Budgeting for Students: Managing Money When You Have Almost None

Budgeting for Students: Managing Money When You Have Almost None

When I was a student, my budget was not really a budget. It was more like a small emergency meeting I held in my head every time I opened my wallet.

I knew the feeling of checking my bank app before buying tea. I knew the little sting of seeing friends order takeout while I was calculating whether instant noodles could be stretched into two meals and a sad breakfast. I knew what it felt like when one tiny surprise, like a lab fee, a bus card top up, or a broken charger, could knock the whole month sideways.

That is why I do not like fluffy money advice for students. It often assumes you have money to move around. Many students do not. You are not choosing between a luxury car and a modest car. You are choosing between printing lecture notes and having enough for lunch on Thursday.

If that is where you are, this guide is for you.

The first thing I want to say is this. Budgeting is still worth doing, even when your money feels laughably small. In fact, that is when it matters most. A budget will not turn twenty into two hundred. But it can stop twenty from vanishing like steam off hot rice.

A budget is not a punishment

I used to think budgeting meant saying no to everything and living like a monk with exam stress.

That idea made me resist it for too long.

A student budget is really a map. A scrappy little map, sure, maybe drawn in pencil on the back of a receipt, but still a map. It shows where your money leaks, what matters most, and how to make small amounts work harder.

When you have very little money, you do not need perfection. You need clarity.

And let me say something that would have helped me years ago. Being broke does not mean you are careless. Many students are dealing with genuinely tight finances. In Trellis Strategies’ Fall 2024 Student Financial Wellness Survey of more than 53,000 undergraduate students at 104 institutions, 56 percent said they would have trouble getting 500 dollars for an unexpected need in the next month, and 68 percent said they had run out of money at least once since the start of the year.

So if your money feels thin, you are not alone and you are not failing some secret adulthood test.

The budget I wish I had started sooner

The system that finally helped me was embarrassingly simple.

I stopped trying to look organized and started trying to be organized.

I used Google Sheets on an old laptop, my phone calculator, and my bank app. Nothing fancy. No glitter. No magical spreadsheet that sang to me at sunrise.

Here is the method.

Step 1: Find out what is actually coming in

As a student, your income may come from different places.

A part time job

Money from family

Scholarships or grants

Freelance work

Tutoring

Selling old books or notes

Odd jobs here and there

The mistake I made was treating random money as extra money. If I earned some tutoring cash, I spent it too fast because it felt like a bonus. But when your income is small, almost nothing is extra.

For one month, write down every amount that comes in.

Do not round it in your head.

Do not trust memory.

Write the real number.

For example, a student budget might look like this for one month:

Part time café job 120

Money from home 80

Tutoring one classmate 40

Scholarship refund 60

Total money in 300

Now you have a starting point. It may not be pretty, but at least it is honest.

Step 2: Protect the essentials first

This changed everything for me.

Before you budget snacks, subscriptions, or fun money, cover the things that keep life moving.

My own essentials were usually:

Food

Transport

Phone data

Printing and study materials

Basic toiletries

A small emergency cushion

If you pay rent, add that too. If your family covers housing, that is helpful, but do not use that as a reason to ignore the other essentials.

Take your total money and give the first jobs to the most important categories.

Using that same 300 example:

Food 110

Transport 45

Phone 20

Study costs 25

Toiletries 15

Emergency cushion 20

Laundry 15

That leaves 50

Only after this should you decide what to do with the leftover amount.

I learned the hard way that if I did not protect food and transport first, the month turned into a circus. I could deal with boring meals. I could not deal with missing class because I had no fare left.

Step 3: Use weekly limits, not just monthly ones

Monthly budgets can lie to students.

You see 120 dollars for food and think, nice, that is manageable. Then you spend half of it in the first week because the month looked longer in your imagination.

I started breaking key categories into weekly amounts.

If I had 120 for food for four weeks, that gave me 30 a week.

That made decisions much easier.

When a friend said, let us grab burgers tonight, I was not asking, can I afford this somehow. I was asking, does this fit inside this week’s food money without wrecking the rest of the week.

That one shift saved me from so many end of month disasters.

A monthly budget is a bird’s eye view. A weekly budget is your actual steering wheel.

Step 4: Make one tiny emergency fund

Please do this even if your budget feels microscopic.

I know it sounds almost funny to talk about savings when you are stretching every note and coin. I thought the same thing. But having even a tiny buffer changes your whole month.

My first goal was not 1000. It was 30.

Then 50.

Then 100.

That little cushion covered things like:

A phone charger that stopped working before exams

Extra transport for a group project

Medicine for a bad cold

A last minute course handout

It kept small problems from turning into a week of chaos.

