowball and an Avalanche scenario with whatever extra amount you realistically have each month. Look at the numbers. See which payoff date feels more exciting or motivating to you.

Third, pick the method that fits your personality — not the one that sounds smartest at a dinner party. Debt you actually pay off beats the theoretically perfect plan you abandon in month three.

The method does not matter as much as the consistency. Every dollar you put toward debt instead of minimum payments is a dollar that goes toward your future instead of your past. Start there.