That matters because student money problems are often not dramatic. They are death by a thousand paper cuts. One surprise print fee. One social event. One late bus. One lunch you did not plan for. That is how the ship starts taking on water.

The Trellis survey also found that 58 percent of respondents had experienced food insecurity, housing insecurity, or homelessness, and 43 percent reported housing insecurity in the prior 12 months. Those numbers are a reminder that even small financial shocks can hit students hard.

Step 5: Make cheap systems, not heroic promises

Heroic promises are useless. Systems are gold.

Do not tell yourself, I will just spend less this month.

That is smoke.

Instead, build a system that makes spending slower and smarter.

Here are a few that genuinely helped me.

I kept my food money separate in my head and sometimes in cash.

I wrote every expense in my Notes app before bed.

I used Google Sheets once a week, not ten times a day.

I turned off one click shopping.

I waited twenty four hours before buying anything that was not essential.

I shared household basics with roommates using Splitwise so nobody ended up buying detergent three times while forgetting cooking oil.

These are small moves, but small hinges swing big doors.

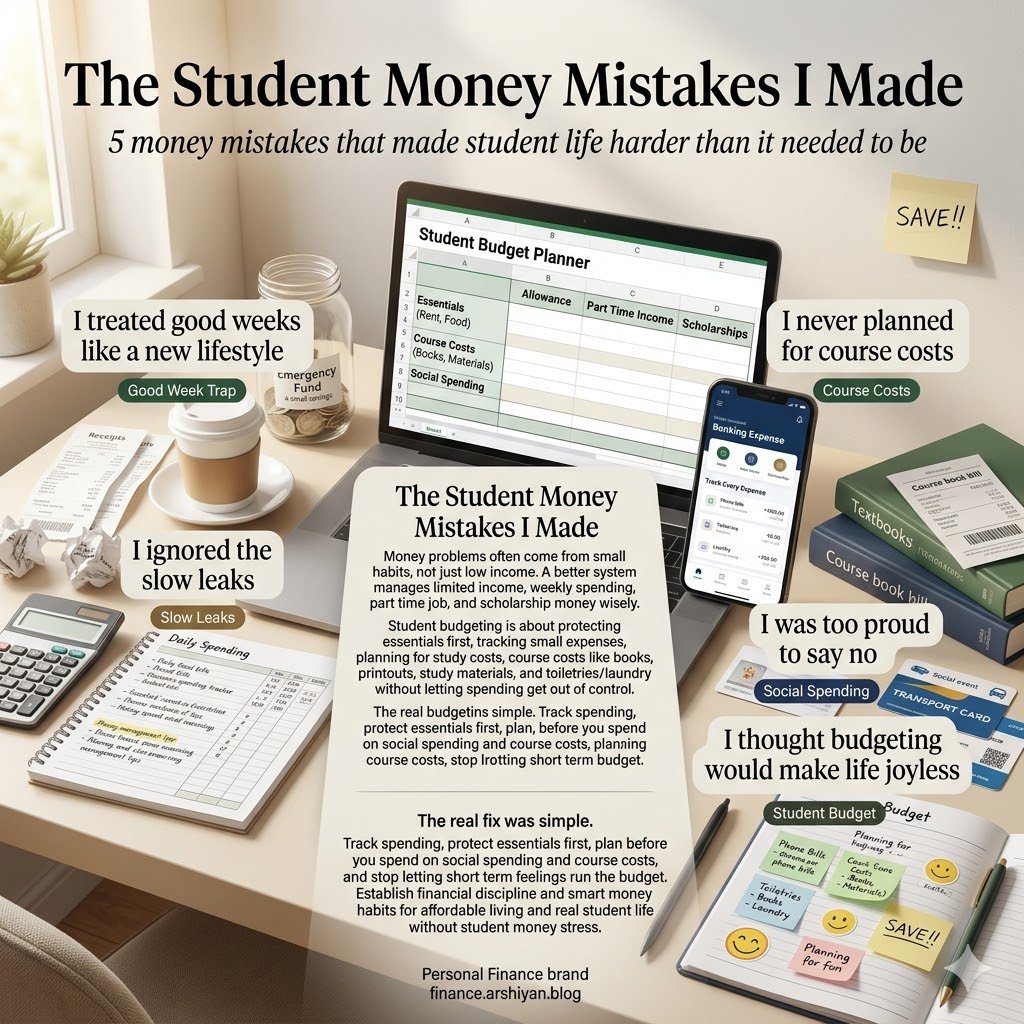

The student money mistakes I made

I made plenty, and some were so silly I laugh now, though I did not laugh then.

I treated good weeks like a new lifestyle

If I got extra money one week, I suddenly became a person who could afford iced coffee, rides, snacks, and little treats. My money had not changed that much. My mood had.

Result: I would feel rich for three days and confused for the next ten.

I ignored the slow leaks

Big spending is easy to spot. Small leaks are sneakier.

A snack here

A payment for extra storage there

A subscription I forgot

A few convenience buys because I was tired

Together they formed a tiny army that attacked my account every month.

I never planned for course costs

Books, printouts, stationery, software, lab items. These were not random surprises. They were regular visitors wearing fake moustaches.

Once I started putting aside even a small amount each month for study costs, things felt calmer.

I was too proud to say no

This one cost me real money.

Sometimes I joined plans because I did not want to look broke. Then I would spend the next week acting like a financial archaeologist, digging through couch cushions and old pockets.

A polite no is cheaper than a panicked yes.

I thought budgeting would make life joyless

The opposite happened.

Budgeting gave me permission to enjoy small things without guilt, because I knew where I stood. A cheap lunch with a friend tastes much better when you are not mentally subtracting bus fare from tomorrow morning.

A trustable case study that says a lot

One of the most useful research snapshots for student money right now comes from Trellis Strategies. In its Fall 2024 Student Financial Wellness Survey, more than 53,000 undergraduates across 104 institutions shared what money really looked like on campus. The findings were stark. More than half would struggle to find 500 dollars for an emergency, and more than two thirds had already run out of money at least once that year.

That matters because it tells us something important. Many students do not need lectures about avocado toast. They need better money systems, better support, and fewer avoidable mistakes.

Another useful reminder comes from Sallie Mae’s 2025 college funding research. Families reported spending an average of 30,837 dollars on college, and three in ten families skipped the FAFSA. That means some students may be leaving aid on the table before the semester even gets going.

My takeaway is simple. Student budgeting is not only about cutting costs. It is also about claiming support you are eligible for and making sure small money does not slip through your fingers.

Step by step plan for students who feel overwhelmed

If your finances are messy right now, do this for the next seven days.

Day 1

Open your bank app and write down your current balance.

No drama. No guilt. Just the number.

Day 2

Write down every regular cost you expect this month.

Food

Transport

Phone

Study supplies

Rent if applicable

Toiletries

Laundry

Any debt payment

Day 3

List every source of money that is likely to come in this month.

Job income

Family support

Scholarship money

Freelance cash

Anything realistic

Day 4

Match your income to your essentials first.

Do not budget entertainment until the basics have names and numbers.

Day 5

Choose a weekly spending limit for food and flexible spending.

This is your safety rail.

Day 6

Set a tiny emergency savings target.

Even 5 or 10 set aside regularly counts.

Day 7

Check whether you are missing outside support.

Scholarships

Campus emergency grants

Food pantry support

Transport discounts

Used textbook groups

Student deals on software

This part matters. Pride is expensive. Use the help that exists.

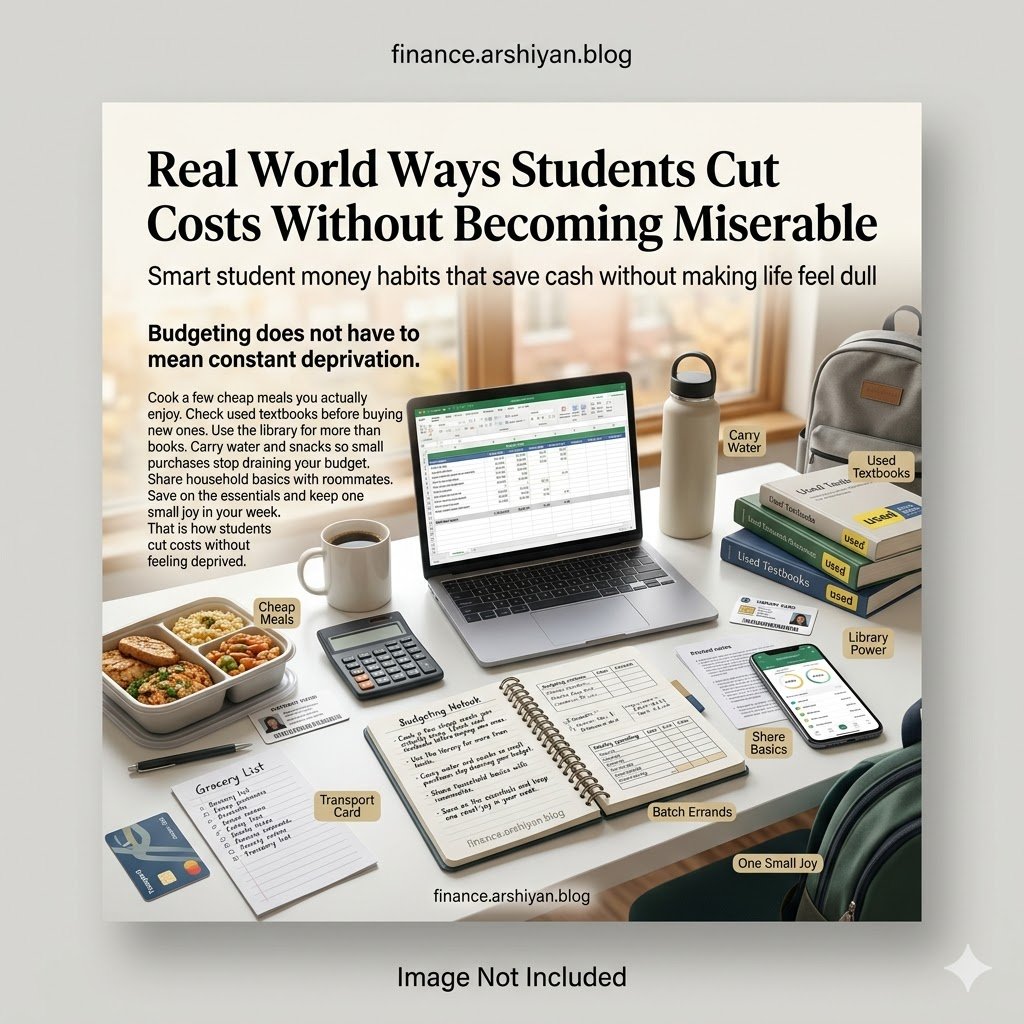

Real world ways students cut costs without becoming miserable

Cook two or three cheap meals on repeat instead of trying to become a budget chef overnight. Rice bowls, eggs, pasta, lentils, oats, potatoes, and frozen vegetables carried me through many weeks.

Buy used textbooks first and compare prices before touching the campus bookstore.

Use the library like it is your rich aunt. Books, study space, printers, wifi, software access, charging points. Sometimes even equipment loans.

Carry water and one snack. Hunger is expensive when a vending machine is the nearest option.

Batch errands so transport costs do not nibble at you all week.

Share basics with roommates, but write things down. Friendship is lovely. Memory is unreliable.

Keep one cheap joy in the budget. Mine was tea and a bakery bun once a week. A budget with no humanity in it will not last.

What changed when I finally got serious

The first result was not that I suddenly had lots of money.

The first result was that I stopped being surprised.

That is huge.

I stopped overdrafting.

I stopped pretending next week would magically fix this week.

I stopped spending scholarship money like it had no job.

I started finishing more months with at least something left, even if it was small.

Most importantly, I felt less ashamed. That part does not show up in spreadsheets, but it matters. Money stress can make you feel foolish, isolated, and behind. A working budget gives you back a bit of control, and control is a powerful thing when student life already feels like a juggling act on a windy day.

FAQ

How do I budget if my income changes every month?

Use the money you actually have, not the money you hope will arrive. Cover essentials first, then divide flexible spending by week.

Should students save money even when income is tiny?

Yes. Start tiny. The habit matters as much as the amount. A small cushion can stop a small problem from becoming a big one.

What is the best budgeting app for students?

The best one is the one you will really use. Google Sheets, your bank app, Notes, and a simple shared expense app can do the job just fine.

How much spending money should a student have each week?

There is no magic number. Look at your income and essential costs first. Whatever remains should be split carefully across the weeks.

Is it bad to say no to social plans because of money?

Not at all. A real friend will understand. Suggest a cheaper plan. A walk, tea, campus hangout, or movie night at home can cost far less than a restaurant trip.

What should I do first if my money is already a mess?

Check your balance, list your upcoming costs, cut optional spending for now, and protect food and transport first. Then look for campus support if needed.

Conclusion

Student budgeting is not glamorous. It is not a shiny vision board with color coded dreams and expensive stationery. Most of the time, it is humble work. It is writing down numbers honestly, planning before panic, and learning how to stretch a little money without stretching yourself to breaking point.

If you are a student with almost none, do not wait until you feel rich enough to budget. That day may not arrive on schedule. Start with what is in your account now. A small plan can still steady your feet, and sometimes that is exactly what you need to get through the month with your dignity, your dinner, and your bus fare intact.